Graphic:

Excerpt:

Under the old regime, the impairment was the incurred credit losses, in determining which only past events and current conditions are used. Credit losses were booked after a credit event had taken place, thus the name “incurred.” ECL and CECL require the incorporation of forward-looking information in addition to the past/current info in the calculation of impairment. There will be an allowance for credit losses since initial recognition regardless of the creditworthiness of the investment asset. The allowance can be perceived as the reserve or capital for credit risks. In practice, the allowance could be zero if there are no expected default losses for the instrument, US Treasury bonds, US Agency MBS, just to name a few.

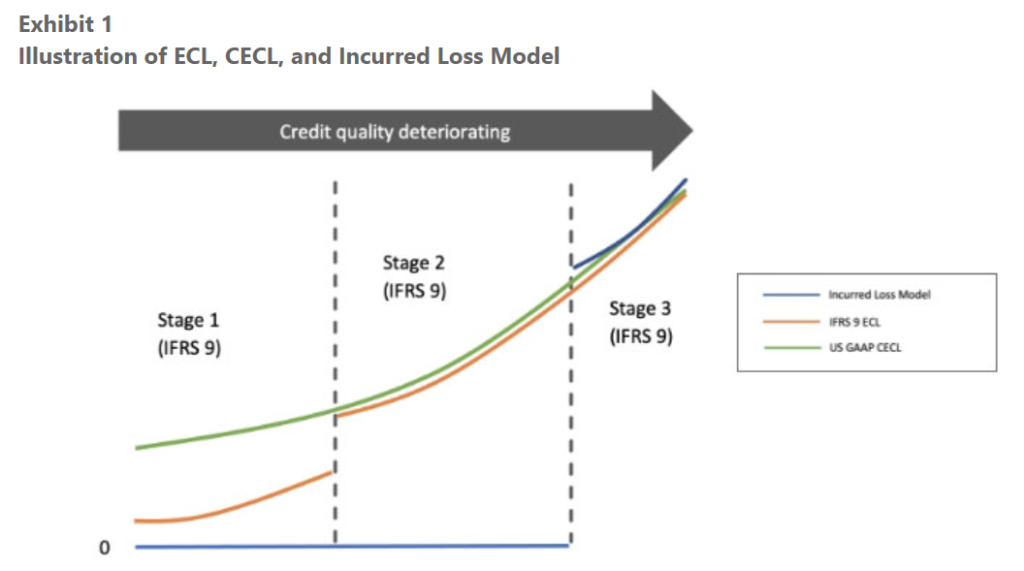

ECL under IFRS 9 is typically calculated as a probability weighted estimate of the present value of cash shortfalls over the expected life of the financial instrument. It Is an unbiased best estimate with all cash shortfalls taking into consideration the collaterals or other credit enhancement. Four typical parameters underlying its calculation are: Probability of default (PD), loss given default (LGD, i.e., 1-Recovery Rate), exposure at default (EAD) and discounting factor (DF). Prepayments, usage given default (UGD) and other parameters can also play a role in the calculations. In the general approach the loss allowance for a financial instrument is 12-month ECL regardless of credit risk at the reporting date, unless there has been a significant increase in credit risk since initial recognition: The PD is only considered for the next 12 months while the cash shortfalls are predicted over the full lifetime; as the creditworthiness deteriorates significantly, the loss allowance is increased to full lifetime ECL in Stage 2, which should always precede stage 3 (credit impairment). Even without change of stages, any credit condition changes should be flowing into the credit loss allowance via updates in some of the underlying parameters. Exhibit 1 has an illustrative comparison between ECL, CECL, and incurred loss model.

CECL is similar to ECL except FASBs doesn’t have so-called staging as IFRS 9, which requires that only 12-month ECL is calculated in stage 1 (in the general model). In other words, CECL requires a full lifetime ECL from Day 1. There are also other differences: IFRS 9 requires certain consideration of time value of money, multiple scenarios, etc., in measurement of ECL while US GAAP CECL doesn’t.

Under US GAAP, different from CECL, currently the impairment for AFS assets, while also recorded as an allowance (with a couple exceptions), is only needed for those whose fair value is less than the amortized cost. Once it is triggered, the credit losses are then measured as the excess of the amortized cost basis over the probability weighted estimate of the present value of cash flows expected to be collected. Only the fair value change related to credit is considered in the calculation of AFS impairment. The quantitative calculation behind the probability weighted best estimate is like CECL/ECL. Both can use discounted cash flow methods with parameters such as PD although one is calculating expected cash shortfalls directly in CECL and the other is calculating the expected collectible cash payments and then is used to back out the impairment.

Author(s): Jing Fritz

Publication Date: September 2022

Publication Site: Risk Management newsletter, SOA