Graphic:

Publication Date: 27 Apr 2026

Publication Site: Treasury Dept

All about risk

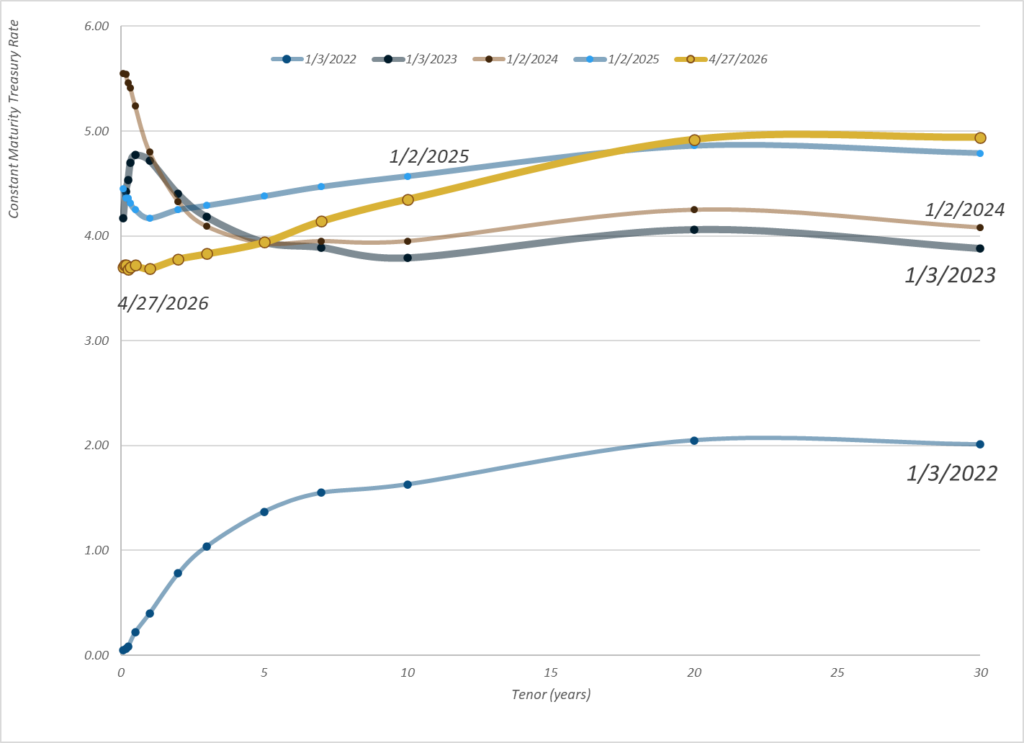

Graphic:

Publication Date: 27 Apr 2026

Publication Site: Treasury Dept

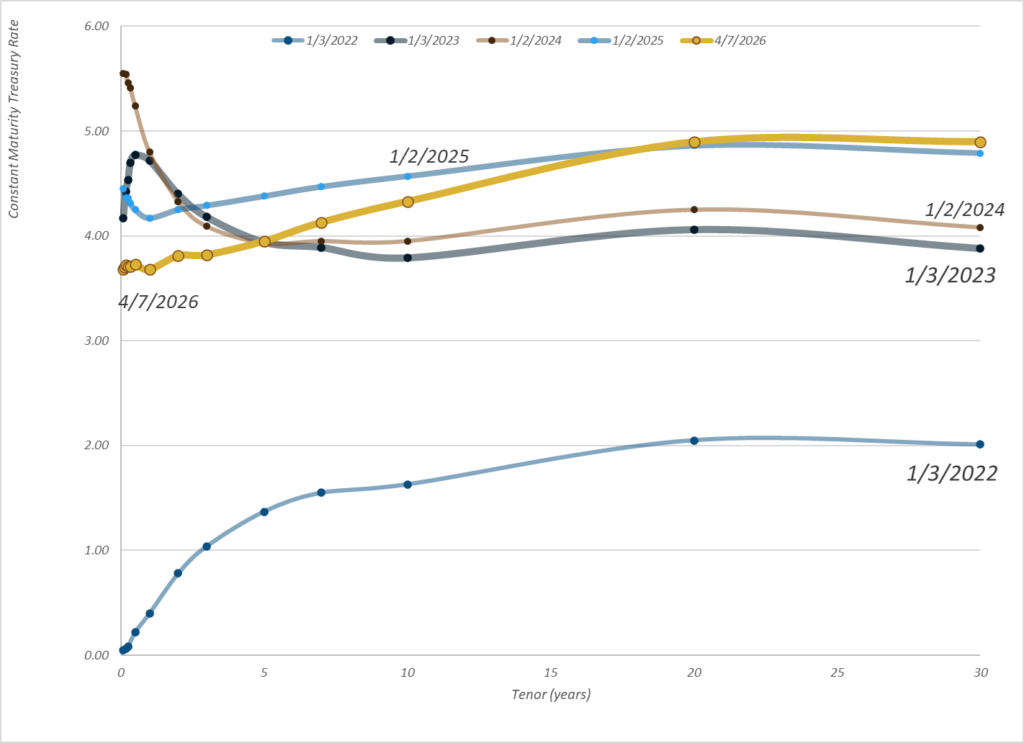

Graphic:

Publication Date: 7 Apr 2026

Publication Site: Treasury Dept

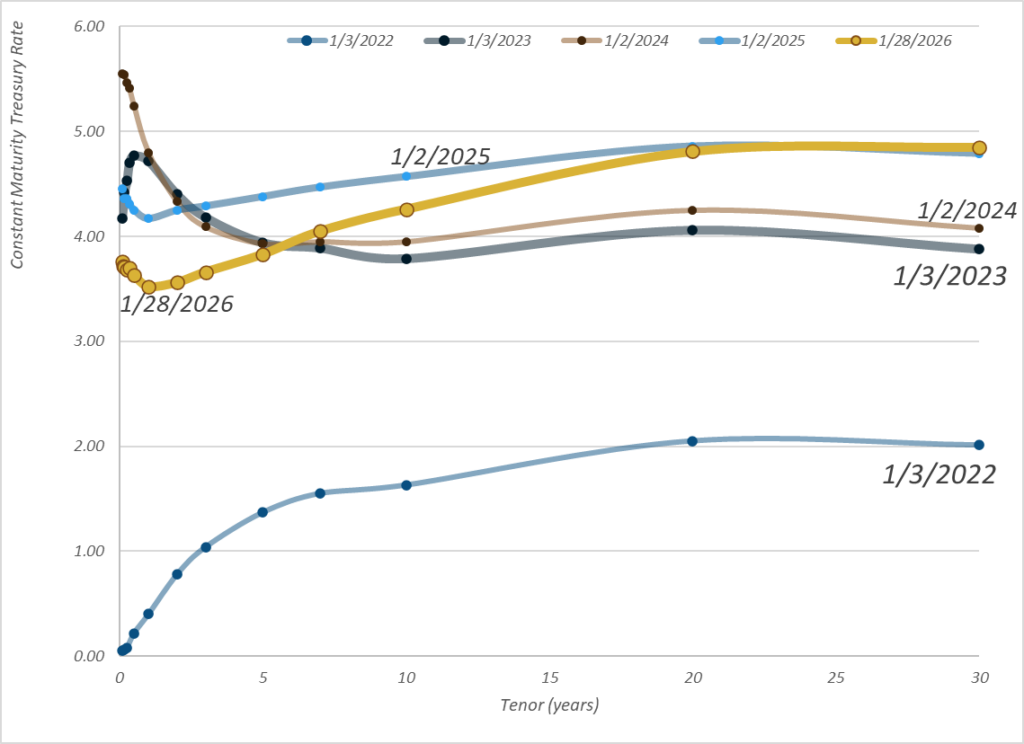

Graphic:

Publication Date: 28 Jan 2026

Publication Site: Treasury Dept

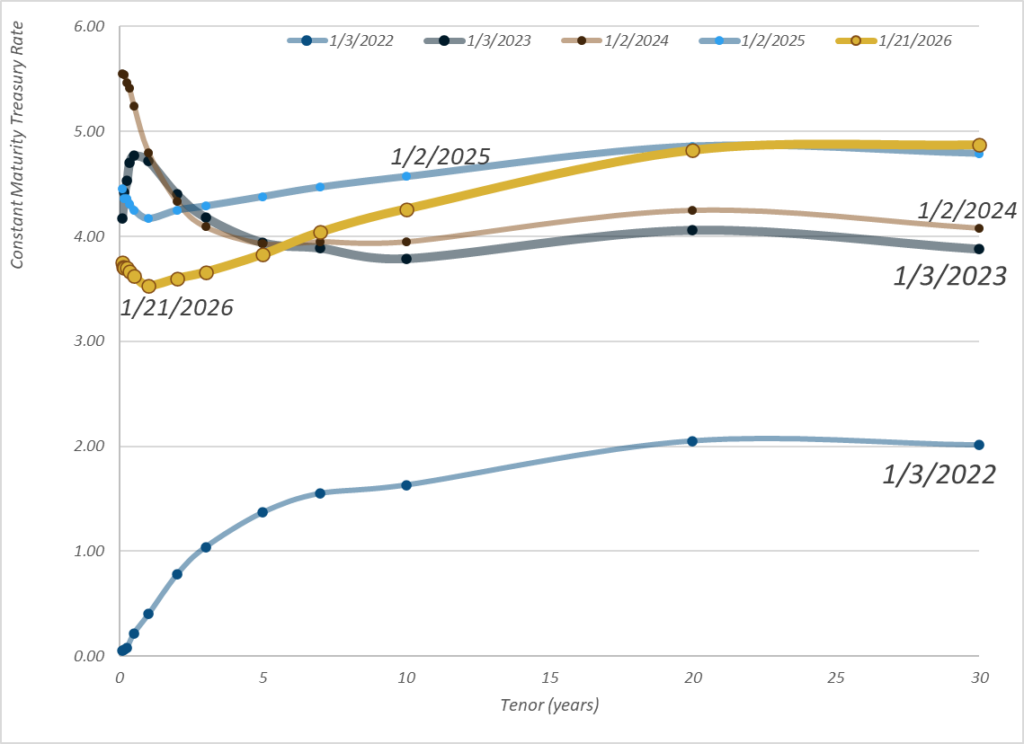

Graphic:

Publication Date: 21 Jan 2026

Publication Site: Treasury Department

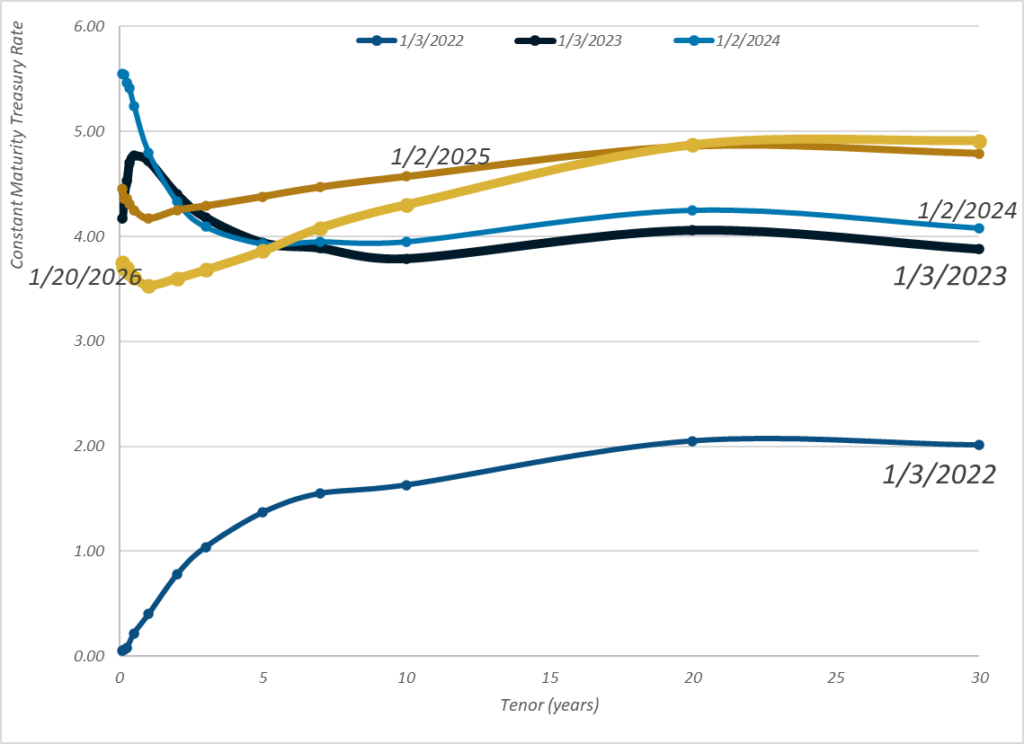

Graphic:

Publication Date: 20 Jan 2026

Publication Site: Treasury Dept

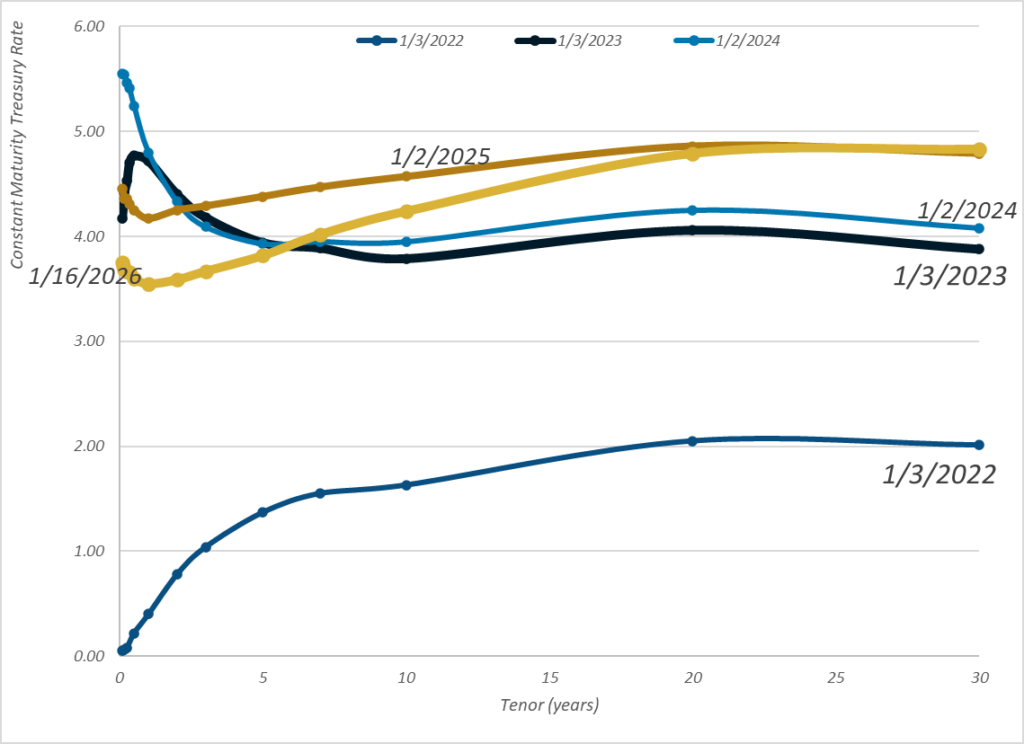

Graphic:

Publication Date: 16 Jan 2026

Publication Site: Treasury Department

Graphic:

Publication Date: 5 Jan 2026

Publication Site: Treasury Dept

Graphic:

Publication Date: 18 Dec 2025

Publication Site: Treasury Dept

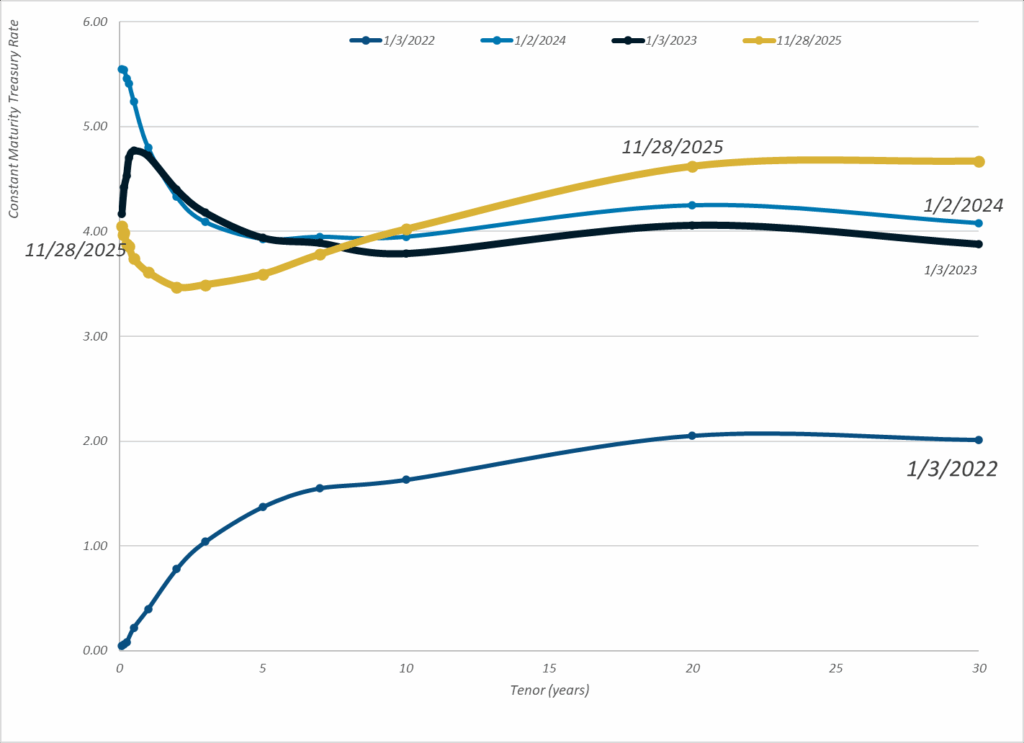

Graphic:

Publication Date: 28 Nov 2025

Publication Site: Treasury Dept

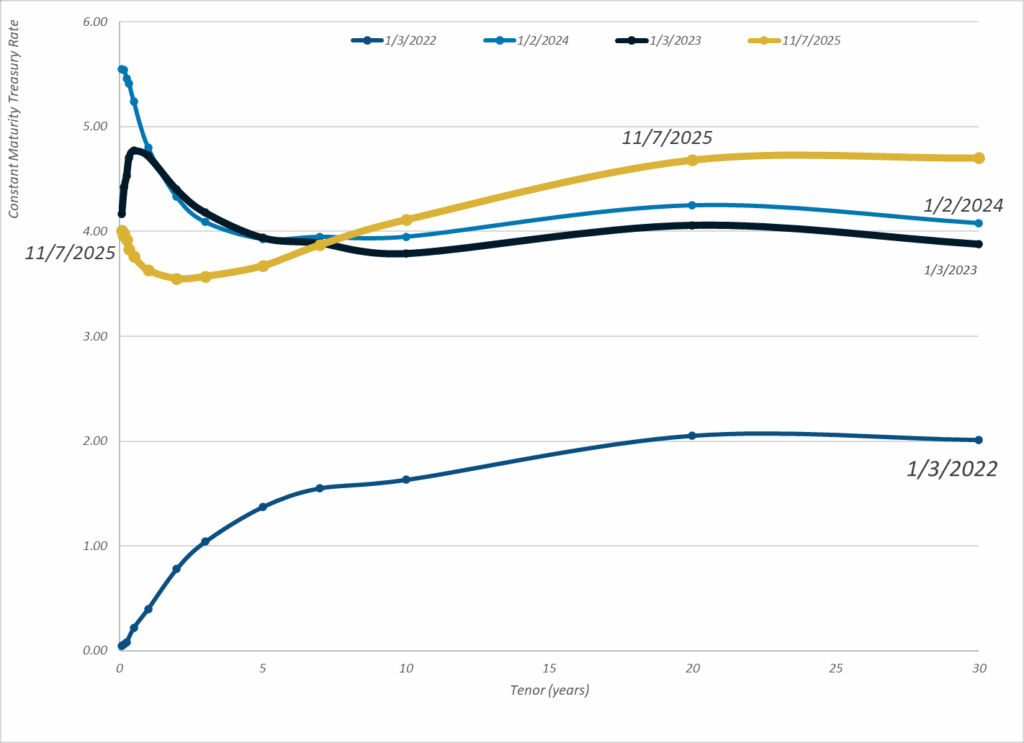

Graphic:

Publication Date: 7 Nov 2025

Publication Site: Treasury Dept

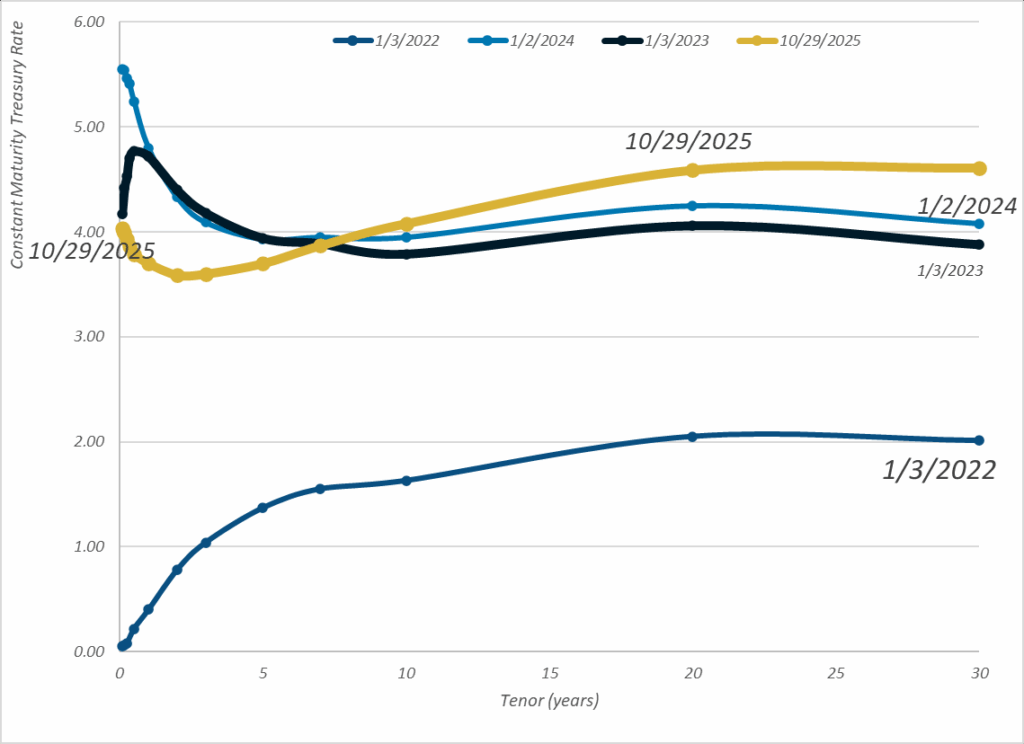

Graphic:

Publication Date: 29 Oct 2025

Publication Site: Treasury Dept

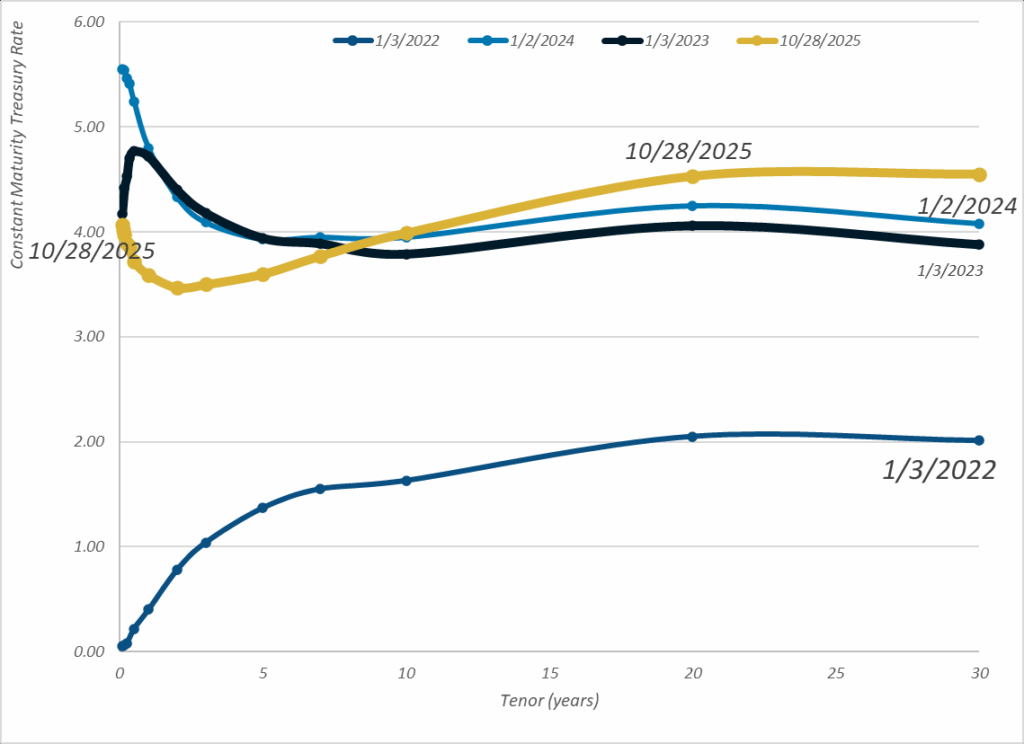

Graphic:

Publication Date: 28 Oct 2025

Publication Site: Treasury Dept