Ken Griffin, founder and CEO of Citadel, spoke in his Chicago office to Editorial Page Editor Chris Jones on Aug. 2. This transcript has been edited for length.

Gov. J.B. Pritzker has said you and he met privately and that you agreed to drop your opposition to his graduated tax proposal if he took on pension reform in Illinois. True?

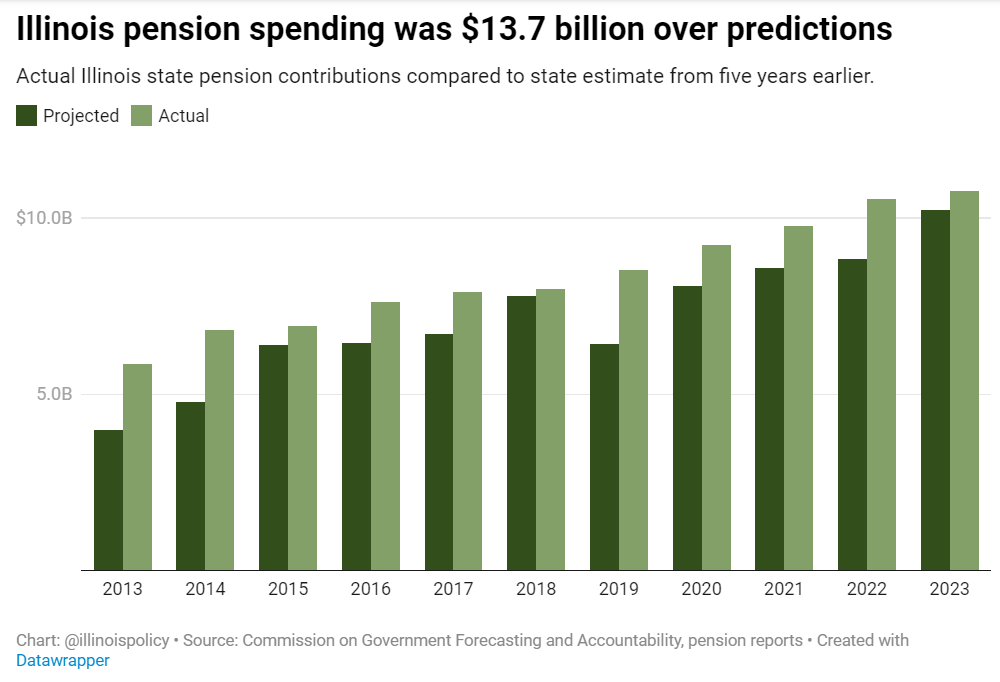

The Illinois pension crisis is rooted in the issue that politicians of the moment are able to make promises to the public sector workers, where the cost of those promises are borne by taxpayers, far into the future. So we have an intrinsic lack of accountability within the state when it comes to that dynamic between the leaders in Springfield and the public sector unions. (Former Gov.) Bruce Rauner and I actually would speak about this problem from time to time because it’s pretty well known that Bruce felt the state should move to a defined contribution program for the state employees.

And there are elements of that I think are attractive, but because the state employees do not participate in Social Security, a strictly defined contribution proposal leaves the state employee, in my opinion, at undue risk of adverse events if they do not invest their money successfully. … And there’s another issue, which is that the costs of the promises made by cities and counties are not borne by the cities and counties directly, they’re socialized across the entire taxpayer base of the state. So it’s pretty easy for the behavior of a number of Illinois cities to offer incredible increases in pay in final years to boost pension benefits, and that cost comes back to all Illinois taxpayers.

So these are some of the areas in which the average man in the street is really being handed a very significant bill. And the most tragic part of this whole story is that when the state hires people early in their careers, they’re not even placing that much value on these pension plans.

Twenty-two-year-olds don’t make lifetime career decisions on pension benefits. So, from my perspective, as a state we’re much better off having higher starting salaries to attract really good people to serve in the public sector. And, as with Bruce, my advice to the governor was consistently that either the state should mirror the benefits of Social Security as a baseline or, even better, go back to the federal government and get into Social Security again. We should reverse our opt-out from decades ago. And then to the extent that a city wants to offer benefits in excess of the Social Security baseline amount, that’s pay-as-you-go through a 401(k)-equivalent program. …

The proposal that I gave to J.B. to solve the state’s pension problems is exactly what I just shared with you. … It would, in all likelihood, require us to amend the constitution for the state to head in this direction. It might be for new employees only. I’m very sensitive to a promise made and earned. That’s your benefit. That’s a very different talking point than you’re 22 years old and it’s your first day working for the state.

But, big picture, we get the state into a program that looks like what I just described. And it’s gonna accelerate, in all likelihood, the costs of the current system. It may require revenue increases.

And like many of the business leaders in this city, I was very direct. I said, “If you’re willing to engage in pension reform, I’m willing to publicly support you in a tax increase.” It wasn’t graduated versus not graduated. It was just a tax increase.

I would’ve assumed that this meeting would’ve been private for the rest of my life until J.B. decided to open the door and talk about this. What he did talk about in terms of fiscal reform for the state was to restructure the state’s (information technology) budget.

And he felt he could achieve $50 million in budget savings for the state of Illinois by taking an ax toward our IT budget for the state, and that was going to be his victory lap for fiscal discipline in the state of Illinois. Here we have a multibillion-dollar problem on the left and 50 million (dollars) on the right. I was like, “J.B., we’re not having the same conversation here.”

To be clear, that was a fracturing moment between the two of us. … He does not want to use his political capital for good. He wants to maintain that capital to maintain the certainty of staying in power.