Link: https://www.cnbc.com/2024/09/18/fed-cuts-rates-september-2024-.html

Graphic:

Excerpt:

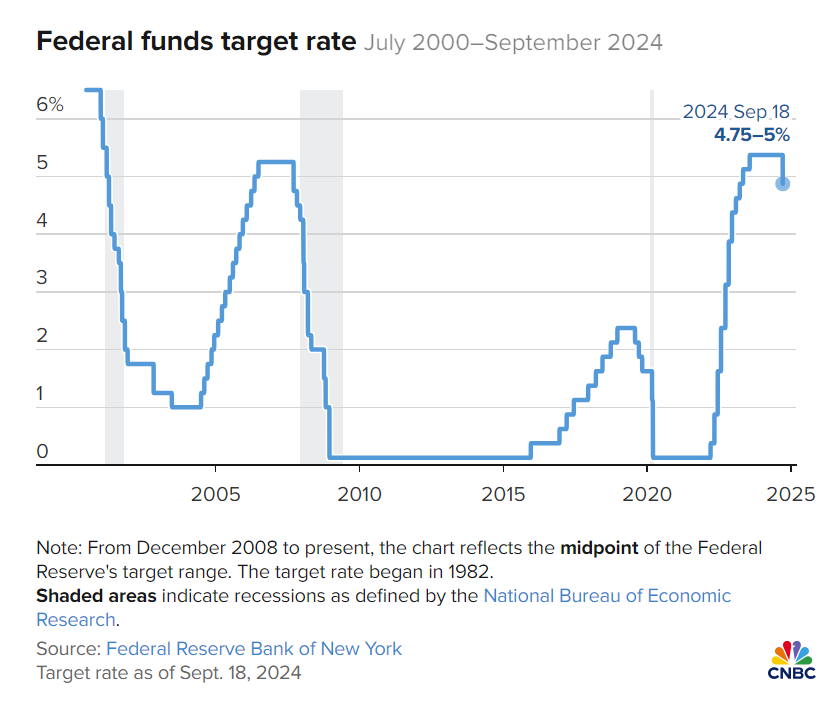

WASHINGTON – The Federal Reserve on Wednesday enacted its first interest rate cut since the early days of the Covid pandemic, slicing half a percentage point off benchmark rates in an effort to head off a slowdown in the labor market.

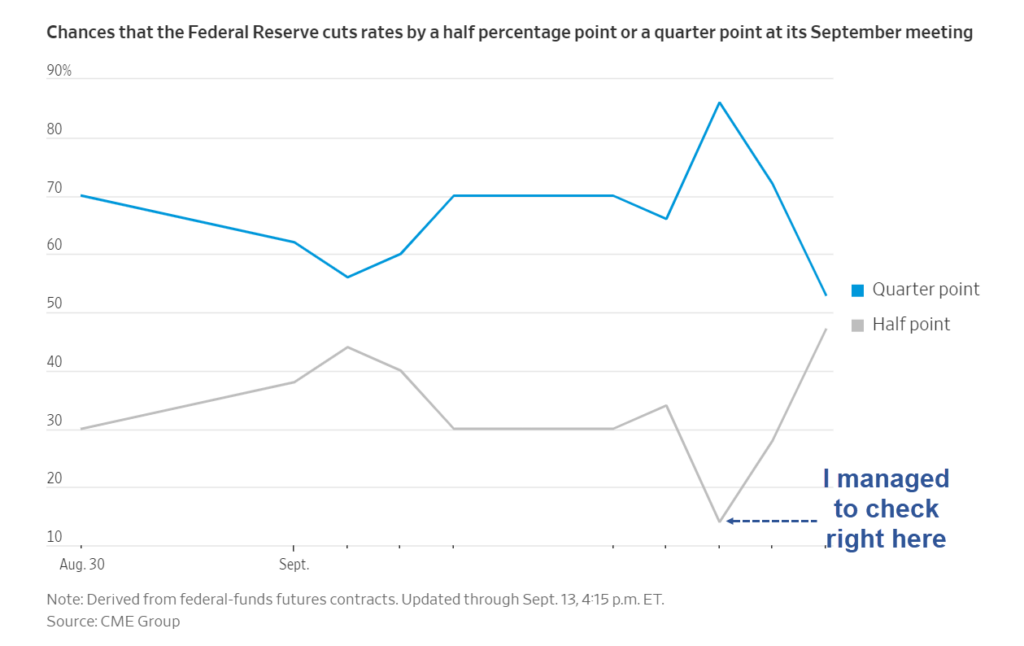

With both the jobs picture and inflation softening, the central bank’s Federal Open Market Committee chose to lower its key overnight borrowing rate by a half percentage point, or 50 basis points, affirming market expectations that had recently shifted from an outlook for a cut half that size.

Outside of the emergency rate reductions during Covid, the last time the FOMC cut by half a point was in 2008 during the global financial crisis.

The decision lowers the federal funds rate to a range between 4.75%-5%. While the rate sets short-term borrowing costs for banks, it spills over into multiple consumer products such as mortgages, auto loans and credit cards.

In addition to this reduction, the committee indicated through its “dot plot” the equivalent of 50 more basis points of cuts by the end of the year, close to market pricing. The matrix of individual officials’ expectations pointed to another full percentage point in cuts by the end of 2025 and a half point in 2026. In all, the dot plot shows the benchmark rate coming down about 2 percentage points beyond Wednesday’s move.

Author(s): Jeff Cox

Publication Date: 18 Sept 2024

Publication Site: CNBC