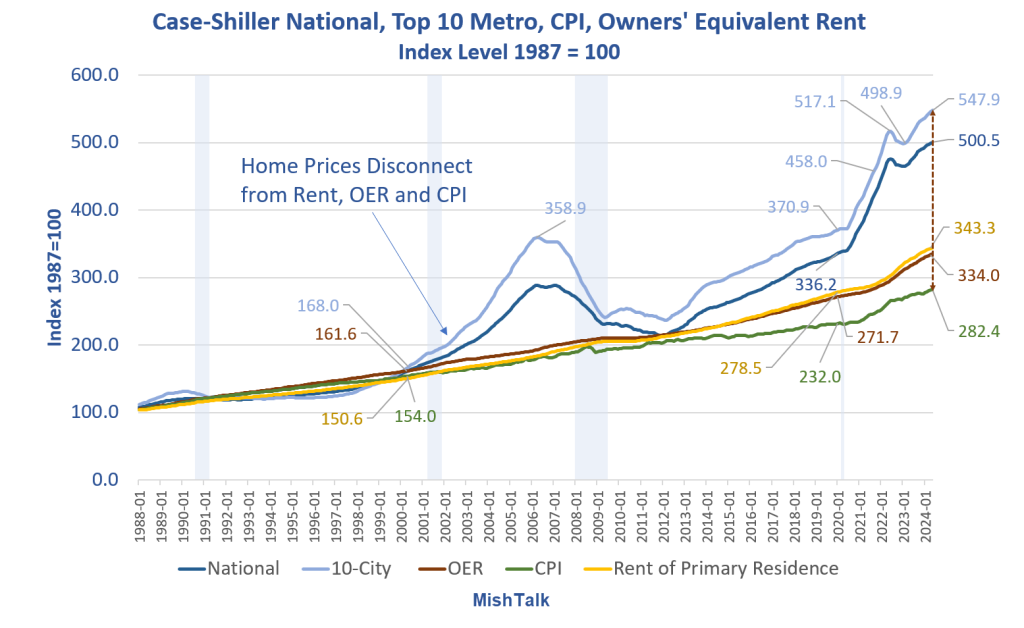

Housing affordability continues to soar out of reach of most buyers. Not only are prices at a new record level, mortgage rates remain close to 7.0 percent.

Chart Notes

Case-Shiller measures repeat sales of the same price over time. It is the best measure of price, but it lags. Current data is as of May which reflects sales 1-3 months prior.

The CPI, OER, and Rent of Primary Residence are all from the BLS.

OER stands for Owners’ Equivalent Rent. It is the rent one would pay if someone was renting instead of paying a mortgage.

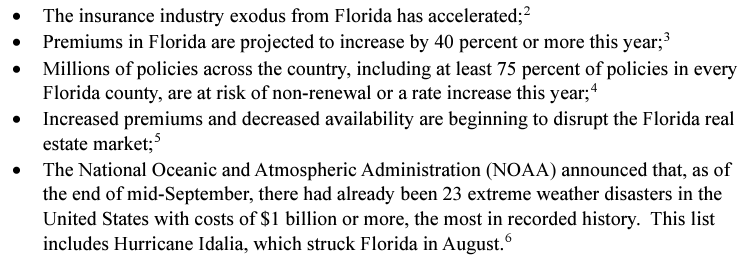

The federal government has launched an investigation into Florida’s largest home insurance company.

Citizens Insurance, the governor, and other state leaders received a letter informing them that a Senate budget committee is looking into the state-run company.

Citizens insure $586 billion worth of property, and they have just over $15 billion in their reserves to pay out on claims. If a major hurricane hit the state, they could be short over $571 billion, leaving everyone in the state on the hook to pay the shortfall.

The letter from the Senate committee investigating the state backed company expresses concern it may be unable to cover its losses. A claim the governor confirmed while visiting Fort Myers last year.

….

Mark Friedlander with the Insurance Information Institute said a private insurer would not be allowed to operate in the State of Florida with those financial dynamics.

Seven private companies went insolvent in the last year and a half in Florida.

“Citizens, unlike a private insurer, could never go insolvent,” Friedlander noted.

That’s because the state could initiate a hurricane tax to cover its costs which would require everyone who owns property or a car to pay a hurricane tax.

As of 2022, Citizens’ market share for homeowners multi-peril policies was approaching 20 percent, having more than doubled since 2020. As private insurers in Florida continue to go insolvent or exit the state, Citizens’ market share will likely continue to grow. At 20 percent market share, Citizens’ losses could be as high as $36 billion in the scenario studied by Swiss Re or $162 billion in the scenario studied by Cambridge and Munich Re (assuming that 60 percent of total losses are insured). If Citizens had to raise $162 billion to cover losses, that would result in an approximately $20,000 assessment for every homeowners insurance policyholder in Florida.

….

To that end, please respond to the following requests for information and documents by December 21, 2023:

1. What modeling or other analysis has Citizens done to estimate its total potential exposure to various worst case hurricane scenarios? What is the upper range of Citizens’ potential losses? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ potential losses.

2. What modeling or other analysis has Citizens done to estimate its market share over the next decade? What does Citizens project its market share to be in each of the next 10 years? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ future market share.

3. What modeling or other analysis has Citizens done to determine its ability to fully pay out claims resulting from various loss scenarios? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ financial position and (in)solvency under such scenarios.

4. What are Citizens’ current assets? What is Citizens’ total reinsurance coverage? What are the maximum total claims Citizens would be able to pay out without having to levy an assessment on Florida policyholders? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ current assets, reinsurance, and ability to pay claims.

5. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Michael Yaworsky, their staffs, or any other state officials regarding Citizens’ current or future solvency? Please provide copies of these communications.

6. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials regarding what Citizens and/or the State would do if Citizens were unable to cover its losses? Please provide copies of these communications.

7. Has Citizens contemplated asking for a federal bailout if it were unable to cover its losses? Has Citizens discussed the possibility of a federal bailout with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials? Please provide copies of these communications.

I spoke to Rex Frazier, president of the Personal Insurance Federation of California, who cited several policies that no doubt contributed to State Farm’s decision to stop issuing policies, including various price controls that prevent insurers from raising prices to meet surging costs without the written approval of the California Department of Insurance.

“California is the only state in the country that doesn’t allow insurers’ rates to be based upon actual reinsurance costs,” Frazier said. “California’s regulations employ a legal fiction that each insurer uses its own capital to serve customers. As reinsurance costs go up, insurers cannot have their rates reflect those higher costs.”

State Farm General Insurance Co. last week became the latest insurer to retreat from California’s homeowners market. The culprit isn’t climate change, as the media claims in parroting Sacramento talking points. The cause is the Golden State’s hostile insurance environment.

The nation’s top property and casualty insurer on Friday said it won’t accept new applications for homeowners insurance, citing “historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market.”

In other words, State Farm can’t accurately price risk and increase its rates to cover ballooning liabilities. Other property and casualty insurers, including AIG and Chubb, have also been shrinking their California footprint after years of catastrophic wildfires, which are becoming more common owing to drought and decades of poor forest management.

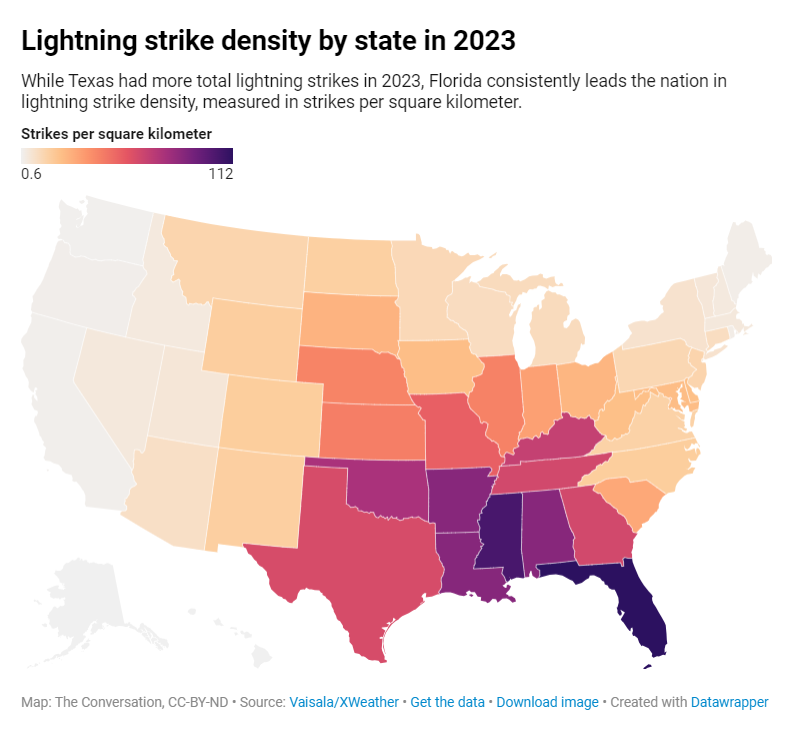

In a typical year, about 100 storms and tropical disturbances develop in the Atlantic Ocean, Caribbean Sea and Gulf of Mexico. Some of these turn into tropical storms, and on average, two each year become hurricanes that make landfall in the U.S.40 Between 1851 and 2016, 289 hurricanes affected the continental U.S. Of these, 63 made landfall in Texas.41

….

Of course, hurricanes and other major storms affect the entire country, not just the Gulf Coast. Exhibit 6 lists the most destructive storms affecting the U.S. in the last half-century.

Hurricane Katrina, which caused $161.3 billion in damages, still ranks as the costliest storm in American history; Hurricane Harvey is expected to rank second, with total estimated damages of about $125 billion.45

Publication Date: February 2018, accessed April 2023

Publication Site: Fiscal Notes, Comptroller of Texas

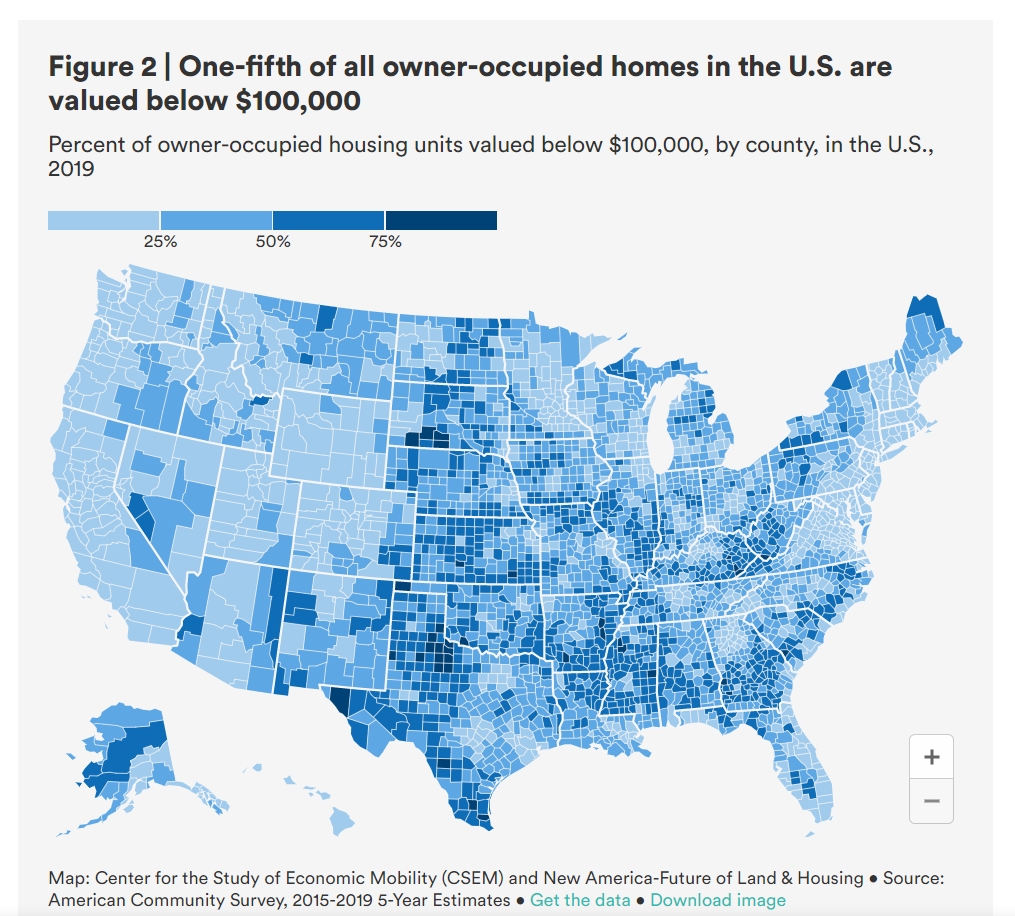

While conventional wisdom maintains that high home prices are to blame for declining homeownership rates, there is another elusive barrier stopping millions of would-be homeowners: banks are increasingly unwilling to write small dollar mortgages. One fifth of owner-occupied homes in the United States cost less than $100,000, but due to unintended consequences of the Dodd-Frank Act, among other factors, banks are opting out of writing small dollar loans. Instead, more than three quarters of small dollar homes are purchased in cash, often by investors or well-off individuals. This lending gap locks millions of low-and-moderate income families out of homeownership, and exacerbates the racial homeownership gap as these small dollar homes are a critical source of homeownership for many first-time buyers in Black and Hispanic communities.

In this report, the Future of Land and Housing program at New America and the Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University (WSSU) focus on three dimensions of this problem: 1) the unavailability of financing for small dollar loans; 2) the catch-22 of “mortgage standards”; and 3) competition with all-cash buyers at a national level and through a local case study of Winston-Salem and Forsyth County, North Carolina.

Author(s): Sabiha Zainulbhai, Zachary D. Blizard, Craig J. Richardson, Yuliya Panfil

This Axios report on a JPMorgan Chase program giving black and Latino borrowers $5,000 toward down payments or home loan closing costs reminded me of a column I wrote in November [2021]. It’s about one of the most infuriating public policy fiascos I’ve run into in a very long time. Hardly anyone knows about this regulatory devastation of household wealth amog people whose inexpensive homes represented years of thrift and hard work. (The only reason I learned of it is that I happened to meet Craig Richardson at an unrelated conference.) It is absolutely heartbreaking. It reminds me of the famous quote from The Great Gatsby: “They were careless people, Tom and Daisy—they smashed up things and creatures and then retreated back into their money or their vast carelessness or whatever it was that kept them together, and let other people clean up the mess they had made.”

….

About one in five U.S. homes are valued at $100,000 or less. And despite their low prices, they’ve gotten extremely hard to sell. When they move at all, these small-dollar properties tend to go for cash. Lenders increasingly won’t write mortgages for them.

The culprits behind the disappearance of small-dollar mortgages are lending restrictions enacted with good intentions and warped by economic blind spots. Designed to protect borrowers and the financial system, the Dodd-Frank Act regulations passed in the wake of the 2008 financial crisis “increased the fixed costs and the per-loan costs of extending a mortgage,” says the study. The regulation-imposed costs made small-dollar mortgages a lousy proposition for lenders.

Compounding the problem, the Consumer Financial Protection Bureau then limited the fees that lenders could charge as closing costs. For profit-oriented lenders, small-dollar mortgages are no longer worth the trouble. At best, they squeeze out the tiniest of margins. At worst, they don’t even cover the fixed cost of processing the loan.

Author(s): Virginia Postrel

Publication Date: 25 June 2022

Publication Site: Virginia’s Newsletter at substack