The first thing to understand about bird-on-plane collisions? They’re not the animals’ fault. Swaths of open green space and very few people around make airstrips and their surroundings ideal places for the feathered to, well, flock. As a result, most bird strikes occur during takeoffs and landings. Even off-airport strikes—such as the one involving Sully’s plane—usually happen within five miles of an airport, and at an altitude of 3,000 feet or less.

With 45,000 flights crisscrossing the US every day, odds are good that a handful of airplanes will run into birds. In 1905, Wilbur Wright recorded the first-ever bird strike, over an Ohio cornfield. In 2023, planes hit more than 18,000 birds. The strikes cost the commercial aviation industry roughly $600 million annually in repairs—and if you add in military flights, the total is closer to $650 million.

….

That’s where airports come in. Over the last three decades, the Federal Aviation Administration has recorded every reported midair encounter between bird and plane— roughly 285,000—in the National Wildlife Strike Database. Somewhat amazingly, just 651 bird species have ever been involved. Knowing the specific types of birds that are in their skies helps airports keep them from the flight paths of jumbo jets.

A casualty actuary might be forgiven for thinking that illness and disease are what those “other” actuaries worry about.

Though risk of illness is usually considered the province of the life-health actuary, a session at the 2017 CAS Annual Meeting in Anaheim, California, showed how epidemics can affect property-casualty risks. The session also described how to approach modeling those exposures.

….

Milliman actuary Cody Webb, FCAS, began by demonstrating how big the insurance gap is, particularly in developing nations. He explained that the spectrum of losses ranges from minuscule (loss of a single strand of hair) to catastrophic (sudden, instant death) and can affect a single person or every entity in the universe across eons. But the insurable losses share some traits, Webb said, including:

a large number of similar exposures.

a definite loss, driven by some sort of accident.

the ability to create an affordable premium to reimburse after such a loss.

the ability to accurately quantify the amount of loss sustained. This is the most important shared trait.

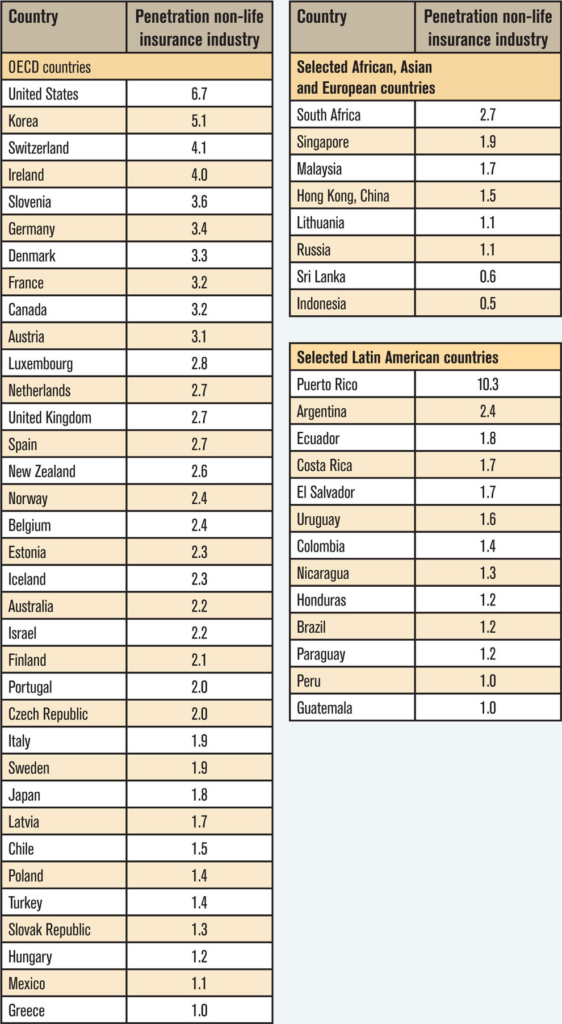

In showing a chart of property-casualty insurance as a percentage of GDP — with the wealthier countries better insured than others — Webb noted that insurance companies need to “quantify and develop products that meet all criteria of insurability.” (See chart below.)

Author(s): James P. Lynch

Publication Date: 16 Jan 2018

Publication Site: Actuarial Review, Casualty Actuarial Society

Insurance prices have surged across America in the past two years, with homeowner’s insurance climbing 21%, while CPI rose just 5%. (Source: Bloomberg)

Jerry Theodorou of R Street Institute is interviewed about Florida homeowners insurance.

Most insurance companies at that time assessed hurricane exposure in their portfolios by simply multiplying customer premiums by a rough factor of supposed risk, rather than tracking actual property replacement costs. “They were just very crude formulas,” she said.

So in 1987, Clark had started her own company, Applied Insurance Research, or AIR, to develop software that better estimated the potential losses from catastrophic events. Unlike the rest of the industry, she used granular data and sophisticated analyses, an approach now called catastrophe modeling. Her first computer model estimated that a Category 5 hurricane hitting Dade County could cause losses almost 10 times more than previously believed. She warned her customers about the risk in Florida, but until Hurricane Andrew, no one listened.

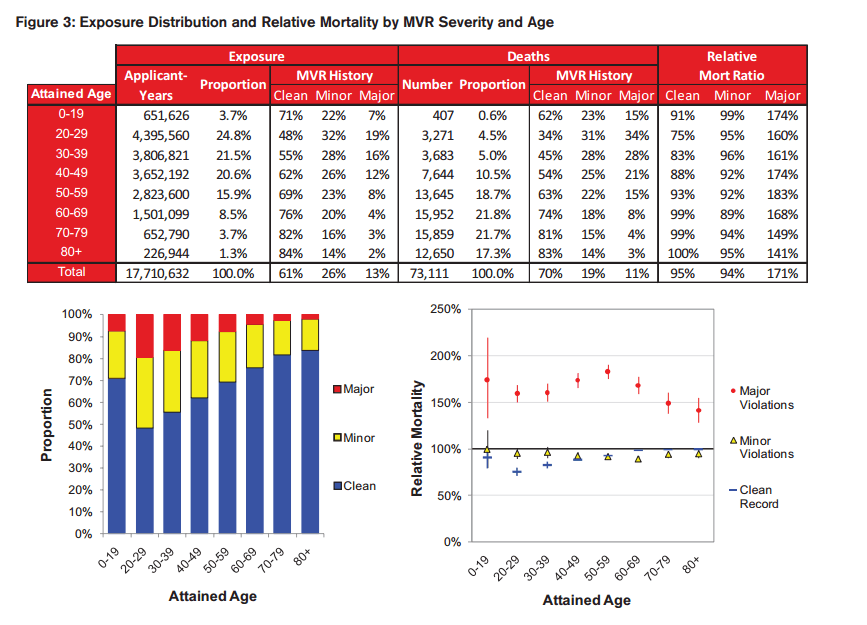

This paper analyzes the all-cause mortality experience of a large cohort of applicants linked to the number and severity of their recent driving infractions. The study verifies that significant excess mortality risk exists for applicants with a recent history of either major or frequent driving violations. The extra mortality risk for drivers with adverse MVRs is persistent across ages for both genders. The results from this study also suggest that MVRs likely have positive protective value across a wide spectrum of ages and face amounts.

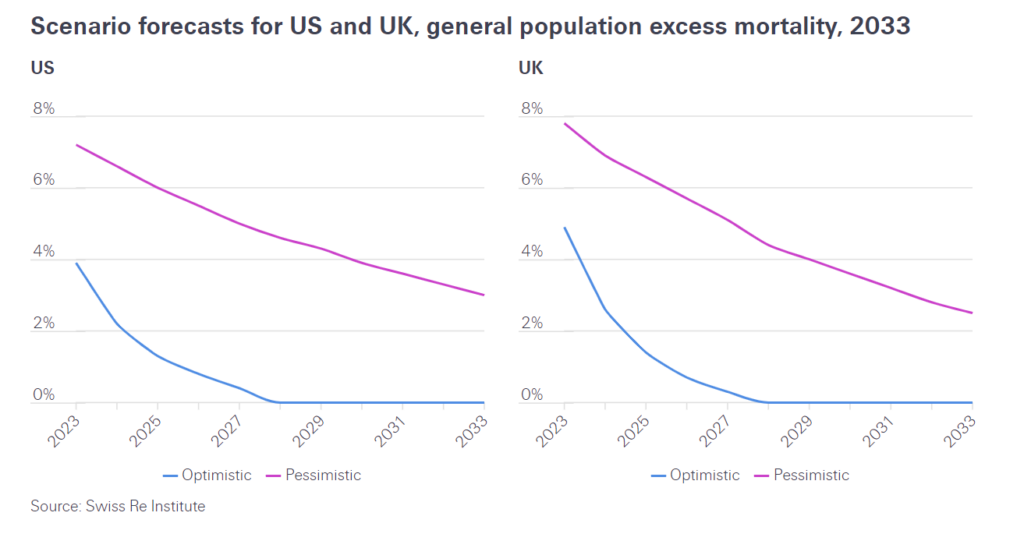

Four years on from the outbreak of the pandemic in 2020, many countries worldwide still report elevated deaths in their populations. This impact appears generally independent of healthcare systems and population health. This trend is evident even after accounting for shifting population sizes, and the range of reporting mechanisms and death classifications that make inter-country comparisons complex. There is also likely a degree of excess mortality under-reporting.

Quantifying excess mortality has been an acute challenge since 2020 due to the exceptional mortality rates of the pandemic. Excess mortality refers to the number of deaths over and above an assumed “expected” number of deaths. The different methods of estimating expected mortality can generate very different excess mortality rates.

This represents a potential challenge for Life and Health (L&H) insurance, with potentially several years of elevated mortality claims ahead, depending on how general population trends translate into the insured population. Ongoing excess mortality can have implications for L&H insurance claims and reserves. Excess mortality that continues to exceed current expectations may affect the long-term performance of in-force life portfolios as well as the pricing of new life policies.

Author(s): By Daniel Meier, Life & Health R&D Manager, CUO L&H Reinsurance & Prachi Patkee, Life & Health R&D Analyst, CUO L&H Reinsurance & Adam Strange, Life & Health R&D Manager, CUO L&H Reinsurance

Chris Swift, the chief executive officer of Hartford Financial, on Friday confirmed what government statistics seem to be showing: The U.S. death rate continues to be noticeably higher than it was before early 2020, when the COVID-19 pandemic came to light.

Swift talked about the effects of the higher U.S. mortality rate on the company’s group life insurance business Friday during a conference call with securities analysts.

He noted that mortality was much lower in the first quarter than in the first quarter of 2023, but that it was still somewhat higher than the pre-pandemic average.

“The trends are downward,” Swift said. “But we believe that we’re still operating in an endemic state of mortality, which means it’s going to be higher than normal, and we think that will continue for at least the next the next couple of years. We’ve been pricing our product with that view.”

There’s a narrow path to such ostentation for the non-famous and non-college-interested who mock the idea of an actual job. Mize found his muse in the con and his ability to rope others into it. Here’s how they say it happened: He struck when you wanted cash. When totems of the middle class were slipping from reach. When you needed a down payment. To pay off credit cards. To start a business. When asking your parents for money made you feel like a failure. When you were suffocated by medical bills, neither earning enough to pay nor poor enough for government help.

Yet money alone doesn’t completely explain why the people closest to Mize entered the ring. Mize had a way of making himself your center of gravity, the one from whom you wanted approval, mentorship, love. Mize could be fun, even thrilling. But getting all that meant pleasing him. And pleasing him meant fraud.

Some of the most chilling examples of insurance fraud are grisly affairs revealing the darkest of humanity’s dark side:

John Gilbert Graham placed a time-release bomb on a plane in which his mother was traveling, for the life insurance payment. The bomb exploded. In addition to Graham’s mother all 43 other passengers and crew perished.

Utah physician Farid Fata administered chemotherapy to hundreds of women who did not have cancer. Fata submitted $34 million in fraudulent claims to Medicare and private insurance companies.

Ali Elmezayen staged a freak car accident which took the lives of his two autistic children and nearly drowned his wife. He collected a $260,000 insurance payout, but his crime was discovered. He was sentenced to 212 years in prison.

A Chicago federal grand jury charged 23 defendants with participating in a fraud scheme swindling $26 million from ten life insurers. The scheme featured submission of fraudulent applications to obtain policies, and misrepresenting the identity of the deceased.

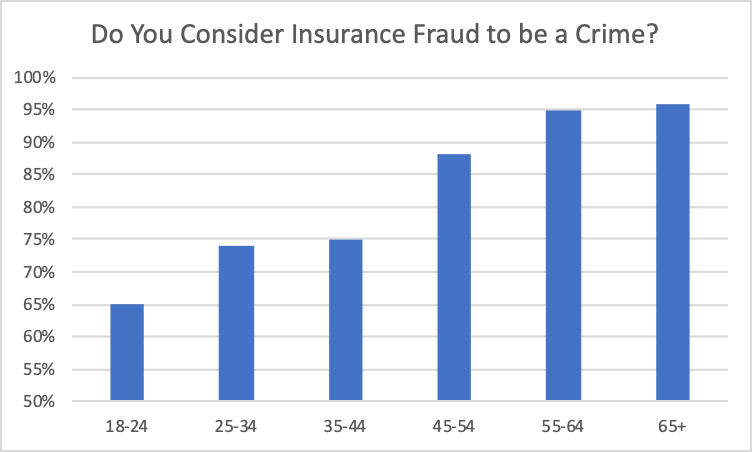

There are thousands of other equally horrific insurance fraud stories. The annual Dirty Dozen Hall of Shame report describes some of the most egregious, and contributes to an understanding of how far fraudsters will go to cheat insurance companies.

….

Improvements in predictive modeling and the introduction of artificial intelligence (AI) have strengthened insurers abilities to identify, and ultimately investigate, submitted claims that may be fraudulent. At the same time, however, AI is also being used as a weapon to penetrate insurers’ fraud detection systems. Techniques being used include AI-created fake photographs of cars of a particular make and model showing damage that is not real, but used to extract a claims payment. Some insurers are no longer accepting photos because they may be doctored, and are returning to adjustors physically visiting the allegedly damaged car. A nefarious life insurance scam includes AI-enabled manipulation of ones voice so that a criminal third party gets past insurers’ voice recognition technology, and initiates a policy being surrendered to a non-policyholder, non-beneficiary. It seems that for every additional layer of protection insurers introduce, the criminals are keeping up, if not forging ahead.

The Post Office had prosecution powers and, between 1999 and 2015, it prosecuted 700 sub-postmasters and sub-postmistresses – an average of one a week – based on information from a computer accounting system called Horizon. Another 283 cases were brought by other bodies including the Crown Prosecution Service.

Some went to prison for false accounting and theft. Many were financially ruined, even though they had repeatedly highlighted problems with the software.

After 20 years, campaigners won a legal battle to have their cases reconsidered. To date only 93 convictions have been overturned. Under government plans, victims will be able to sign a form to say they are innocent, in order to have their convictions overturned and claim compensation.

….

Horizon was introduced by the Post Office in 1999. The system was developed by the Japanese company Fujitsu, for tasks like accounting and stocktaking.

Sub-postmasters complained about bugs in the system after it falsely reported shortfalls – often for many thousands of pounds.

Some attempted to plug the gap with their own money, as their contracts stated that they were responsible for any shortfalls. Many faced bankruptcy or lost their livelihoods as a result.

Lib Dem leader Sir Ed Davey is among several politicians who have faced questions, as he was postal affairs minister in the coalition government. He said he regretted not asking “tougher questions” of Post Office managers, describing what had happened as “dreadful”.

The inquiry is hearing from Post Office investigators, Fujitsu, civil servants and others.

Author(s): By Kevin Peachey, Michael Race & Vishala Sri-Pathma

As of 2022, Citizens’ market share for homeowners multi-peril policies was approaching 20 percent, having more than doubled since 2020. As private insurers in Florida continue to go insolvent or exit the state, Citizens’ market share will likely continue to grow. At 20 percent market share, Citizens’ losses could be as high as $36 billion in the scenario studied by Swiss Re or $162 billion in the scenario studied by Cambridge and Munich Re (assuming that 60 percent of total losses are insured). If Citizens had to raise $162 billion to cover losses, that would result in an approximately $20,000 assessment for every homeowners insurance policyholder in Florida.

….

To that end, please respond to the following requests for information and documents by December 21, 2023:

1. What modeling or other analysis has Citizens done to estimate its total potential exposure to various worst case hurricane scenarios? What is the upper range of Citizens’ potential losses? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ potential losses.

2. What modeling or other analysis has Citizens done to estimate its market share over the next decade? What does Citizens project its market share to be in each of the next 10 years? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ future market share.

3. What modeling or other analysis has Citizens done to determine its ability to fully pay out claims resulting from various loss scenarios? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ financial position and (in)solvency under such scenarios.

4. What are Citizens’ current assets? What is Citizens’ total reinsurance coverage? What are the maximum total claims Citizens would be able to pay out without having to levy an assessment on Florida policyholders? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ current assets, reinsurance, and ability to pay claims.

5. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Michael Yaworsky, their staffs, or any other state officials regarding Citizens’ current or future solvency? Please provide copies of these communications.

6. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials regarding what Citizens and/or the State would do if Citizens were unable to cover its losses? Please provide copies of these communications.

7. Has Citizens contemplated asking for a federal bailout if it were unable to cover its losses? Has Citizens discussed the possibility of a federal bailout with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials? Please provide copies of these communications.

First: “A Jane Street intern had what amounted to a professional obligation to take any bet with a positive expected value”? Really? I feel like, if you are a trading intern, you are really there to learn two things. One is, sure, take bets with positive expected value and avoid bets with negative expected value.

But the other is about bet sizing. As a Jane Street intern, you have $100 to bet each day, and your quasi-job is to turn that into as much money as possible. Is betting all of it (or even $98) on a single bet with a 1% edge really optimal?[6]

People have thought about this question! Like, this is very much a central thing that traders and trading firms worry about. The standard starting point is the Kelly criterion, which computes a maximum bet size based on your edge and the size of your bankroll. Given the intern’s bankroll of $100, I think Kelly would tell you to put at most $10 on this bet, depending on what exactly you mean by “this bet.”[7] Betting $98 is too much.

I am being imprecise, and for various reasons you might not expect the interns to stick to Kelly in this situation. But when I read about interns lining up to lose their entire bankroll on bets with 1% edge, I think, “huh, that’s aggressive, what are they teaching those interns?” (I suppose the $100 daily loss limit is the real lesson about position sizing: The interns who wipe out today get to come back and play again tomorrow.)

But I also think about a Twitter argument that Bankman-Fried had with Matt Hollerbach in 2020, in which Bankman-Fried scoffed at the Kelly criterion and said that “I, personally, would do more” than the Kelly amount. “Why? Because ultimately my utility function isn’t really logarithmic. It’s closer to linear.” As he tells Lewis, “he had use for ‘infinity dollars’” — he was going to become a trillionaire and use the money to cure disease and align AI and defeat Trump, sure — so he always wanted to maximize returns.

But as Hollerbach pointed out, this misunderstands why trading firms use the Kelly criterion.[8]Jane Street does not go around taking any bet with a positive expected value. The point of Kelly is not about utility curves; it’s not “having $200 is less than twice as pleasant as having $100, so you should be less willing to take big risks for big rewards.” The point of Kelly is about maximizing your chances of surviving and obtaining long-run returns: It’s “if you bet 50% of your bankroll on 1%-edge bets, you’ll be more likely to win each bet than lose it, but if you keep doing that you will probably lose all your money eventually.” Kelly is about sizing your bets so you can keep playing the game and make the most money possible in the long run. Betting more can make you more money in the short run, but if you keep doing it you will end in ruin.