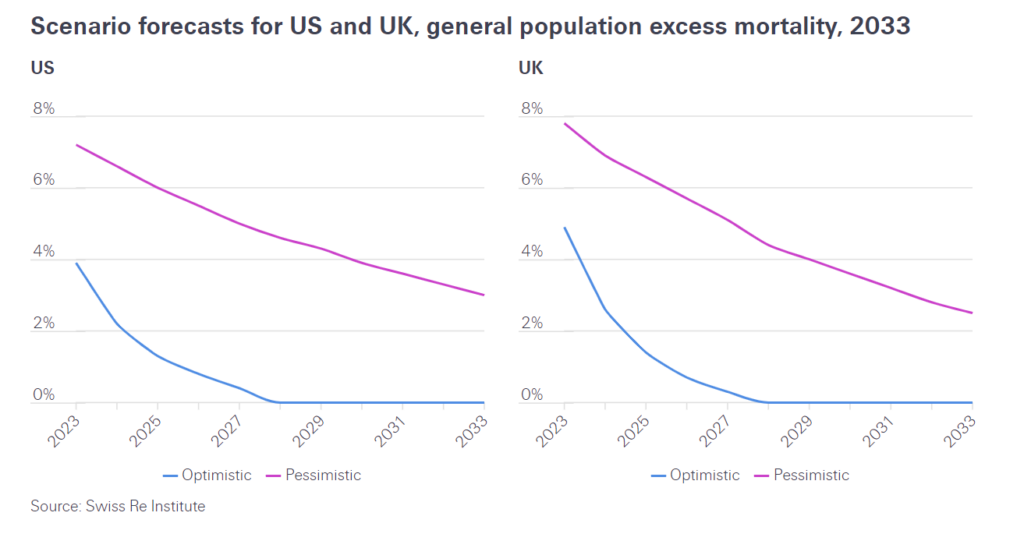

Four years on from the outbreak of the pandemic in 2020, many countries worldwide still report elevated deaths in their populations. This impact appears generally independent of healthcare systems and population health. This trend is evident even after accounting for shifting population sizes, and the range of reporting mechanisms and death classifications that make inter-country comparisons complex. There is also likely a degree of excess mortality under-reporting.

Quantifying excess mortality has been an acute challenge since 2020 due to the exceptional mortality rates of the pandemic. Excess mortality refers to the number of deaths over and above an assumed “expected” number of deaths. The different methods of estimating expected mortality can generate very different excess mortality rates.

This represents a potential challenge for Life and Health (L&H) insurance, with potentially several years of elevated mortality claims ahead, depending on how general population trends translate into the insured population. Ongoing excess mortality can have implications for L&H insurance claims and reserves. Excess mortality that continues to exceed current expectations may affect the long-term performance of in-force life portfolios as well as the pricing of new life policies.

Author(s): By Daniel Meier, Life & Health R&D Manager, CUO L&H Reinsurance & Prachi Patkee, Life & Health R&D Analyst, CUO L&H Reinsurance & Adam Strange, Life & Health R&D Manager, CUO L&H Reinsurance

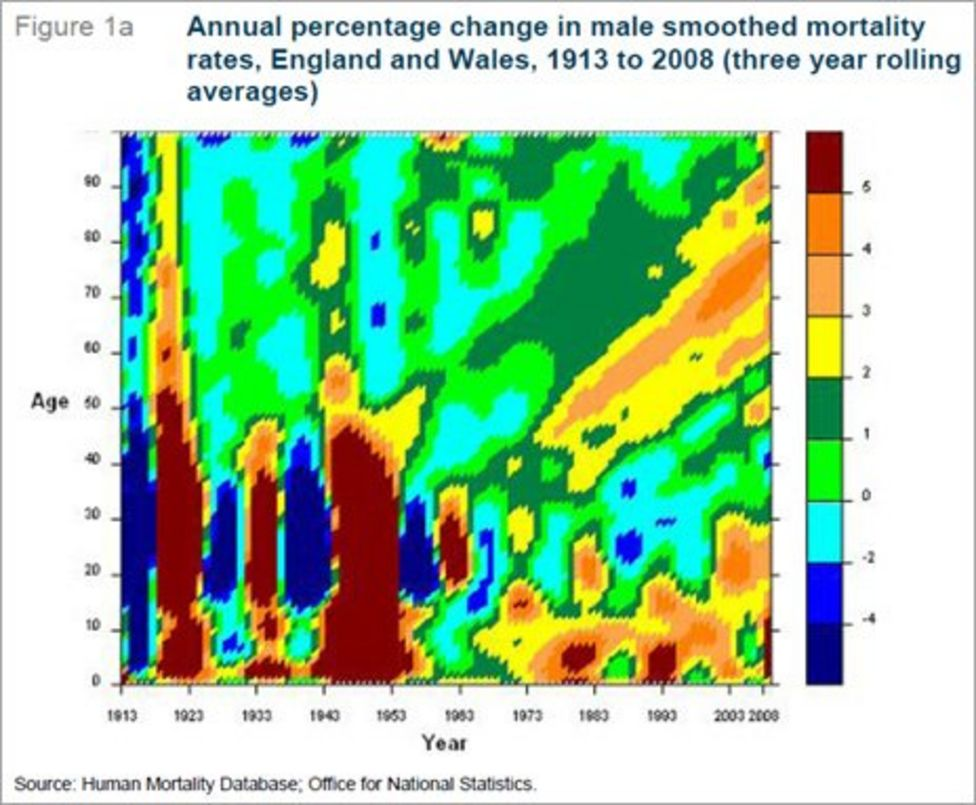

The life experience of British people born between the years 1925 and 1934 has long had demographers and insurance companies scratching their heads.

For reasons which remain unclear, individuals within this slice of the UK population have been living longer and healthier lives than groups both older and younger.

One tool used to track the golden cohort is a heat chart which, in this case, looks at annual mortality improvements for men and women. It takes a bit of explaining, but the diagrams reflect the social history of Britain over the last century or so.

Starting with men (Figure 1a), the most obvious feature of the heat chart are the vertical bands of blue and brown in the bottom left corner. Blue represents worsening mortality and brown improving, so the blue slice closest furthest to the left is the cohort decimated by World War I and the influenza pandemic.

The Post Office had prosecution powers and, between 1999 and 2015, it prosecuted 700 sub-postmasters and sub-postmistresses – an average of one a week – based on information from a computer accounting system called Horizon. Another 283 cases were brought by other bodies including the Crown Prosecution Service.

Some went to prison for false accounting and theft. Many were financially ruined, even though they had repeatedly highlighted problems with the software.

After 20 years, campaigners won a legal battle to have their cases reconsidered. To date only 93 convictions have been overturned. Under government plans, victims will be able to sign a form to say they are innocent, in order to have their convictions overturned and claim compensation.

….

Horizon was introduced by the Post Office in 1999. The system was developed by the Japanese company Fujitsu, for tasks like accounting and stocktaking.

Sub-postmasters complained about bugs in the system after it falsely reported shortfalls – often for many thousands of pounds.

Some attempted to plug the gap with their own money, as their contracts stated that they were responsible for any shortfalls. Many faced bankruptcy or lost their livelihoods as a result.

Lib Dem leader Sir Ed Davey is among several politicians who have faced questions, as he was postal affairs minister in the coalition government. He said he regretted not asking “tougher questions” of Post Office managers, describing what had happened as “dreadful”.

The inquiry is hearing from Post Office investigators, Fujitsu, civil servants and others.

Author(s): By Kevin Peachey, Michael Race & Vishala Sri-Pathma

Many countries, including the UK, have continued to experience an apparent excess of deaths long after the peaks associated with the COVID-19 pandemic in 2020 and 2021. Numbers of excess deaths estimated in this period are considerable. The UK Office for National Statistics (ONS) has calculated that there were 7.2% or 44,255 more deaths registered in the UK in 2022 based on comparison with the five-year average (excluding 2020). This persisted into 2023 with 8.6% or 28,024 more deaths registered in the first six months of the year than expected. The Continuous Mortality Investigation (CMI) found a similar excess (28,500 deaths) for the same period using different methods. Several methods can be used to estimate excess deaths, each with limitations which should be considered in interpretation, however the overall trends tend to be consistent across the various methods.

The causes of these excess deaths are likely to be multiple and could include the direct effects of Covid-19 infection, acute pressures on NHS acute services resulting in poorer outcomes from episodes of acute illness, and disruption to chronic disease detection and management. Further analysis by cause and by age- and sex-group may help quantify the relative contributions of these causes.

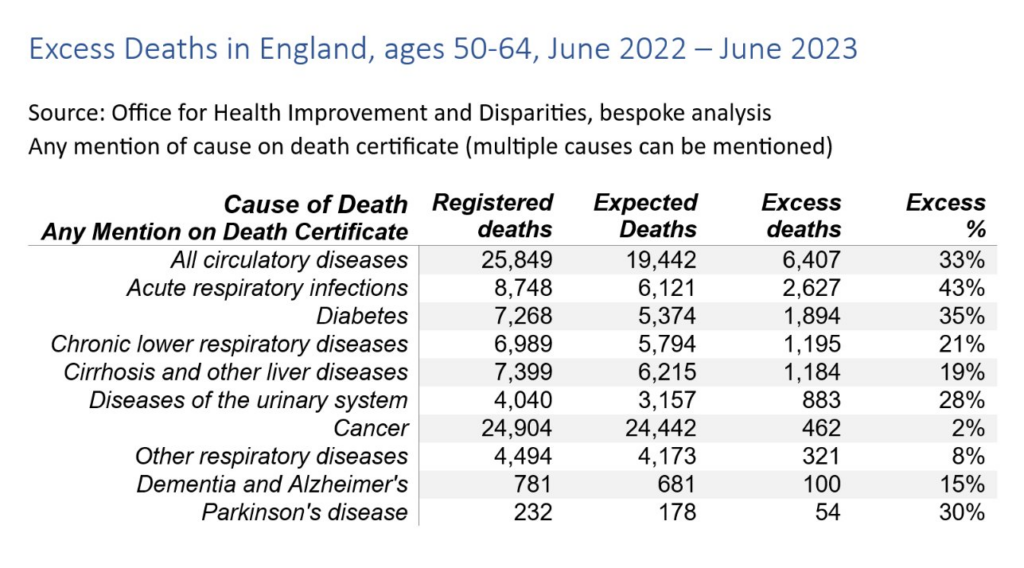

Since July 2020, the Office for Health Improvement and Disparities (OHID) has published estimates of excess mortality based on a Poisson regression model for England week by week, overall and decomposed by age, ethnicity, region and cause. This model finds that in the period from week ending 3rd June 2022 to 30th June 2023, excess deaths for all causes were relatively greatest for 50–64 year olds (15% higher than expected), compared with 11% higher for 25–49 and < 25 year olds, and about 9% higher for over 65 year old groups. While the median age of these groups has changed since 2020, age-standardised mortality analysis breaking down death rates by sex find clearer age differences still. The age-standardised CMI found similar patterns with the largest relative excess deaths for 2022 observed in young (20–44 years) and middle-aged (45–64 years) adults. These findings should be interpreted carefully because of greater than usual delay in registration of deaths in the latter part of 2022.

Several causes, including cardiovascular diseases, show a relative excess greater than that seen in deaths from all-causes (9%) over the same period (week ending 3rd June 2022–30th June 2023), namely: all cardiovascular diseases (12%), heart failure (20%), ischaemic heart diseases (15%), liver diseases (19%), acute respiratory infections (14%), and diabetes (13%).

For middle-aged adults (50–64) in this 13-month period, the relative excess for almost all causes of death examined was higher than that seen for all ages. Deaths involving cardiovascular diseases were 33% higher than expected, while for specific cardiovascular diseases, deaths involving ischaemic heart diseases were 44% higher, cerebrovascular diseases 40% higher and heart failure 39% higher. Deaths involving acute respiratory infections were 43% higher than expected and for diabetes, deaths were 35% higher. Deaths involving liver diseases were 19% higher than expected for those aged 50–64, the same as for deaths at all ages.

Looking at place of death, from 3rd June 2022 to 30th June 2023 there were 22% more deaths in private homes than expected compared with 10% more in hospitals, but there was no excess in deaths in care homes and 12% fewer deaths than expected in hospices. For deaths involving cardiovascular diseases the relative excess in private homes was higher than all causes at 27%. Deaths in hospital were 8% higher and deaths in care homes only 3% higher.

The greatest numbers of excess deaths in the acute phase of the pandemic were in older adults. The pattern now is one of persisting excess deaths which are most prominent in relative terms in middle-aged and younger adults, with deaths from CVD causes and deaths in private homes being most affected. Timely and granular analyses are needed to describe such trends and so to inform prevention and disease management efforts. Leveraging such granular insights has the potential to mitigate what seems to be a continued and unequal impact on mortality, and likely corresponding impacts on morbidity, across the population.

Author(s): Jonathan Pearson-Stuttard Sarah Caul Stuart McDonald Emily Whamond John N. Newton

Publication Date: 1 Dec 2023

Publication Site: The Lancet Regional Health Europe

However, a second tab in the spreadsheet contained multiple entries in relation to more than 10,000 individuals. For each individual, there are 32 pieces of data meaning that in total, there are about 345,000 pieces of data in the file.

The spreadsheet, which has been seen by the Belfast Telegraph after we were alerted to it by a relative of a serving officer, includes each officer’s service number, their status, their gender, their contract type, their last name and initials, details of how much of the week they work, and their rank.

It also includes the location where they are based (but not their home address), their duty type (from chief constable to detective, intelligence officer and so on), details of their unit (such as the anti-corruption unit or the vetting department), their branch and department, and other technical information about their employment.

There are 10,799 entries in the database. There are 9,276 police officers and police staff. It is not clear if the additional entries relate to other employees or former employees.

The data has been removed from the internet.

There are details of staff who are suspended, on career breaks, or partly retired.

It reveals members of the organised crime unit, telecom liaison officers, intelligence officers stationed at ports and airports, PSNI pilots in its air support unit, officers in the surveillance unit and – of acute sensitivity – almost 40 PSNI staff based at MI5’s headquarters in Holywood.

There are a tiny number of individuals whose unit is given as “secret”. But although that does not disclose precisely what they do, it marks them out as operating in an acutely sensitive area – and then gives their name.

Whoever you decide to vote for, please do take the time to engage with the election process, consider what each candidate can contribute to move the profession forwards, and whether you want an active council or a passive council: make your vote count for the sake of your profession.

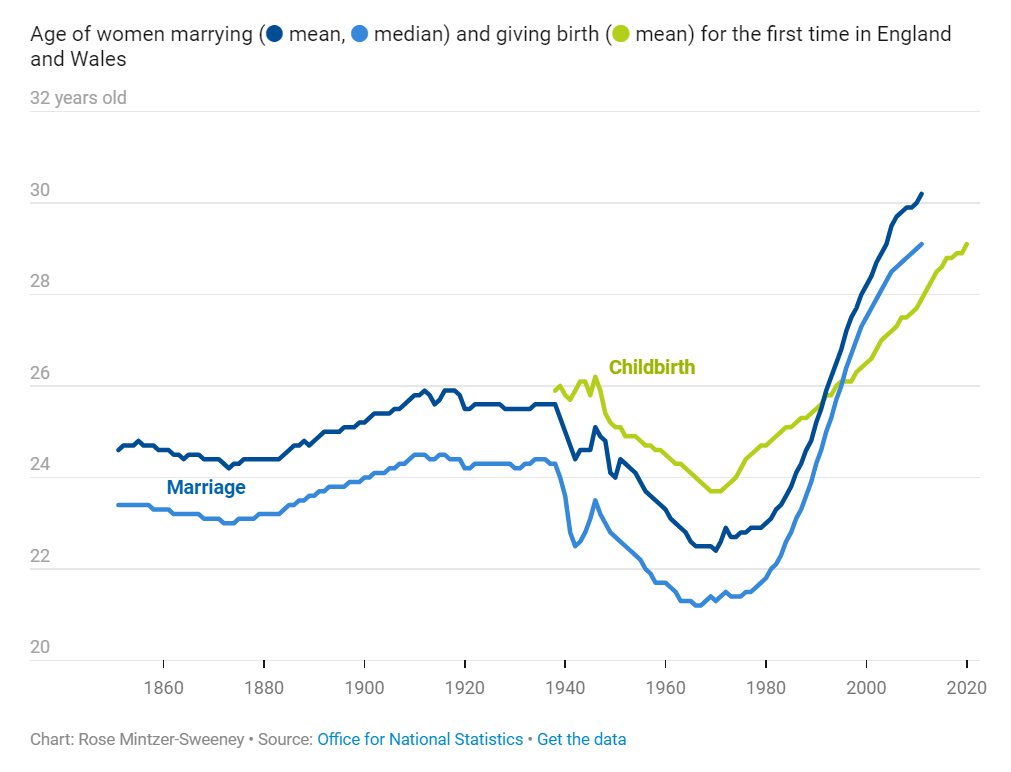

In the previous Weekly Chart, Elliot brought the data to confirm a commonsense impression: people these days are waiting later than their parents and grandparents did to get married and have children. The average age of a newlywed in the U.K. is 30.6 for women and 32.1 for men — about five years older than they would have been 1995, and nine years older than in 1964.

When we’re looking back in history, three generations is about as far as common sense can usually go. Those are the people whose lives we know firsthand. Many of us might have a general impression that women, especially, married young in the past, but we don’t actually have any 19th century friends or family to compare that impression against. Reading last week’s post, I was curious to see the older data that could fill in that gap.

Cite: JAMA Intern Med. Published online February 27, 2023. doi:10.1001/jamainternmed.2023.0015

Graphic:

Excerpt:

Question What is the association of cardiovascular health (CVH) levels, estimated by the American Heart Association’s Life’s Essential 8 score, with life expectancy free of major chronic diseases?

Findings In this cohort study of 135 199 adults from the UK Biobank study, high CVH level was associated with substantially longer life expectancy free of 4 major chronic diseases (cardiovascular disease, diabetes, cancer, and dementia) in both men and women. Furthermore, the disease-free life expectancy was similar between low and other socioeconomic groups among participants with high CVH.

Meaning These findings support improvement in population health by promoting a high CVH level, which may also narrow health disparities associated with socioeconomic status.

Author(s): Xuan Wang, MD, PhD1; Hao Ma, MD, PhD1; Xiang Li, MD, PhD1; et al

The CMI has issued its consultation to help shape the next version of its mortality projection model, which is used by the majority of pension scheme trustees and sponsors in setting their funding and accounting assumptions. The consultation focuses on how to respond to the very high mortality rates seen in England & Wales over 2022, to which the model is calibrated.

The CMI believe mortality in 2022 may be indicative of future mortality to some extent, unlike the exceptional mortality seen in 2020 and 2021 during the peak of the pandemic.

The key proposal is to give 25% weight to the 2022 mortality data. In the coming years, the CMI plan to steadily increase the weight on mortality data until around 2025, by which time it expects a clearer indication of mortality trends of the future. The CMI also intend to update the model to use the latest population estimates based on the 2021 Census.

Both of these changes reduce projected life expectancy relative to previous versions of the model.

Chris Tavener, Partner and Head of Life Analytics commented: “If these proposals go ahead then life expectancy assumptions at age 65 are likely to fall by around 6 months, equivalent to 2%, when adopting the new core model, all else being equal. This is a larger fall in life expectancies compared to recent model updates, but we share the concern expressed by the CMI that higher death rates seen in the latter part of 2022, and continuing into January, may be indicative of future mortality.

“We are seeing an increasing number of pension scheme trustees and sponsors look to us to understand how their own members are likely to be affected by the various factors driving recent higher death rates, such as the ramifications of the pandemic and pressures on the healthcare system, which in our view will affect some groups more than others.”

The Charitable Corporation was established in London in 1707 with the noble mission of providing “relief of the industrious poor by assisting them with small sums at legal interest.”

Essentially, it sought to provide low-interest loans to poor tradesmen, shielding them from predatory pawnbrokers who charged as much as 30% interest. The corporation made loans available at the rate of 5% in return for a pledge of property for security.

The Charitable Corporation was modeled on Monti di Pietà, a charitable institution of credit established in Catholic countries during the Renaissance era to combat usury, or high rates of interest.

Unlike the Monti di Pietà, however, the British version – despite its name – wasn’t a nonprofit. Instead, it was a business venture. The enterprise was funded by offering shares to investors who, in return, would make money while doing good. Under its original mission, it was like an 18th century version of today’s socially responsible investing, or “sustainable investment funds.”

….

There are several key characteristics that stand out in the collapses of both the Charitable Corporation and FTX. Both companies were offering something new or venturing into a new sector. In the former’s case, it was microloans. In FTX’s case, it was cryptocurrency.

Meanwhile, the management of both ventures was centralized in the hands of just a few people. The Charitable Corporation got into trouble when it reduced its directors from 12 to five and when it consolidated most of its loan business in the hands of one employee – namely, Thomson. FTX’s example is even more extreme, with founder Sam Bankman-Fried calling all the shots.

Raising interest rates won’t just push Britain into a recession and make the cost-of-living crisis worse for working-class people — it will discourage badly needed investments in green energy, undermining the UK’s efforts to address climate change.

….

The theory goes that higher interest rates help bring inflation down by making credit more expensive across the economy and reducing the amount of money firms and families have to spend on goods and services, thereby slowing price increases. But our inflation is predominantly driven by external factors, most notably high gas prices resulting from COVID-19 supply issues and the war in Ukraine. Instead, the bank’s policy is likely to push the UK economy into a recession, without addressing the main underlying causes of rising prices. That also means higher costs of borrowing for the very investments we need to reduce our reliance on costly fossil gas, like wind farms and home insulation.

To compound the problem, higher interest rates discourage investment in clean projects more than dirty ones. Running renewables doesn’t cost much: they rely on free wind and solar energy instead of expensive fossil fuels. But building them in the first place does come with high initial costs, meaning they are particularly impacted by the higher costs of credit. Similarly, insulation and heat pumps need to be paid for up front, before they begin to lower energy bills for households. Demand for improvements like heat pumps is significantly influenced by the availability of cheap loans to cover the initial installation costs.