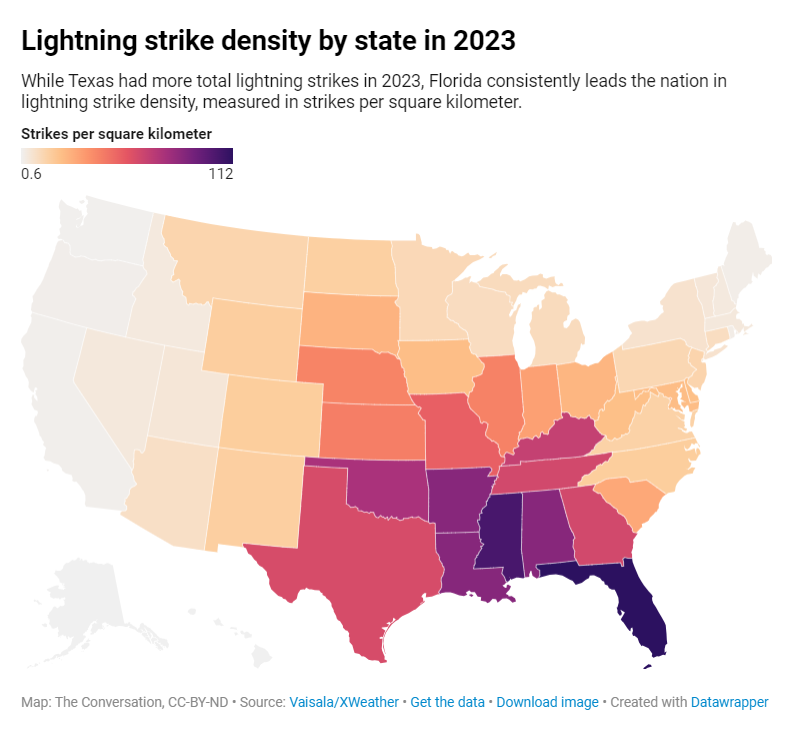

Insurance prices have surged across America in the past two years, with homeowner’s insurance climbing 21%, while CPI rose just 5%. (Source: Bloomberg)

Jerry Theodorou of R Street Institute is interviewed about Florida homeowners insurance.

Most insurance companies at that time assessed hurricane exposure in their portfolios by simply multiplying customer premiums by a rough factor of supposed risk, rather than tracking actual property replacement costs. “They were just very crude formulas,” she said.

So in 1987, Clark had started her own company, Applied Insurance Research, or AIR, to develop software that better estimated the potential losses from catastrophic events. Unlike the rest of the industry, she used granular data and sophisticated analyses, an approach now called catastrophe modeling. Her first computer model estimated that a Category 5 hurricane hitting Dade County could cause losses almost 10 times more than previously believed. She warned her customers about the risk in Florida, but until Hurricane Andrew, no one listened.

Sen. John Kennedy (R–La.) is upset because Sen. Rand Paul (R–Ky.) wants to limit federal flood insurance.

But Paul is right. In my new video, Paul says, “[It] shouldn’t be for rich people.”

That should be obvious. Actually, federal flood insurance shouldn’t be for anyone. Government has no business offering it. That’s a job for the insurance business.

Of course, when actual insurance businesses, with their own money on the line, checked out what some people wanted them to insure, they said, “Heck no! If you build in a dangerous place, risk your own money!”

Politically connected homeowners who own property on the edges of rivers and oceans didn’t like that. They whined to congressmen, crying, “We can’t get insurance! Do something!”

Craven politicians obliged. Bureaucrats at the Federal Emergency Management Agency even claim they have to issue government insurance because, “There weren’t many affordable options for private flood insurance, especially for people living in high-risk places.”

But that’s the point! A valuable function of private insurance is to warn people away from high-risk places.

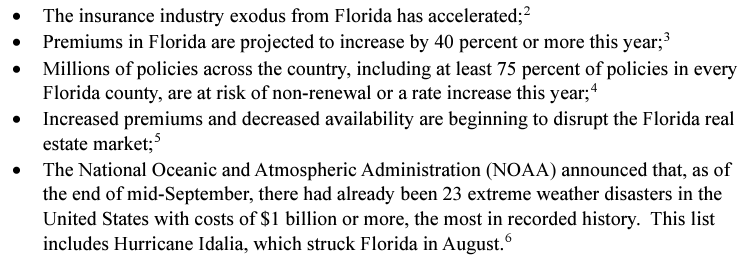

The federal government has launched an investigation into Florida’s largest home insurance company.

Citizens Insurance, the governor, and other state leaders received a letter informing them that a Senate budget committee is looking into the state-run company.

Citizens insure $586 billion worth of property, and they have just over $15 billion in their reserves to pay out on claims. If a major hurricane hit the state, they could be short over $571 billion, leaving everyone in the state on the hook to pay the shortfall.

The letter from the Senate committee investigating the state backed company expresses concern it may be unable to cover its losses. A claim the governor confirmed while visiting Fort Myers last year.

….

Mark Friedlander with the Insurance Information Institute said a private insurer would not be allowed to operate in the State of Florida with those financial dynamics.

Seven private companies went insolvent in the last year and a half in Florida.

“Citizens, unlike a private insurer, could never go insolvent,” Friedlander noted.

That’s because the state could initiate a hurricane tax to cover its costs which would require everyone who owns property or a car to pay a hurricane tax.

As of 2022, Citizens’ market share for homeowners multi-peril policies was approaching 20 percent, having more than doubled since 2020. As private insurers in Florida continue to go insolvent or exit the state, Citizens’ market share will likely continue to grow. At 20 percent market share, Citizens’ losses could be as high as $36 billion in the scenario studied by Swiss Re or $162 billion in the scenario studied by Cambridge and Munich Re (assuming that 60 percent of total losses are insured). If Citizens had to raise $162 billion to cover losses, that would result in an approximately $20,000 assessment for every homeowners insurance policyholder in Florida.

….

To that end, please respond to the following requests for information and documents by December 21, 2023:

1. What modeling or other analysis has Citizens done to estimate its total potential exposure to various worst case hurricane scenarios? What is the upper range of Citizens’ potential losses? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ potential losses.

2. What modeling or other analysis has Citizens done to estimate its market share over the next decade? What does Citizens project its market share to be in each of the next 10 years? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ future market share.

3. What modeling or other analysis has Citizens done to determine its ability to fully pay out claims resulting from various loss scenarios? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ financial position and (in)solvency under such scenarios.

4. What are Citizens’ current assets? What is Citizens’ total reinsurance coverage? What are the maximum total claims Citizens would be able to pay out without having to levy an assessment on Florida policyholders? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ current assets, reinsurance, and ability to pay claims.

5. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Michael Yaworsky, their staffs, or any other state officials regarding Citizens’ current or future solvency? Please provide copies of these communications.

6. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials regarding what Citizens and/or the State would do if Citizens were unable to cover its losses? Please provide copies of these communications.

7. Has Citizens contemplated asking for a federal bailout if it were unable to cover its losses? Has Citizens discussed the possibility of a federal bailout with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials? Please provide copies of these communications.

Craig Allen recently accomplished a personal first as an ecology professor by getting listed on a patent for a fireball-dropping drone.

“For me, because I expect that I will probably never have another patent in my life, because I do science that’s generally not patentable and I really don’t have the capacity for that kind of thing, the patent is fully unique and, thus, will have a special place in my heart,” said Allen, director of the National Science Foundation Research Traineeship at Nebraska.

He worked with agronomy professor Dirac Twidwell, computer science professors Sebastian Elbaum and Carrick Detweiler, and former Nebraska students Christian Laney, James Higgins and Evan Michael Beachly in developing IGNIS, the drone product.

….

At first, the three discussed using drones as a less dangerous way to sample invasive species like zebra mussels in Nebraska waters. Then, when a person was injured on an ATV during a prescribed burn, the three professors turned to discussing using drones in prescribed burns.

Allen said about 40,000 acres of rangeland in Nebraska are invaded by trees every year and fire is the best way to control that.

Typically, firefighters on ATVs or in helicopters carry out prescribed burns, but both methods can be dangerous.

Prescribed burns are a proven way to reduce the impact of destructive wildfires, but they still come with risks to the firefighters who carry them out. That was the impetus behind a project from the National Science Foundation’s National Research Traineeship (NRT) program at the University of Nebraska-Lincoln (UNL) that uses a drone to drop fireballs to ignite prescribed burns, keeping firefighters out of harm’s way.

I spoke to Rex Frazier, president of the Personal Insurance Federation of California, who cited several policies that no doubt contributed to State Farm’s decision to stop issuing policies, including various price controls that prevent insurers from raising prices to meet surging costs without the written approval of the California Department of Insurance.

“California is the only state in the country that doesn’t allow insurers’ rates to be based upon actual reinsurance costs,” Frazier said. “California’s regulations employ a legal fiction that each insurer uses its own capital to serve customers. As reinsurance costs go up, insurers cannot have their rates reflect those higher costs.”

State Farm General Insurance Co. last week became the latest insurer to retreat from California’s homeowners market. The culprit isn’t climate change, as the media claims in parroting Sacramento talking points. The cause is the Golden State’s hostile insurance environment.

The nation’s top property and casualty insurer on Friday said it won’t accept new applications for homeowners insurance, citing “historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market.”

In other words, State Farm can’t accurately price risk and increase its rates to cover ballooning liabilities. Other property and casualty insurers, including AIG and Chubb, have also been shrinking their California footprint after years of catastrophic wildfires, which are becoming more common owing to drought and decades of poor forest management.

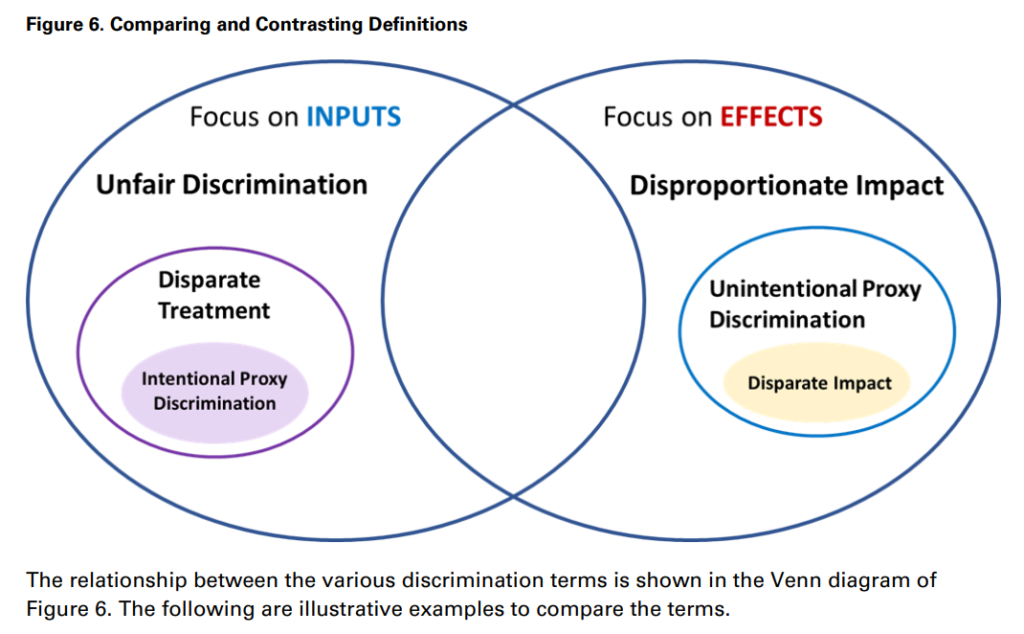

Unfair Discrimination without Disproportionate Impact. As previously defined, unfair discrimination occurs when rating variables that have no relationship to expected loss are used. A hypothetical example could be if an insurer decided to use rating factors that charged those with red cars higher rates, even if the data did not show this. In this case, there would be no disproportionate impact, assuming protected classes do not own a large majority of red cars. Disparate Treatment. Disparate treatment and unfair discrimination are not directly related if we use the Fair Trade Act definition of unfair discrimination. However, in states where rating on protected class is defined to be unfair discrimination, disparate treatment would be a subset of unfair discrimination. In such cases, an insurer would explicitly use protected class to charge higher rates, with the intention of prejudicing against that class. Intentional Proxy Discrimination. If proxy discrimination is defined to require intent, it would be a subset of disparate treatment, whereby an insurer would deliberately substitute a facially neutral variable for protected class for the purpose of discrimination. Redlining is an example of this type of discrimination, given the use of location characteristics as proxies for race and social class. Disproportionate Impact. Disproportionate impact focuses on effect on protected class, even if there is a relationship to expected loss. An example of this is the one mentioned in the AAA study, whereby a rating plan that uses age could disproportionately impact a minority group if those in that minority group tend to have higher risk ages. This disproportionate impact is not necessarily the same as proxy discrimination, since it is likely that even after controlling for minority status, age would have a relationship to expected costs.

Unintentional Proxy Discrimination. If proxy discrimination is defined to be unintentional, the focus is more on disproportionate outcomes and the variables used to substitute for protected class. Several variables are being investigated by regulators to potentially be proxy discrimination and include criminal history for auto insurance rating. In order to prove proxy discrimination, an analysis would have to be performed to understand the extent to which criminal history proxies for minority status, and whether its predictive power would decrease when controlling for protected class. It is important to note once again that terms like “unintentional proxy discrimination” may be subsumed by “disparate impact,” but they are included in this paper to show how various stakeholders use the term differently. Disparate Impact. Disparate impact is unintentional discrimination, where there is disproportionate impact, but also other legal requirements, such as the existence of alternatives. To date, no disparate impact lawsuits against insurance companies have been won. An example of potential disparate impact (although it was not litigated as a lawsuit) is from health care. Optum used an algorithm to identify and allocate additional care to patients with complex healthcare needs. The algorithm was designed to create a risk score for each patient during the enrollment period. Patients above the 97th percentile were automatically enrolled in the program and thus allocated additional care. Upon an independent peer review of the model, researchers found that the model was in fact allocating artificially lower scores to Black patients, even though the model did not use race. The reason behind this was the model’s use of prior healthcare costs as an input. Black patients typically spend less than white patients on health care, which artificially allocated better health to Black patients.18 Unfair Discrimination and Disproportionate Impact. In this case, an insurer would use a variable that both has no relationship to expected loss, but also has an outsized effect on protected classes. An example of this could be the same red car case above, but where protected classes also owned almost all the red cars. In this case, higher rates would create a disproportionate effect on protected classes, while also having no relationship to expected loss.

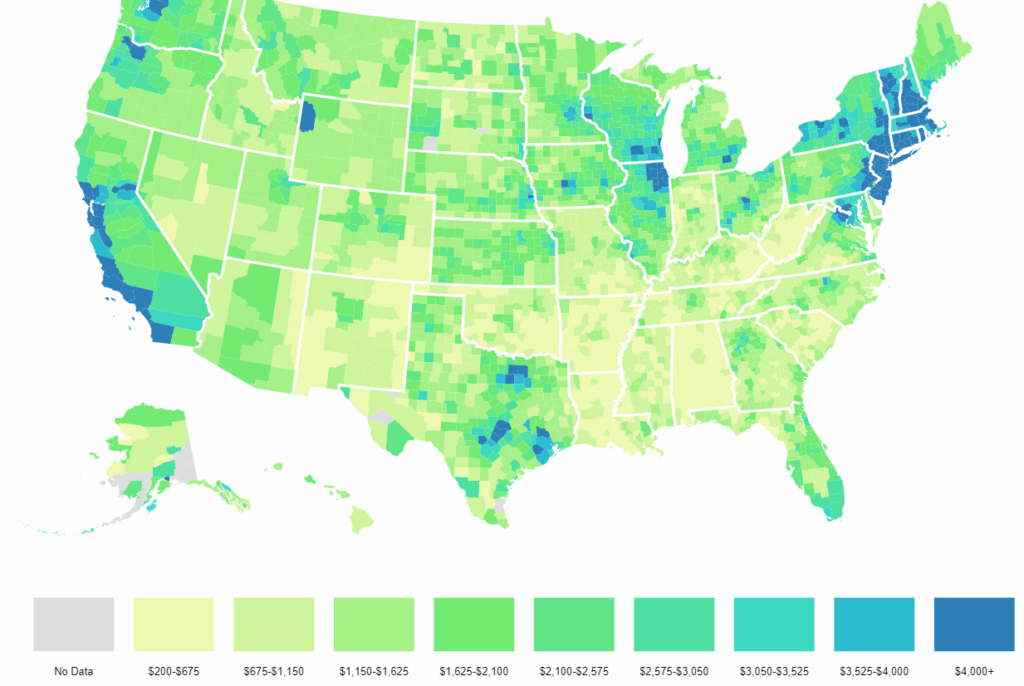

Median property taxes paid vary widely across (and within) the 50 states. The lowest bills in the country are in six counties or county equivalents with median property taxes of less than $200 a year:

Northwest Arctic Borough and the Kusivlak Census Area (Alaska)*

Avoyelles, East Carroll, and Madison (Louisiana)

Choctaw (Alabama)

(*Significant parts of Alaska have no property taxes, though most of these areas have such small populations that they are excluded from federal surveys.)

The next-lowest median property tax of $201 is found in Allen Parish, near the middle of Louisiana, followed by $218 in McDowell County, West Virginia, in the southernmost part of the state.

The eight counties with the highest median property tax payments all have bills exceeding $10,000:

Bergen, Essex, and Union (New Jersey)

Nassau, New York, Rockland, and Westchester (New York)

Falls Church (Virginia)

All but Falls Church are near New York City, as is the next highest, Passaic County, New Jersey ($9,999).