There are many reasons why changes to Social Security are unpopular and potentially harmful. One reason is that raising the retirement age may disproportionately impact low-wage earners. Studies have shown that low-wage earners at the age of 65 have a lower life expectancy than high-wage earners. So raising the full retirement age further due to a longer average life expectancy may force those income brackets with below-average life expectancies to bear the brunt of a difficult policy change.

This impact disparately impacts low earners further because they are more likely to rely on Social Security Benefits for their full income at retirement. High-income earners rely more on private pensions, earned income, or assets. A rise in the retirement age forces low-income earners to either work longer or claim their social security benefits with penalties.

….

One solution is a two-pronged approach that accounts for this: Raise the retirement age while changing the replacement formula. While increasing the retirement age will effectively reduce benefits, raising the replacement formula for the lowest bracket and reducing it for the middle- and upper-income brackets would allow low-income retirees to claim benefits at the current retirement age and receive current benefits if needed. This would also allow the biggest cuts to social security benefits to fall on those with other means for funding their retirement.

Workers born after 1970 have been told they need to keep going for another three years — and many are not happy

Denmark has raised its retirement age to 70 for everyone born after 1970, becoming the first European country to reach the symbolic threshold.

While other nations are bogged down in seemingly intractable political battles over increasing the state pension age, the Danes are following a long-established principle that it should go up broadly in line with life expectancy. The average for Danes is 81.7 years. The legislation was passed with an overwhelming majority in the Danish parliament.

However, there is a good deal of public unease at the plan to oblige many people to keep working until the end of their seventh decade. Some MPs look aghast at projections that the retirement age could rise as high as 77.

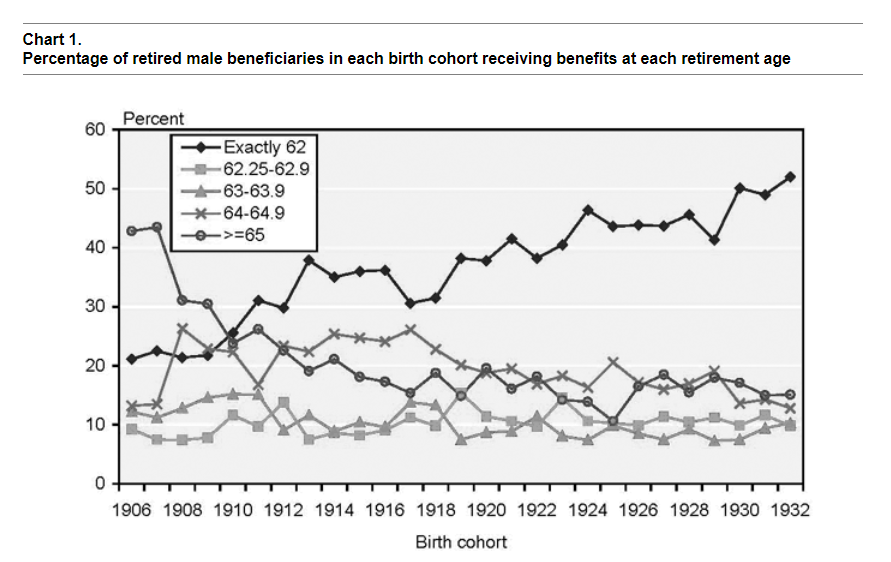

In this paper I use the 1973 cross-sectional Current Population Survey (CPS) matched to longitudinal Social Security administrative data (through 1998) to examine the relationship between retirement age and mortality for men who have lived to at least age 65 by year 1997 or earlier.1 Logistic regression results indicate that controlling for current age, year of birth, education, marital status in 1973, and race, men who retire early die sooner than men who retire at age 65 or older. A positive correlation between age of retirement and life expectancy may suggest that retirement age is correlated with health in the 1973 CPS; however, the 1973 CPS data do not provide the ability to test that hypothesis directly.

Regression results also indicate that the composition of the early retirement variable matters. I represent early retirees by four dummy variables representing age of entitlement to Social Security benefits—exactly age 62 to less than 62 years and 3 months (referred to as exactly age 62 in this paper), age 62 and 3 months to 62 and 11 months, age 63, and age 64. The reference variable is men taking benefits at age 65 or older. I find that men taking benefits at exactly age 62 have higher mortality risk than men taking benefits in any of the other four age groups. I also find that men taking benefits at age 62 and 3 months to 62 and 11 months, age 63, and age 64 have higher mortality risk than men taking benefits at age 65 or older. Estimates of mortality risk for “early” retirees are lowered when higher-risk age 62 retirees are combined with age 63 and age 64 retirees and when age 62 retirees are compared with a reference variable of age 63 and older retirees. Econometric models may benefit by classifying early retirees by single year of retirement age—or at least separating age 62 retirees from age 63 and age 64 retirees and age 63 and age 64 retirees from age 65 and older retirees—if single-year breakdowns are not possible.

The differential mortality literature clearly indicates that mortality risk is higher for low-educated males relative to high-educated males. If low-educated males tend to retire early in relatively greater numbers than high-educated males, higher mortality risk for such individuals due to low educational attainment would be added to the higher mortality risk I find for early retirees relative to that for normal retirees. Descriptive statistics for the 1973 CPS show that a greater proportion of age 65 retirees are college educated than age 62 retirees. In addition, a greater proportion of age 64 retirees are college educated than age 62 retirees, and a lesser proportion of age 64 retirees are college educated than age 65 or older retirees. Age 63 retirees are only slightly more educated than age 62 retirees.

Despite a trend toward early retirement over the birth cohorts in the 1973 CPS, I do not find a change in retirement age differentials over time. However, I do find a change in mortality risk by education over time. Such a change may result from the changing proportion of individuals in each education category over time, a trend toward increasing mortality differentials by socioeconomic status, or a combination of the two.

This paper does not directly explore why a positive correlation between retirement age and survival probability exists. One possibility is that men who retire early are relatively less healthy than men who retire later and that these poorer health characteristics lead to earlier deaths. One can interpret this hypothesis with a “quasidisability” explanation and a benefit optimization explanation. Links between these interpretations and my analysis of the 1973 CPS are fairly speculative because I do not have the appropriate variables needed to test these interpretations.

A quasi-disability explanation, following Kingson (1982), Packard (1985), and Leonesio, Vaughan, and Wixon (2000), could be that a subgroup of workers who choose to take retired-worker benefits at age 62 is significantly less healthy than other workers but unable to qualify for disabled-worker benefits. An econometric model with a mix of both these borderline individuals and healthy individuals retiring at age 62 and with almost no borderline individuals retiring at age 65 could lead to a positive correlation between retirement and mortality, even if a greater percentage of individuals who retire at age 62 are healthy than unhealthy. Evidence for this hypothesis can be inferred from the finding that retiring at exactly age 62 increases the odds of dying in a unit age interval by 12 percent relative to men retiring at 62 and 3 months to 62 and 11 months for men in the 1973 CPS. In addition, retiring exactly at age 62 increases the odds of dying by 23 percent relative to men retiring at age 63 and by 24 percent relative to men retiring at age 64. A group with relatively severe health problems waiting for their 62nd birthday to take benefits could create this result.

An explanation based on benefit optimization follows Hurd and McGarry’s research (1995, 1997) in which they find that individuals’ subjective survival probabilities roughly predict actual survival. If men in the 1973 CPS choose age of benefit receipt based on expectations of their own life expectancy, then perhaps a positive correlation between age of retirement and life expectancy implies that their expectations are correct on average. If actuarial reductions for retirement before the normal retirement age are linked to average life expectancy and an individual’s life expectancy is below average, it may be rational for that individual to retire before the normal retirement age. Evidence for this hypothesis can be inferred from the fact that men retiring at age 62 and 3 months to age 62 and 11 months, age 63, and age 64 all experience greater mortality risk than men retiring at age 65 or older. If only men with severe health problems who are unable to qualify for disability benefits are driving the results, we probably would not expect to see this result. We might expect most of these individuals to retire at the earliest opportunity (exactly age 62).2

Author(s): Hilary Waldron

Publication Date: August 2001

Publication Site: Social Security Office of Policy, ORES Working Paper No 93

Before she exited the Republican primary race, Nikki Haley advocated gradually increasing the retirement age to match the growth in life expectancy. Her political rivals swiftly criticized her proposal, but it enjoys widespread support among those looking to rein in soaring entitlement costs. A new book by economist Teresa Ghilarducci, Work, Retire, Repeat, offers reasons to seek an alternative path to reform.

Pay-as-you-go retirement systems such as Social Security or Medicare use taxes on current workers to pay benefits to retirees. Even if individuals on average fully pay for what they later get, such an arrangement will not be sustainable if declining birth rates and rising life expectancy reduce the ratio of workers to retirees. In 1960, there were five workers for each retiree. By 2000, the ratio had fallen to three-to-one. By 2040, there will be only two workers for each retiree. Raising the retirement age would both reduce the cost of benefits and increase payroll tax revenues to pay for them.

But Ghilarducci’s book argues against pushing back retirement. She suggests that, whereas policymaking elites view retirement as boring, low-paid workers typically can’t wait for relief from “heavy lifting, crushing work schedules, arbitrary changes in work duties, and the fear of being laid off.”

Ghilarducci acknowledges that employment can be a valuable source of meaning, personal identity, achievement, social interaction, and structure in people’s lives. But she disputes the claim that the correlation of retirement with declining mental health proves that it is bad for people.

….

By allowing younger workers to opt for a lower payroll tax rate for the remainder of their careers, in return for a uniform safety-net benefit when they reach retirement, Social Security could be made more effective at preventing poverty while also being less of a burden on the young. Such a benefit structure would likely also motivate higher-earning workers to retire later than the poor—the arrangement for which Ghilarducci provides her strongest arguments.

The MBTA Retirement Fund is going over a cliff, and the reasons why are well known. But neither the T nor its unions are in a hurry to do anything about it.

The new MBTA Retirement Fund Actuarial Valuation Report shows the fund’s balance as of Dec. 31, 2022, was $1.62 billion — about $300 million less than what it was just 12 months earlier. Its liability — the amount it will owe current and future T retirees — is over $3.1 billion, meaning the fund is about 51 percent funded. In 2006, it was 94 percent funded. A “death spiral” generally accelerates when retirement system funding dips below 50 percent.

In April, the Pioneer Public Interest Law Center got the MBTA to hand over an August 2022 arbitration decision regarding a pension dispute between the T and its biggest union. It contained a critical win for the authority: Arbitrator Elizabeth Neumeier decided that most employees would have to work until age 65 to earn a full pension, saving the MBTA at least $12 million annually.

But the Carmen’s Union sued to invalidate that portion of the decision, and the parties returned to the bargaining table. The new pension agreement they hammered out doesn’t include the historic retirement age victory; T management negotiated it away.

….

As of Dec. 31, 2022, 5,555 active employees paid into the fund, but 6,783 retirees collected from it. The biggest reason for the mismatch is the age at which T employees retire. Those hired before December 2012 can retire with a full pension after 23 years of service, regardless of age. Those hired after December 2012 can retire with a full pension at age 55 after 25 years.

The arbitrator finally gave the MBTA the win it so desperately needed, and T management promptly gave it back. Many MBTA managers have long opposed changing the age at which employees can earn a full pension, fearing the reaction of T unions.

….

Hard as it may be to believe, the T retirement fund’s financial outlook is even worse than it appears. Financial projections assume the fund’s assets will earn 7.25 percent annually. Over time, actual returns have been more like 4 percent to 7 percent.

These misleading projections are based on other faulty assumptions. In her 2022 decision, Neumeier refused the MBTA’s request to use newer actuarial tables, ruling that changing would be costly and that there was no compelling reason to update the tables. The ones in place are from 1989 — so old that they assume all T employees are men. Since women tend to live longer, the tables materially understate the retirement fund liability.

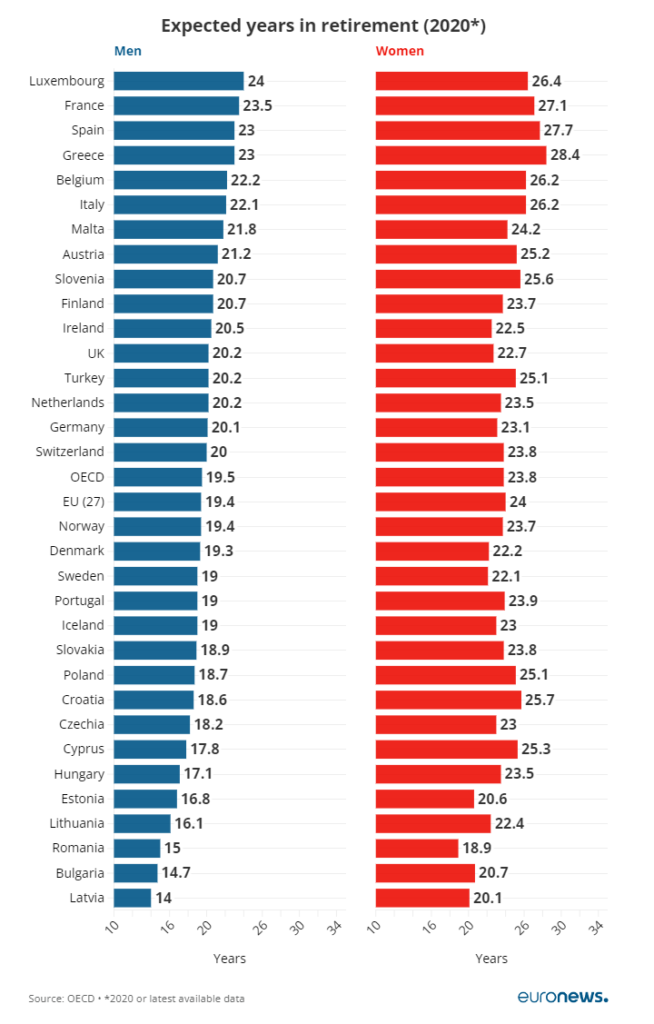

The gap between women and men in expected years of retirement varies from 2.0 years in Ireland to 7.5 years in Cyprus.

By 2020, European women typically can expect to live 4.3 years more than men after they exit the labour market.

While the EU average is 4.6 years, in France, the gender gap stands in favour of women by a total of 3.6 years.

Interestingly, life expectancy in retirement for both highly varies across Europe. For men, it ranges from 14 years in Latvia to 24 years in Luxembourg.

For women, it varies from 18.9 years in Latvia to 28.4 years in Greece. Women are expected to have 26 years or more to spend while retired in Belgium, France, Greece, Italy, Luxembourg and Spain.

China has one of the lowest retirement ages among major economies. Under a policy unchanged since the 1950s, it allows women to retire as early as at age 50 and men at 60. Now, local governments are running out of money just as a wave of retirees hits. That is leaving Beijing with little choice but to ask people to work longer—a move economists say is long overdue but one still likely to meet with resistance.

China’s version of “baby boomers”—those born after China emerged from devastating starvation in the early 1960s—are retiring in droves. Even with government subsidies, by 2035 China’s state-led urban pension fund will run out of money accumulated over the previous two decades, leaving it to rely entirely on new workers’ contributions, according to projections made in 2019 by the Chinese Academy of Social Sciences, a government think tank.

Former central bank Gov. Zhou Xiaochuan warned in a February speech that China must address its pension shortfall and communicate that many Chinese may need to rely on private pension savings

At 6 p.m. yesterday, France’s Constitutional Council ruled that President Emmanuel Macron’s pension cuts are constitutional, removing the last legal obstacle to their adoption as law. The Elysée presidential palace announced 15 minutes later that Macron will promulgate the pension cuts as law within 48 hours.

The Council’s predictable approval of a law opposed by 80 percent of the French people, which Macron rammed through without even a vote in parliament, again tears the “democratic” mask off the capitalist state. It imposes the diktat of the banks, which plan amid the NATO-Russia war in Ukraine to massively divert social spending into strengthening the military-police machine. The struggle against the pension cuts can only be waged as a political struggle directed against the entire capitalist state machine.

The Council’s decision also exposes the forces in the union bureaucracy and the pseudo-left parties who, warning of “violence” by protesters, told workers to place their hopes in trade union “mediation” with Macron. Everyone involved, including masses of workers and youth, knew very well that Macron would ignore the “mediation.” On the other hand, two-thirds of the French people supported a general strike to block the economy and bring down Macron.

In 2021, government spending accounted for 59 percent of GDP in France, compared with 45 percent in the United States. Spending on public pensions accounts for much of that gap: it’s 15 percent of GDP in France, but only 7 percent in the U.S. This greatly inflates associated payroll taxes, which alone took 28 percent of workers’ incomes in France, compared with just 11 percent in the U.S.

President Macron argues that the cost of financing pensions is dragging down the whole economy, and that reform is necessary to make France an attractive venue for investment and employment. Whereas workers’ incomes in 1975 were 46 percent higher than those of retirees, by 2016 they were 2 percent lower. Many economists see it as senseless to redistribute so much from the young to the elderly, who seldom have childrearing expenses and whose mortgages are often paid off.

Pension reform is seen as necessary by 61 percent of French voters, but only 32 percent support raising the retirement age. Macron argues that the only alternatives to his reforms would involve cutting benefit levels, hiking taxes, or cutting public spending on other items such as education, health care, or defense. France already has close to the highest taxes in the developed world.

Median incomes for French residents aged 65 and over ($20,116) are little different than those for Americans ($19,704). The main effects of France’s extra pension spending are to crowd out private savings for retirement (which amount to 12 percent of GDP versus 170 percent in the U.S), and to cause French citizens to retire much earlier (at an average age of 60.4, vs 64.9 in the states).

Protests and strikes against unpopular pension reforms gripped France again Tuesday, with many thousands marching and the Eiffel Tower closed and police ramping up security amid government warnings that radical demonstrators intended “to destroy, to injure and to kill.”

Concerns that violence could mar the demonstrations prompted what Interior Minister Gérald Darmanin described as an unprecedented deployment of 13,000 officers, nearly half of them concentrated in the French capital.

After months of upheaval, an exit from the firestorm of protest triggered by President Emmanuel Macron ‘s changes to France’s retirement system looked as far away as ever. Despite fresh union pleas hat the government pause its hotly contested push to raise France’s legal retirement age from 62 to 64, Macron seemingly remained wedded to it.

According to police figures, Tuesday’s nationwide protests marked the largest single-day union-backed demonstration in France in thirty years. Some 1.272 million turned out to the streets. That’s more than the already-impressive January 19 turnout, it’s more than any of the single-day peaks of the 2010 and 2003 movements over retirement reforms — it even topped the height of the legendary 1995 protests.

And there’s more to come. The united union coalition has called for two further days of strikes and protest: Tuesday, February 7, and Saturday, February 11. “Until then,” the coalition has also called on the public to “multiply actions, initiatives, meetings, and general assemblies across the country, in workplaces [and] at places of study, including through strikes.”

After two successful national mobilizations, the movement seems to be entering a new phase. Public opinion is clearly on its side — and yet, the government isn’t budging on the proposed hike in the retirement eligibility age from sixty-two to sixty-four. Clearly, it’s going to take more for organized labor to win this battle.

….

Clearly, the strike calls over pension reform have resonated beyond organized labor’s traditional bastions of support in the public sector: namely, schools, health services, and transit networks (the national SNCF rail company and the Paris metro network). Workers in all these sectors have walked off the jobs, but so have others in the private sector. The General Confederation of Labour (CGT) has shared a list of strikes on January 31 that illustrates this point: five thousand strikers at Airbus; a walkout from 90 percent of the staff at a FNAC department store outside of Toulouse; a strike from 80 percent of the workers at a LU Mondelēz factory in Normandy, etc.