There are many books about spreadsheets out there. Most of these books will tell you things like “How to save a file” and “How to make a graph” and “How to compute the present value of a stream of cashflows” and “How to use conjoint analysis to figure out which features you should add to the next version of your company’s widgets in order to impress senior management and get a promotion and receive a pay raise so you can purchase a bigger boat than your neighbor has.”

This book isn’t about any of those. Instead, it’s about how to Think Spreadsheet. What does that mean? Well, spreadsheets lend themselves well to solving specific types of problems in specific types of ways. They lend themselves poorly to solving other specific types of problems in other specific types of ways.

Thinking Spreadsheet entails the following:

Understanding how spreadsheets work, what they do well, and what they don’t do well.

Using the spreadsheet’s structure to intelligently organize your data.

Solving problems using techniques that take advantage of the spreadsheet’s strengths.

Building spreadsheets that are easy to understand and difficult to break.

To help you learn how to Think Spreadsheet, I’ve collected a variety of curious and often whimsical examples. Some represent problems you are likely to encounter out in the wild, others problems you’ll never encounter outside of this book. Many of them we’ll solve multiple times. That’s because in each case, the means are more interesting than the ends. You’ll never (I hope) use a spreadsheet to compute all the prime numbers less than 100. But you’ll often (I hope) find useful the techniques we’ll use to compute those prime numbers, and if you’re clever you’ll go away and apply them to all sorts of real-world problems. As with most books of this sort, you’ll really learn the most if you recreate the examples yourself and play around with them, and I strongly encourage you to do so.

Author(s): Joel Grus

Publication Date: originally in dead-tree form 2010, accessed 29 Oct 2022

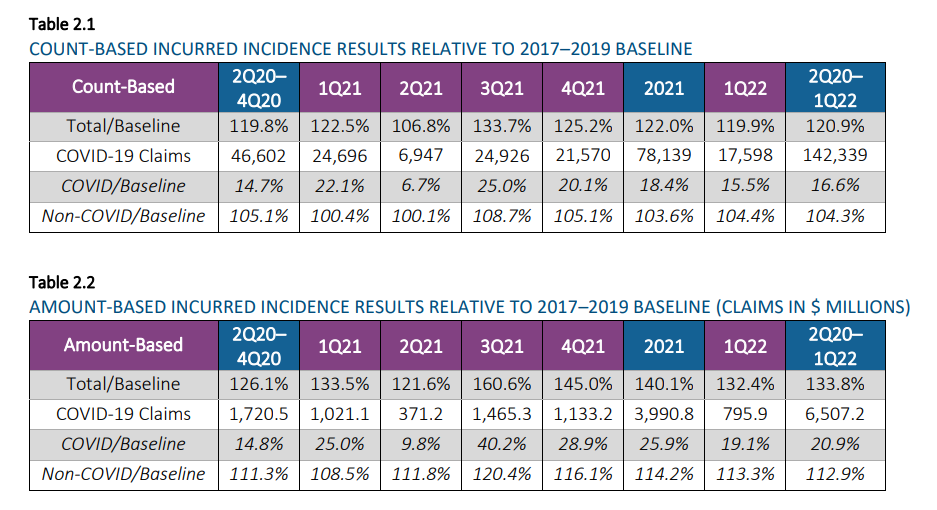

Tables 2.1 through 2.41 display high-level incidence results for the second quarter of 2020 through the first quarter of 2022 compared to the 2017-2019 baseline period for each combination of (a) incurred/reported basis and (b) count/amount basis as of March 31, 2022. In these tables, the number of COVID-19 claims has not been adjusted for seasonality, but the ratios to baseline have been adjusted for seasonality.

Note that additional data reported in April and May 2022 indicated that the 1Q 2022 excess mortality would likely complete downward from the 19.9% shown below using March data. The fully complete 1Q 2022 excess mortality is expected to remain above 15%.

….

The 24-month period of April 2020 through March 2022 showed the following Group Life mortality results: • Estimated reported Group Life claim incidence rates were up 20.0% on a seasonally-adjusted basis compared to 2017–2019 reported claims. • Estimated incurred Group Life incidence rates were 20.9% higher than baseline on a seasonally-adjusted basis. As noted above, the incurred incidence rates in February and March 2022 are based on fairly incomplete data, so they are subject to change and should not be fully relied upon at this point.

Author(s):

Thomas J. Britt, FSA, MAAA Paul Correia, FSA, MAAA Patrick Hurley, FSA, MAAA Mike Krohn, FSA, CERA, MAAA Tony LaSala, FSA, MAAA Rick Leavitt, ASA, MAAA Robert Lumia, FSA, MAAA Cynthia S. MacDonald, FSA, MAAA, SOA Patrick Nolan, FSA, MAAA, SOA Steve Rulis, FSA, MAAA Bram Spector, FSA, MAAA

Debate now rages about whether the Federal Reserve should continue to raise interest rates to tame inflation or slow down these hikes and see what happens. This is not the first debate we’ve had recently about inflation and Fed actions. The lesson we should learn, and I fear we won’t, is that government officials and those advising them from inside or outside the government don’t know as much as they claim to about the interventions they design to control the economy.

As a reminder, in 2021, the dominant voices including Fed Chairman Jerome Powell asserted that the emerging inflation would be “transitory” and disappear when pandemic-induced supply constraints dissolve. That was wrong. When this fact became obvious, the messaging shifted: Fed officials could and would fight inflation in a timely manner by raising rates to the exact level needed to avoid recession and higher unemployment. Never mind that the whole point of raising interest rates is precisely to soak money out of the economy by slowing demand, which often causes unemployment to rise.

…..

Over at Discourse magazine, my colleague Thomas Hoenig—a former president of the Fed’s Kansas City branch—explains how Fed officials faced similar pressures during the late 1960s and 1970s. Unfortunately, he writes, “Bowing to congressional and White House pressure, [Fed officials] held interest rates at an artificially low level….What followed was a persistent period of steadily higher inflation, from 4.5% in 1971 to 14% by 1980. Only then did the [Federal Reserve Open Market Committee], under the leadership of Paul Volcker, fully address inflation.”

Often overlooked is Volcker’s accomplishment: the willingness to stay the course despite a painful recession. Indeed, it took about three years from when he pushed interest rates up to about 20 percent in 1979 for the rate of inflation to fall to a manageable level. As such, Hoenig urges the Fed to stay strong today. He writes, “Interest rates must rise; the economy must slow, and unemployment must increase to regain control of inflation and return it to the Fed’s 2% target.” There is a cost in doing this; a soft landing was never in the cards.

Republicans have seized upon the issues of net-zero and environmental, social and governance investing to call attention to what they claim are negative effects of so-called ‘woke’ orthodoxy on portfolio performance, and harm the U.S. energy industry.

They have also raised the potential for a lapse in fiduciary duty by arguing that allocating towards long-term ESG goals may create short-term underperformance, harming plan beneficiaries.

The attorneys general of 14 states – Arizona, Arkansas, Indiana, Kansas, Kentucky, Louisiana, Mississippi, Missouri, Montana, Nebraska, Oklahoma, Tennessee, Texas, Virginia, and five more that have joined but can’t be named due to state laws or regulations regarding confidentiality –have sent civil investigative demands to the six U.S. banks the investigation targets

The six banks did not respond to requests for comment.

The coalition argues that the banks’ membership in the Net-Zero Banking Alliance is damaging U.S. energy companies. The CIDs, similar to subpoenas, are legally enforceable requests for information related to state or federal investigations.

FRIES: There are ten terms in this glossary: Net Zero, Carbon Offsets, Nature-Based Solutions, Zero Deforestation, Climate Smart Agriculture, Agriculture 4.0 (or the Fourth Industrial Revolution), Regenerative Agriculture, Carbon Farming, Bioeconomy and last but not least Green Finance. This then is what you identify as key greenwashing concepts and false solutions used by food and agribusiness corporations?

KUYEK: Yes. And some of the terms are not just being used by Big Food and Ag alone. There are terms that are being used by corporations from other sectors as well. But they are a big part of the greenwashing that agribusiness is involved in.

…..

NET ZERO

KUYEK: Well, net zero refers to the Paris Agreement, the COP in Paris from several years ago, where countries agreed to achieve net zero emissions by 2050. And what that meant was that they would reduce emissions (it was supposed to mean they would reduce emissions) as close to zero as possible.

And then any remaining emissions would be absorbed from the atmosphere. Now, how much would be remaining and how that would be absorbed is not defined. And certainly at this point, the technologies that are being talked about and stuff is definitely not proven. But there was that.

And then it was also not discussed that if there are some emissions, well, what are those emissions for? Of course, you’d only want those to be for the most essential services or to fulfill the most basic needs of people. But the corporations have really used that as an open door to come forward with their own idea of net zero.

….

And then as a way to get to that net zero (which they’re claiming that they’ll be able to do), they are relying heavily on offsets. What is called carbon offsets. Meaning that they will invest or they’ll purchase credits of projects or technologies that are able to absorb carbon from the atmosphere

And an increasing amount of these sort of offset projects are based on land and forests. On the idea that if you say protect a forest from being deforested or you plant trees or you even engage in some kinds of agricultural practices that are set to store carbon in the soil, that through that (if a company purchases or pays for that) then they can offset their own emissions.

So really it becomes just this way for them to continue with business as usual.

Maybach is unpaid, a volunteer among a cadre organized by Faith in Action in Red Wing, a nonprofit that relies on retirees to ferry residents to essential services.

The riders, mostly seniors, are people who don’t have immediate access to transportation, especially in rural areas where public transit options are either limited or nonexistent.

There are several such programs serving rural counties in Minnesota, but, as with other services across the country, their existence has become precarious because the number of volunteer drivers has steadily declined, according to transportation advocates. Volunteers either get to a point where, because of age, they can no longer drive, or the costs associated with their volunteerism are no longer sustainable. For decades, Congress has refused to increase the rate at which the drivers’ expenses can be reimbursed.

Experts say that with public transit in rural areas already insufficient and the long distances that residents in rural communities must travel to access health care, a decimated volunteer driver network would leave seniors with even fewer transportation options and could interrupt their health management. Already, social service organizations that rely on volunteers have begun to restrict their service options and deny ride requests when drivers aren’t available.

….

Volunteers, like Maybach, are eligible for a reimbursement of 14 cents per mile, which generally doesn’t come close to covering the cost of gas and wear and tear on a vehicle. And while the Internal Revenue Service increased the business rate from 58.5 cents per mile to 62.5 cents per mile in June, it did not raise the charitable rate because it is under Congress’ purview and must be set by statute. The charitable rate was last changed in 1997.

Raising interest rates won’t just push Britain into a recession and make the cost-of-living crisis worse for working-class people — it will discourage badly needed investments in green energy, undermining the UK’s efforts to address climate change.

….

The theory goes that higher interest rates help bring inflation down by making credit more expensive across the economy and reducing the amount of money firms and families have to spend on goods and services, thereby slowing price increases. But our inflation is predominantly driven by external factors, most notably high gas prices resulting from COVID-19 supply issues and the war in Ukraine. Instead, the bank’s policy is likely to push the UK economy into a recession, without addressing the main underlying causes of rising prices. That also means higher costs of borrowing for the very investments we need to reduce our reliance on costly fossil gas, like wind farms and home insulation.

To compound the problem, higher interest rates discourage investment in clean projects more than dirty ones. Running renewables doesn’t cost much: they rely on free wind and solar energy instead of expensive fossil fuels. But building them in the first place does come with high initial costs, meaning they are particularly impacted by the higher costs of credit. Similarly, insulation and heat pumps need to be paid for up front, before they begin to lower energy bills for households. Demand for improvements like heat pumps is significantly influenced by the availability of cheap loans to cover the initial installation costs.

A recent webinar held by the National Institute on Retirement Security, in conjunction with consulting firm Segal and Lazard Asset Management, reviewed the report “Examining the Experience of Public Pension Plans Since the Great Recession,” which examines how public retirement plans weathered the period’s market and made subsequent changes to public pension funds to ensure their long-term sustainability.

Most plans recovered their losses between 2011 and 2014, three to six years after the market bottom. Despite the recession and subsequent loss of value, plans continued to pay out over a trillion dollars in benefits to subscribers during the period.

Todd Tauzer, vice president at Segal, says that since 2008, the models and risk assessment strategies of public plans have evolved greatly. Tauzer says, “funding status alone does not indicate health of a public pension, after all, one cannot see the underlying assumptions used. A plan’s funding status can be measured in many different ways, and the ways we measure can change over time.”

“Plans today are on a much stronger measurement of liability than they were 15 years ago,” according to Tauzer. Adjustments to the assumption of the models in mortality, the assumed rate of return, general population counts, and the assumed rate of inflation are a few of the assumptions modified which give greater clarity into pension health post-GFC.

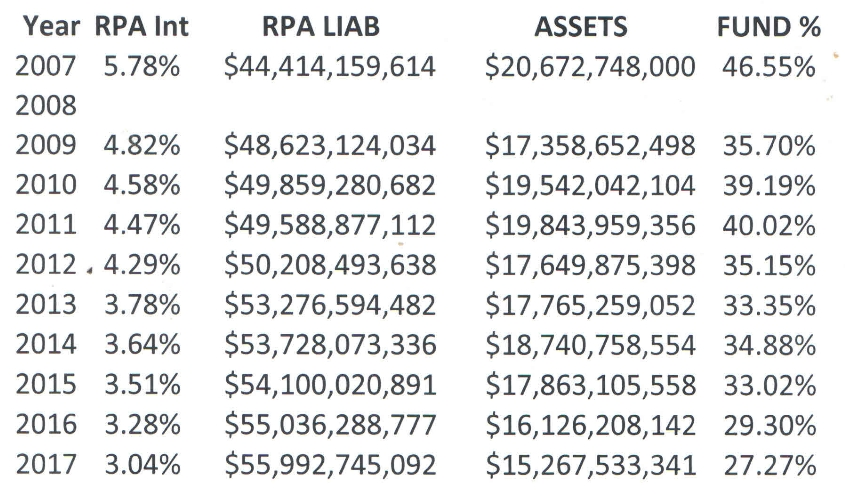

With the 5500 filing season done it is time to tentatively get back to some blogging – starting with the plan that was likely to bring the PBGC (and the entire private pension system) down before the SFA bailout and now will be another cog in the hyperinflation wheelbarrow.

We had some 5500 history in an earlier blog through 2016. This is where the plan was last year based on their 5500 filing for 2021:

Plan Name: Central States, Southeast & Southwest Areas Pension Plan

EIN/PN: 36-6044243/001

Total participants @ 12/31/21: 357,056 including:

Retirees: 189,449

Separated but entitled to benefits: 117,511

Still working: 50,096

Asset Value (Market) @ 1/1/21: 10,409,440,502

Value of liabilities using RPA rate (2.43%) @ 1/1/21: $58,623,837,073 including:

Retirees: $34,084,275,398

Separated but entitled to benefits: $15,801,905,005