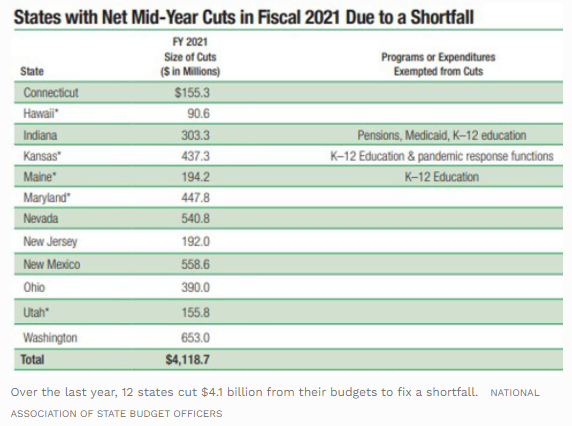

A total of 12 states had to cut a combined $4.1 billion from their budgets in order to balance out projected shortfalls before the end of their fiscal year, according to a new report released Thursday by the National Association of State Budget Officers (NASBO). (Most state fiscal years end on June 30.) Nevada, New Mexico and Washington state cut the most, accounting for 42% of the total.

Many of these states targeted staff for these cuts, including implementing hiring freezes, eliminating open positions, cutting salaries and ordering furloughs. They also turned to Medicaid, which saw more than $1 billion in combined cuts from the 12 shortfall states while higher education cuts totaled more than $500 million from the group. Washington State focused its cuts mainly on K-12 education, slashing more than $1 billion from the budget over the past year.

Somewhere in PHE’s data pipeline, someone had used the wrong Excel file format, XLS rather than the more recent XLSX. And XLS spreadsheets simply don’t have that many rows: 2 to the power of 16, about 64,000. This meant that during some automated process, cases had vanished off the bottom of the spreadsheet, and nobody had noticed.

The idea of simply running out of space to put the numbers was darkly amusing. A few weeks after the data-loss scandal, I found myself able to ask Bill Gates himself about what had happened. Gates no longer runs Microsoft, and I was interviewing him about vaccines for a BBC program called How to Vaccinate The World. But the opportunity to have a bit of fun quizzing him about XLS and XLSX was too good to pass up.

I expressed the question in the nerdiest way possible, and Gates’s response was so strait-laced I had to smile: “I guess… they overran the 64,000 limit, which is not there in the new format, so…” Well, indeed. Gates then added, “It’s good to have people double-check things, and I’m sorry that happened.”

Exactly how the outdated XLS format came to be used is unclear. PHE sent me an explanation, but it was rather vague. I didn’t understand it, so I showed it to some members of Eusprig, the European Spreadsheet Risks Group. They spend their lives analyzing what happens when spreadsheets go rogue. They’re my kind of people. But they didn’t understand what PHE had told me, either. It was all a little light on detail.

Illinois received its first credit rating upgrade in 23 years on Tuesday when Moody’s Investors Services raised the state’s rating one notch, citing “material improvement in the state’s finances.”

Although the upgrade still leaves Illinois bonds rated just two notches above so-called “junk” status, Gov. JB Pritzker said it marked a turning point for the state, and he credited the General Assembly and members of his own administration for bringing greater fiscal discipline to the state’s budget.

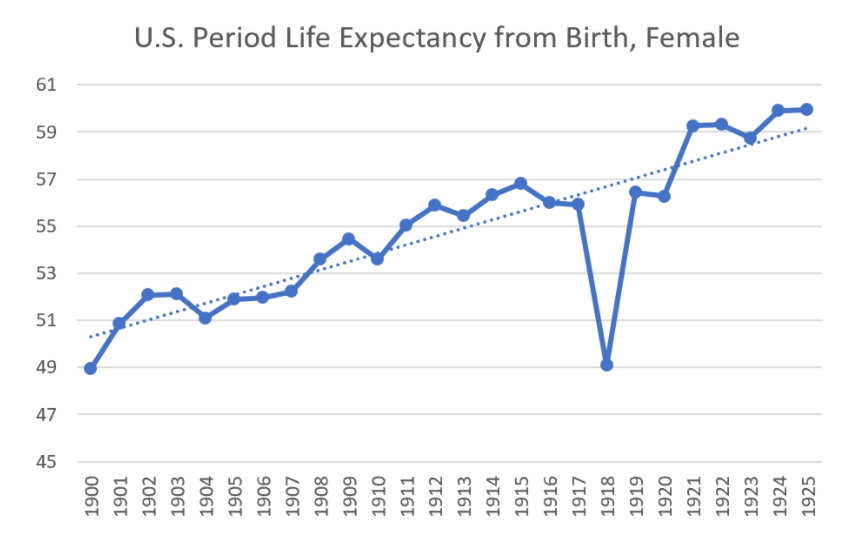

The Spanish flu pandemic gives us the demonstration of what happens when there is a short-term large increase in mortality.

Using Social Security records of period life expectancy, there was a huge drop in life expectancy in 1918…. and then a huge increase in 1919. But going from 1917 to 1919 wasn’t really that big of a difference.

The period life expectancy drop was 12% for females, 13% for males in 1918.

Then there was an increase of 15% for females, 20% for males in 1919. The Spanish flu hit the U.S. hard in 1918, and let up in 1919.

If you compare 1919 against 1917, the life expectancy from birth increase was 1% for females, and 4% increase for males — male life expectancy was down in 1917 compared to 1916, probably related to World War I.

Now, because the pandemic produced higher death rates in 2020 compared to prior years, a period life expectancy calculated for 2020 produced lower life expectancies compared to period life expectancies calculated for prior years. That’s because it’s assumed that the elevated death rates we experienced in 2020 would apply to all future years. But if the death rates decline in 2021, then any period life expectancies calculated for 2021 would most likely be higher. And that’s certainly the hope, given that a large portion of the population has received a vaccine, which is already resulting in a dramatic decline in new infections and hospitalizations.

If you’ve survived the pandemic with your health relatively intact and if you’ve also received the vaccine, then it’s highly likely the virus won’t shorten your lifespan. Of course, new deadly variants or future deadly viruses could change that conclusion, but for now, the outlook is positive.

“Cohort life expectancies” on the other hand, are calculated for a group of people reflecting their characteristics and the experience they might expect over their lifetimes. These life expectancies are calculated in the same way as period life expectancies, except that the death rates used to estimate someone’s remaining future years are modified to reflect anticipated future changes in death rates. If you want to estimate your own remaining lifespan, a cohort life expectancy is often most appropriate.

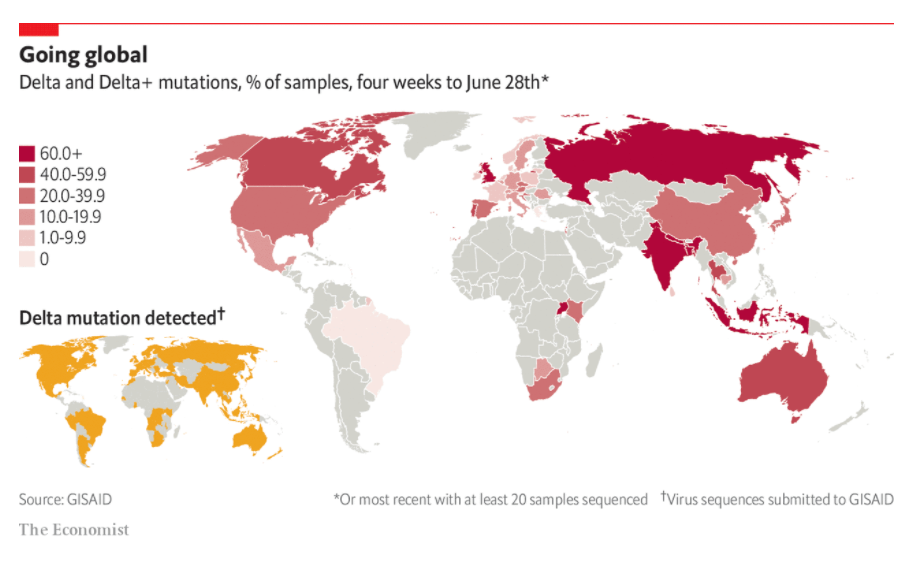

AT A PRESS conference at the White House on June 22nd Anthony Fauci, the director of America’s National Institute of Allergy and Infectious Diseases, issued a warning. The delta variant of the SARS-CoV-2 virus, first identified in India in February, was spreading in America—and quickly. “The delta variant is currently the greatest threat in the US to our attempt to eliminate covid-19,” declared Dr Fauci. Boris Johnson, Britain’s prime minister, issued a similar warning a week earlier. To contain the rapid spread of the variant, European countries and Hong Kong have tightened controls on travellers from Britain.

According to GISAID, a data-sharing initiative for corona- and influenza-virus sequences, the delta variant has been identified in 78 countries (see chart). The mutation is thought to be perhaps two or three times more transmissible than the original virus first spotted in Wuhan in China in 2019. It is rapidly gaining dominance over others. According to GISAID’s latest four-week average, it represents more than 85% of sequenced viruses in Bangladesh, Britain, India, Indonesia and Russia. It may soon be the most prevalent strain in America, France, Germany, Italy, Mexico, South Africa, Spain and Sweden. (GISAID does not, in its summary data, distinguish between delta, B.1.617.2, and the “delta plus” mutation, AY.1, AY.2.)

A state judge refused to block distribution of Harvey, Illinois’ share of American Rescue Plan Act federal coronavirus aid relief funds after rejecting a pension fund’s claim to the money.

The financially stressed Chicago suburb, which has battled over the last decade with its public safety pension funds, Chicago, and bondholders over its obligations, settled a legal dispute in 2018 with its police and firefighters’ pension funds over past due payments. The settlement gives the funds a share of various funding that flows through the state government.

The firefighters’ fund recently sued Harvey to stake a claim to the ARPA money, arguing it is subject to the 10% claim on city tax and aid funds that are sent directly to the pension fund under the 2018 settlement. The fund asked the court to enjoin Comptroller Susana Mendoza, whose office manages the state’s pension intercept program, from distributing any funds until the case was argued.

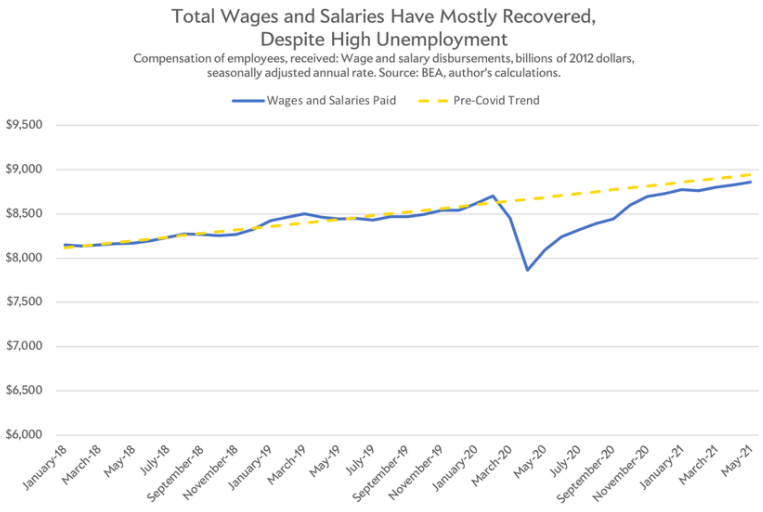

But there are good reasons to be upbeat about the answer. For starters, households saved record amounts of money while they were stuck at home in 2020, which suggests they still have pent-up spending power. Second, Americans have mostly recovered their collective earning power. Total wages and salaries quietly reached a new peak in May, and are trailing less than 1 percent behind their pre-plague trend. Pay has bounced back faster than employment, because the country’s missing jobs are largely concentrated in lower-wage service industries like hospitality.

The January report by former SEC Chairman Harvey Pitt lays bare deep divisions within the Public Company Accounting Oversight Board, which oversees the audits of companies valued in total at trillions of dollars.

It also alleges organizational dysfunction. There were no records documenting the rationale for several staff firings, and confusion about the roles of the PCAOB’s board members has “created some dysfunctional behavior” by them, the report found.

Current SEC Chairman Gary Gensler this month ousted William Duhnke as PCAOB chairman and is replacing the rest of the five-member board.

A PCAOB spokeswoman didn’t return a request for comment. An SEC spokesman declined to comment. Mr. Duhnke said he hasn’t seen the report and cannot comment on it.

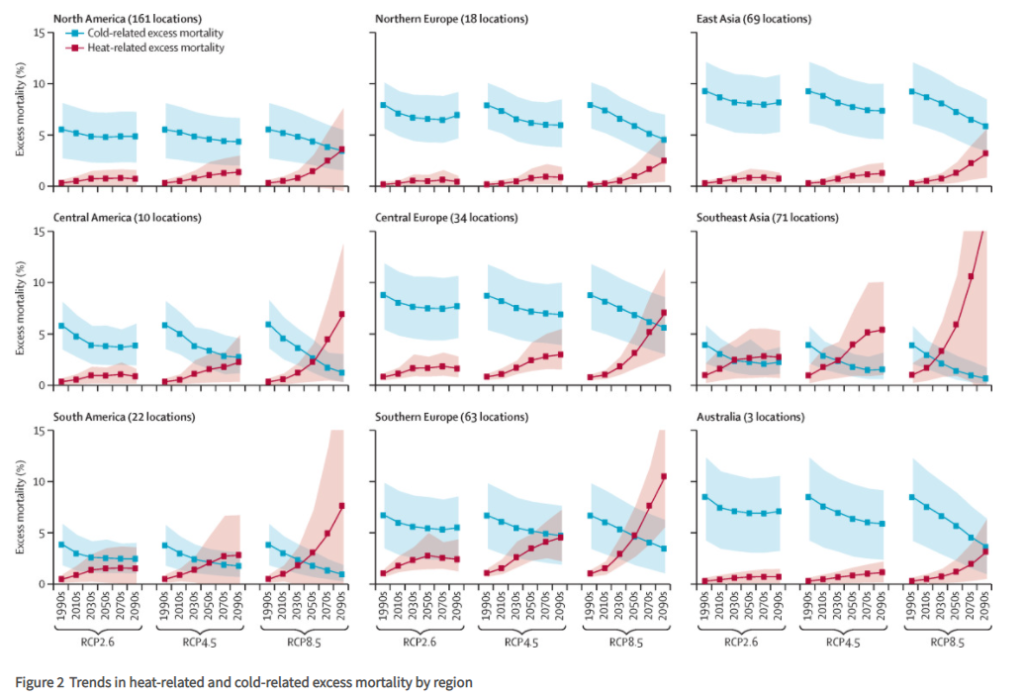

Our dataset comprised 451 locations in 23 countries across nine regions of the world, including 85 879 895 deaths. Results indicate, on average, a net increase in temperature-related excess mortality under high-emission scenarios, although with important geographical differences. In temperate areas such as northern Europe, east Asia, and Australia, the less intense warming and large decrease in cold-related excess would induce a null or marginally negative net effect, with the net change in 2090–99 compared with 2010–19 ranging from −1·2% (empirical 95% CI −3·6 to 1·4) in Australia to −0·1% (−2·1 to 1·6) in east Asia under the highest emission scenario, although the decreasing trends would reverse during the course of the century. Conversely, warmer regions, such as the central and southern parts of America or Europe, and especially southeast Asia, would experience a sharp surge in heat-related impacts and extremely large net increases, with the net change at the end of the century ranging from 3·0% (−3·0 to 9·3) in Central America to 12·7% (−4·7 to 28·1) in southeast Asia under the highest emission scenario. Most of the health effects directly due to temperature increase could be avoided under scenarios involving mitigation strategies to limit emissions and further warming of the planet.

Author(s):

Antonio Gasparrini, PhD Yuming Guo, PhD Francesco Sera, MSc Ana Maria Vicedo-Cabrera, PhD Veronika Huber, PhD Prof Shilu Tong, PhD Micheline de Sousa Zanotti Stagliorio Coelho, PhD Prof Paulo Hilario Nascimento Saldiva, PhD Eric Lavigne, PhD Patricia Matus Correa, MSc Nicolas Valdes Ortega, MSc Haidong Kan, PhD Samuel Osorio, MSc Jan Kyselý, PhD Aleš Urban, PhD Prof Jouni J K Jaakkola, PhD Niilo R I Ryti, PhD Mathilde Pascal, PhD Prof Patrick G Goodman, PhD Ariana Zeka, PhD Paola Michelozzi, MSc Matteo Scortichini, MSc Prof Masahiro Hashizume, PhD Prof Yasushi Honda, PhD Prof Magali Hurtado-Diaz, PhD Julio Cesar Cruz, MSc Xerxes Seposo, PhD Prof Ho Kim, PhD Aurelio Tobias, PhD Carmen Iñiguez, PhD Prof Bertil Forsberg, PhD Daniel Oudin Åström, PhD Martina S Ragettli, PhD Prof Yue Leon Guo, PhD Chang-fu Wu, PhD Antonella Zanobetti, PhD Prof Joel Schwartz, PhD Prof Michelle L Bell, PhD Tran Ngoc Dang, PhD Prof Dung Do Van, PhD Clare Heaviside, PhD Sotiris Vardoulakis, PhD Shakoor Hajat, PhD Prof Andy Haines, FMedSci Prof Ben Armstrong, PhD

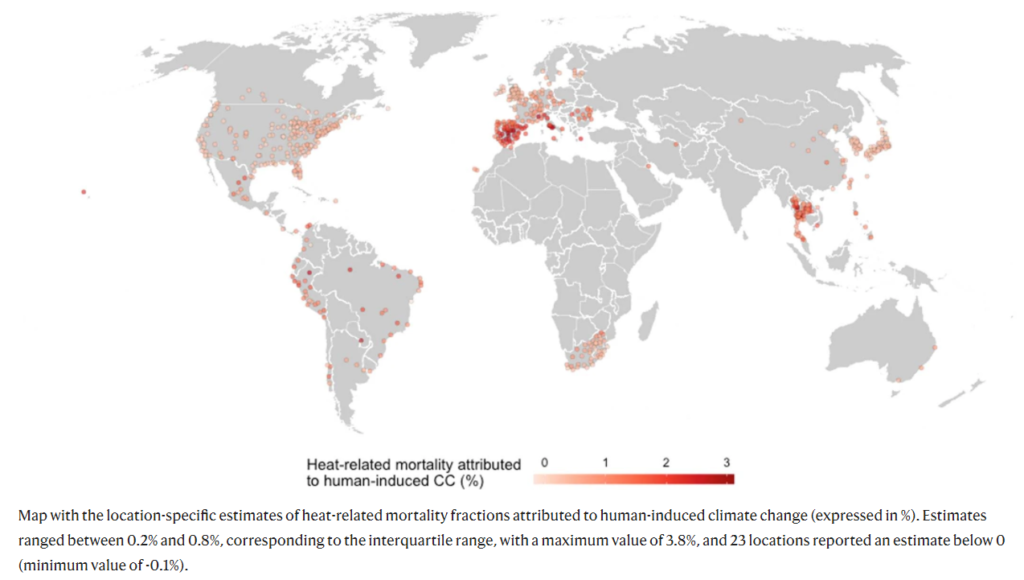

Climate change affects human health; however, there have been no large-scale, systematic efforts to quantify the heat-related human health impacts that have already occurred due to climate change. Here, we use empirical data from 732 locations in 43 countries to estimate the mortality burdens associated with the additional heat exposure that has resulted from recent human-induced warming, during the period 1991–2018. Across all study countries, we find that 37.0% (range 20.5–76.3%) of warm-season heat-related deaths can be attributed to anthropogenic climate change and that increased mortality is evident on every continent. Burdens varied geographically but were of the order of dozens to hundreds of deaths per year in many locations. Our findings support the urgent need for more ambitious mitigation and adaptation strategies to minimize the public health impacts of climate change.

Vicedo-Cabrera, A.M., Scovronick, N., Sera, F. et al. The burden of heat-related mortality attributable to recent human-induced climate change. Nat. Clim. Chang.11, 492–500 (2021). https://doi.org/10.1038/s41558-021-01058-x

Author(s): A. M. Vicedo-Cabrera, N. Scovronick, A. Gasparrini

Earlier this month, a landmark study in Nature made headlines around the world. Rising temperatures from global warming increase the number of heat deaths, now causing a third of all heat deaths, or about 100,000 deaths per year.

Obviously, this is a powerful narrative to justify urgent climate policies.

But the study left out glaring truths that even its own authors have abundantly documented. Heat deaths are declining in countries with good data, likely because of ever more air conditioning. This is abundantly clear for the US, which has seen increasing hot days since 1960 affecting a much greater population. Yet, the number of heat deaths has halved. So while global warming could result in more heat deaths, technological development in, for instance, the US, is actually resulting in fewer heat deaths.