School districts and state agencies face another major hike in their payments to the Oregon Public Employees Retirement System during the two-year budget cycle starting July 1, 2027, according to new projections released last week.

The tab for individual public employers won’t be clear until December, when system actuary Milliman Inc. releases projected pension contribution rates for each of the system’s 900 participating employers for the next biennium. And those rates won’t be set in stone until next year, when the actuary knows how much the system’s investments earned in 2025.

Service Union Employees International Union 503 boss Melissa Unger speaks at the Oregon Capitol in support of a $4.3 billion tax increase passed by the legislature last month.

Excerpt:

The timing of the latest financial projections from the Oregon Public Employees Retirement System, as reported by The Oregonian’s Ted Sickinger, could not have been more appropriate.

As the Oregon Legislature was inching toward the conclusion of a special session it claimed was necessary to ensure continuance of basic road maintenance, the actuary for the PERS system issued preliminary estimates of investment earnings and required contributions by public employers indicating that the state is going to need a lot more money unless it finds a way to reduce pension obligations or operate more efficiently.

Whether your political preferences lean left or right or reside in the middle, the report should scare you. Unless the Legislature is able to accomplish one of three difficult things, the state’s descent toward the bottom of national rankings is likely to pick up speed. Here’s a look at each one, all fraught with risk.

Raise taxes more, probably a lot more.

….

Enact further PERS reforms

….

Downsize state and local government

….

This is a problem that has been building for a more than a half century. Aside from occasional efforts to make minor fixes that at best slowed the bleeding, the Legislature has chosen to ignore the problem and hope for a miracle cure in the form of outsized investment gains. But despite record stock-market gains over most of that period, the day of reckoning finally appears upon us. And, as usually happens when one delays necessary treatment, the patient already is in critical condition.

I note with great emphasis: “We do not possess thorough look through ability.”

That’s the first time I’ve ever heard those confusing words. Here’s a translation:

State pension fiduciaries have failed to demand that external investment managers disclose to the pension on a timely basis all investments, including but not limited to crypto, in their funds’ portfolios.

State pension fiduciaries have failed to disclose to Oregonians information they don’t possess regarding the pension’s riskiest investments.

State pension fiduciaries cannot be monitoring the risks related to crypto investments they do not know they own.

Bad enough that the Oregon State Treasury is gambling $60 billion in high-cost, high-risk alternative funds. State officials don’t know—and apparently don’t even care—what’s in those funds.

BlackRock, the world’s largest asset manager, said letters sent to the firm by 26 Republican state finance officials in July and 17 Democrat state finance officials in August “continue a concerning trend by both parties of politicizing the management of public pension funds.”

“Many of our clients value having BlackRock act as an engaged shareholder on their behalf,” S. Jane Moffat, BlackRock’s managing director of U.S. government affairs and public policy, told the finance officials in an Aug. 27 response letter. “At the same time, BlackRock is not an activist investor.”

BlackRock’s response comes after the state officials painted drastically different views of what they viewed as “fiduciary duty” in their letters. The coalition of Republican state officials urged the asset manager and other financial institutions to stop framing climate change as a long-term risk, while the coalition of Democrat officials looked to push BlackRock and others to reaffirm their commitment to managing climate change and other similar long-term risks.

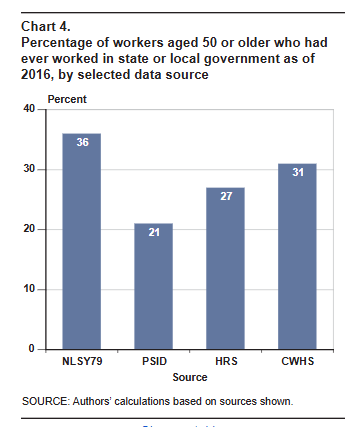

Analysis based on a synthetic population of noncovered state and local government workers confirms earlier results based on a sample of retirement plan benefit formulas: Workers with medium-length government tenures are at risk of receiving lifetime retirement income that falls short of Social Security equivalence. Given the distributions of the synthetic population of noncovered workers by occupation, retirement-plan benefit formula, and tenure in government employment, this translates to about 16 percent of all noncovered workers at risk of receiving less retirement income than they would have received from Social Security alone had they spent their whole careers in covered employment.

Although the share of workers with projected retirement benefits that fall short of Social Security equivalence is not large, the problem is serious. Social Security is intended to provide a minimum level of retirement income for all Americans. Covered public-sector workers and many private-sector workers augment their Social Security benefits with employer-sponsored retirement plans. The concern is that pension benefits ultimately will not meet that minimum level for 750,000 to 1 million noncovered workers annually who cannot augment those benefits with Social Security income.

Author(s): Jean-Pierre Aubry, Siyan Liu, Alicia H. Munnell, Laura D. Quinby, and Glenn R. Springstead

Social Security Bulletin, Vol. 82 No. 3, 2022 (released August 2022)

The Ohio State Teachers’ Retirement System cannot invest its way to a permanent COLA, Brian Grinnell, former chief actuary of the $97.3 billion pension fund, told Pensions & Investments.

Grinnell left the pension fund in May after more than 10 years as its chief actuary. In a Sept. 27 interview, he said his responsibilities were primarily to help STRS staff and the board understand the risks the pension fund has faced and help develop a forward-looking plan to make decisions with long-term outcomes in mind.

In his interview, he said, “I was not comfortable with the direction the plan was headed, and I didn’t feel like my continued participation would be positive.”

….

The pension reform law, SB342, was one of five laws that addressed funding issues at all five of Ohio’s state retirement systems and was drafted as a result of severe stock market declines that came from the Great Recession in 2008 and 2009. Among all the state systems, STRS was the worst off in 2012 with a funding ratio of 57.6% as of June 30 of that year. Additionally, the amortization period for the retirement system’s unfunded pension liabilities under the STRS defined benefit plan had become infinite — meaning that it would never become fully funded.

Grinnell said STRS has had to contend with the challenge of being an extremely mature pension fund: Essentially, there is more money being sent out to retirees receiving benefits now relative to the future contributions the pension fund can expect from current and future teachers.

“Here’s where STRS is a little bit of an unusual situation because it is a fixed-rate plan,” Grinnell said, “so both the benefits and the contributions are essentially fixed by statute. So most plans, if they have a bad year in terms of investment performance, the contribution rate goes up the following year to fill that hole. That doesn’t happen at STRS.”

Grinnell said when a pension fund is both a mature plan and has that fixed-rate contribution and fixed benefits, it’s very difficult to recover from any kinds of market downturns. He noted that all five of Ohio’s state retirement systems have that fixed-rate structure.

“Most other public pensions do not have that kind of structure,” he said, “and I think that tends to work all right for an immature plan, a plan that’s growing and not paying out a lot of benefits relative to the contributions.”

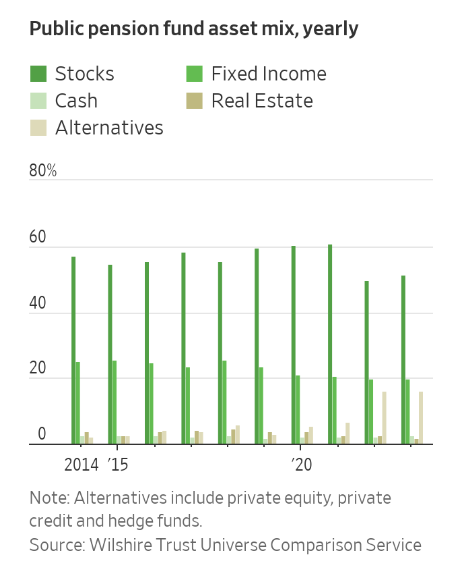

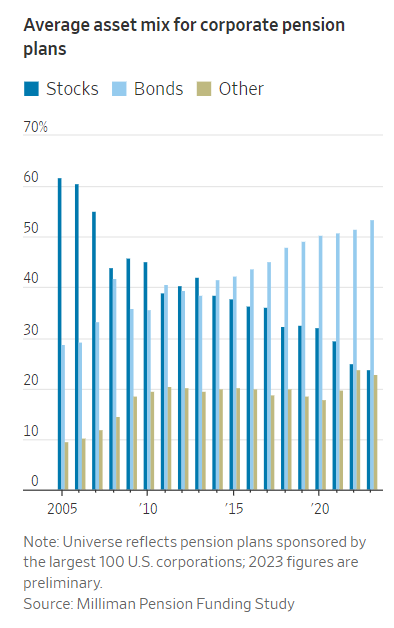

Stock portfolios at large pension funds had a blockbuster run. Now, managers are cashing out.

Corporate pension funds are shifting money into bonds. State and local government funds are swapping stocks for alternative investments. The nation’s largest public pension, the California Public Employees’ Retirement System, is planning to move close to $25 billion out of equities and into private equity and private debt.

Like investors of all kinds, the funds are slowly adapting to a world of yield, where they can get sizable returns on risk-free assets. That is rippling throughout markets, as investors assess how much risk they want to take on. Moving out of stocks could mean surrendering some potential gains. Hold too much, for too long, and prices might fall.

The Dallas Police and Fire Pension System — which as been severely underfunded for years — still has about 25% of its assets tied up in private investments.

That’s according to pension system official’s briefing during Thursday’s Ad Hoc Committee on Pensions meeting.

Those include investments in an energy fund, natural resources — and assets in real estate. The private investments were deemed “legacy” assets that the pension system still maintains.

It was risky private investments that landed the system in the situation it’s in now — with over a billion dollars in unfunded liabilities.

“Currently we’ve gotten that down to 26%,” Dallas Police and Fire Pension System Chief Investment Officer Ryan Wagner said during the meeting.

Connecticut taxpayers, saddled with a pension system for state workers and teachers marked by decades of underfunding, glimpsed a ray of hope in 2017 when legislators embarked on a path toward accountability and fiscal discipline by enacting “fiscal guardrails.”

Now, state unions under the umbrella of the State Employees Bargaining Agent Coalition are clamoring for the removal of the fiscal guardrails that were constructed to prevent the same unions from driving taxpayers over the cliff. The staggering state debt of more than $80 billion, including unfunded pension debt from the state workers’ and teachers’ pension funds, bonded debt, and health-care liabilities, was the result of years of irresponsibility and political horse-trading with state unions that were all too eager to negotiate benefits without a sustainable funding plan.

…..

Connecticut has long been a high-income per capita state and also imposes one of the country’s most burdensome tax systems. Yet it still managed to accumulate the highest state debt per resident. The 2017 bipartisan fiscal guardrails constituted a recognition that the previous decade’s cycle of budget shortfalls, followed by significant tax increases, was simply unsustainable.

The guardrails were codified in 2023, and the general assembly unanimously voted to extend them for another five years. Their very effectiveness in slowing spending growth has made them susceptible to attack from state unions.

The Financial Times made its interview with departing CalSTRS’ Chief Investment Officer Chris Ailman its lead story yesterday: Private equity should share more wealth with workers, says US pension giant. The Financial Times was too polite to say so, but Ailman could lay claim to being the best large public pension fund chief investment officer. CalSTRS, which manages the pensions of California teachers, is in the same general size league as its Sacramento sister CalPERS, and regularly outperforms CalPERS by a meaningful margin.

….

It’s hard to know where to begin with this. Limited partners like CalSTRS, who are, in Wall Street parlance, the money, have not even been able to get basic disclosures from the general partners like how much in total the private equity firms hoover out in fees and expenses, despite many years of pleading. Mind you, it’s a requirement for a fiduciary to evaluate the costs and risks of any investment, yet these investors have accepted this abuse.

Limited partners don’t get P&Ls of portfolio companies. They don’t get independent valuations even though that is considered to be essential for every other type of investment. So it’s ludicrous to think that general partners will share money with one of the very weakest parties in the picture, mere workers, when they won’t give information to the limited partners.

Someone new to this topic might wonder why limited partners don’t say “no”. The reason is they perceive private equity to be necessary for them to earn enough to reduce their level of underfunding, which in the public pension fund world is typically pretty bad. To make up for the shortfalls, pension funds like CalPERS and CalSTRS have also been increasing the amount they charge to cities, counties, and other local government entities. These pension costs are taking up larger and larger proportions of these budgets, creating concern and anger.

The New York State Common Retirement Fund (Fund) will restrict its investments in eight integrated oil and gas companies, including Exxon Mobil Corp., after a review of the companies’ readiness to transition to a low-carbon economy, State Comptroller Thomas P. DiNapoli, trustee of the Fund, announced today.

The evaluation of the Fund’s integrated oil and gas holdings is part of DiNapoli’s broader review of the transition readiness of energy sector investments that face significant climate risk. With today’s announcement, the Fund will be divesting its corporate bonds and actively managed public equity holdings in eight integrated oil and gas companies that it has determined are not transition-ready. In addition to Exxon, the companies to be divested and restricted in the coming months are Guanghui Energy Company Ltd., Echo Energy PLC, IOG PLC, Oil and Natural Gas Corporation Ltd, Delek Group Ltd., Dana Gas Co and Unit Corp. The value of these holdings is approximately $26.8 million as of Dec. 31, 2023.

DiNapoli also announced the Fund has met its initial goal of committing $20 billion to the Sustainable Investments and Climate Solutions program, and has set a new goal of investing $40 billion in that program by 2035. With the program, the Fund invests in sustainable investments including clean energy generation, energy storage, resource efficiency, and green infrastructure across all asset classes. As part of the expansion of this program, DiNapoli also announced the Fund would increase its climate index investments by 50% to over $10 billion over the next two years, with the longer-term goal of doubling it by 2035.

Publication Date: 15 Feb 2024

Publication Site: Office of the Comptroller of NY State

Activists credit the support of Beck, Maine Rep. Maggie O’Neil and state Sen. Chloe Maxmin for making Maine the first state to require fossil fuel divestment by law.

Passed and signed by Maine’s governor in 2021, LD99 calls for the state’s permanent funds and its pension system, MainePERS, to divest from fossil fuel investments by 2026 and not reinvest going forward.

It prohibits both specific lists of publicly traded companies as well as any whose “core business” is in fossil fuel exploration, extraction, refining, processing or infrastructure. (A separate 2021 law also requires Maine to divest from private prisons.)

Other pension systems, including New York state’s, have made promises to divest from companies whose primary business drives planet-warming emissions, but are not required to by legislation. In 2015, California passed a law to remove public investments in thermal coal, but a move to extend that to all fossil fuel companies died in the Legislature this session.

MainePERS’ assets — about $18 billion at the end of the last fiscal year — are small in comparison to New York and California, but how they manage their legislative mandate will be closely watched as other states face calls for fossil fuel divestment and wider questions of dealing with climate risk in investing.

Leaders at the pension system stressed a key phrase in the legislation, that any MainePERS divestment decision will be made “in accordance with sound investment criteria and consistent with fiduciary obligations” — crucial to a state constitutional requirement to its pension members.

….

MainePERS Chief Investment Officer James Bennett estimates about $1.2 billion of the system’s total holdings are in fossil fuel investments, split evenly between publicly traded companies and private investments.

Liquidating private investments will be more complicated, he says. Many of the limited partnerships MainePERS is invested in include fossil fuel assets alongside other infrastructure investments and cannot be separated. They’d need to sell the whole thing, if it indeed is within the financial interest of members to do so.