Workers born after 1970 have been told they need to keep going for another three years — and many are not happy

Denmark has raised its retirement age to 70 for everyone born after 1970, becoming the first European country to reach the symbolic threshold.

While other nations are bogged down in seemingly intractable political battles over increasing the state pension age, the Danes are following a long-established principle that it should go up broadly in line with life expectancy. The average for Danes is 81.7 years. The legislation was passed with an overwhelming majority in the Danish parliament.

However, there is a good deal of public unease at the plan to oblige many people to keep working until the end of their seventh decade. Some MPs look aghast at projections that the retirement age could rise as high as 77.

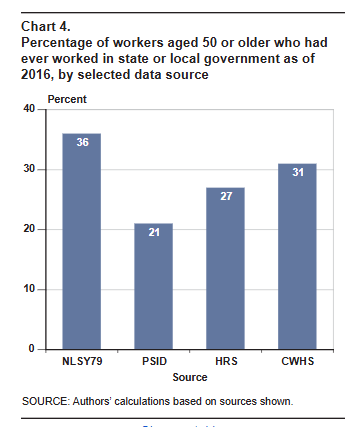

Analysis based on a synthetic population of noncovered state and local government workers confirms earlier results based on a sample of retirement plan benefit formulas: Workers with medium-length government tenures are at risk of receiving lifetime retirement income that falls short of Social Security equivalence. Given the distributions of the synthetic population of noncovered workers by occupation, retirement-plan benefit formula, and tenure in government employment, this translates to about 16 percent of all noncovered workers at risk of receiving less retirement income than they would have received from Social Security alone had they spent their whole careers in covered employment.

Although the share of workers with projected retirement benefits that fall short of Social Security equivalence is not large, the problem is serious. Social Security is intended to provide a minimum level of retirement income for all Americans. Covered public-sector workers and many private-sector workers augment their Social Security benefits with employer-sponsored retirement plans. The concern is that pension benefits ultimately will not meet that minimum level for 750,000 to 1 million noncovered workers annually who cannot augment those benefits with Social Security income.

Author(s): Jean-Pierre Aubry, Siyan Liu, Alicia H. Munnell, Laura D. Quinby, and Glenn R. Springstead

Social Security Bulletin, Vol. 82 No. 3, 2022 (released August 2022)

When planning for retirement, it’s important to consider all the risks, and one consideration that individuals often overlook is “longevity risk.” Longevity risk refers to the chance a person could outlive their savings. Understanding longevity and reasonably estimating the probabilities of living to various advanced ages and the risk of outliving resources are important for planning a secure retirement.

As a result of healthy lifestyles, medical advancements and scientific discoveries, it has become much more common for people these days to live into their 80s and 90s — or even their 100s! In fact, Pew Research Center writes that, according to estimates by the U.S. Census Bureau, there are about 101,000 centenarians in the U.S. in 2024, and this population could quadruple to about 422,000 in 2054.

While a long life is something most people desire, it requires planning for a longer retirement than in the past. For example, if a worker retires at 67, planning for a 20-year retirement may not be enough, and if they live to be in their 90s, or even past 100, they could outlive their savings or end up with fewer assets to leave their heirs.

This year is a major milestone for the retirement industry as the Employee Retirement Income Security Act of 1974 (ERISA) reaches its 50th anniversary today.

ERISA is the federal law that for the first time set important standards for most voluntarily established retirement and health plans in the private sector to protect individual participants and beneficiaries. Key provisions of ERISA require plans to provide participants with essential plan information; set minimum standards for participation, vesting, benefit accrual, and funding; establish fiduciary responsibilities for those who manage plan assets; and guarantee payment of benefits through the Pension Benefit Guaranty Corporation (PBGC) for terminated defined benefit pension plans.

There are numerous ERISA successes to celebrate, but there also are challenges associated with the law that can be addressed to help create better retirement outcomes in the future.

Major Successes of ERISA

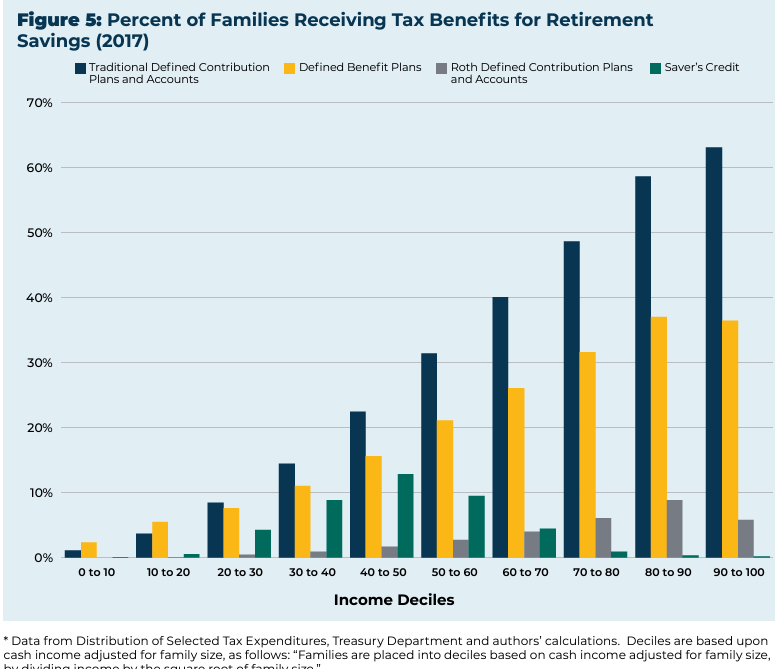

ERISA has helped Americans prioritize saving for retirement through employer plans at a key juncture when people are living longer. When ERISA was enacted, defined benefit pension plans were the primary type of retirement plan offered by private sector employers.

Thanks in part to ERISA, U.S. pension plans have paid out roughly $8.7 trillion dollars to America’s seniors just since 2009. According to the Investment Company Institute, another $12 trillion in assets are held by pension plans that invest and manage these funds for the benefit of 25 million retirees and millions of workers. Pensions continue to do much of the heavy lifting to preserve a reasonable standard of living for retirees by supplementing Social Security benefits.

Another success of ERISA is that it provides a wide range of protections to workers to ensure retirement assets go toward workers’ retirement benefits and employers are adequately funding these plans. ERISA also created a federal insurance program directed by the PBGC that protects retirement benefits, even if a plan closes or a company goes out of business. Importantly, the program is funded by premiums paid by pension funds, not taxpayers. Typically, the PBGC steps in to oversee plan assets and ensure payment of benefits after a firm ceases to exist. This has proven to be an incredibly successful program, protecting millions of retirees and their beneficiaries.

Author(s): Dan Doonan

Dan Doonan is executive director of the National Institute on Retirement Security, a non-partisan, non-profit research think tank located in Washington, D.C. Dan has been a Forbes Contributor since 2021, and he has more than 25 years of experience on retirement issues from a variety of vantage points – an analyst, consultant and plan trustee. His work is driven by the belief that everyone has a shared interest in a strong and resilient retirement infrastructure in the U.S. that provides sufficient retirement income in the most cost-efficient manner possible. Dan holds a B.S. in Mathematics from Elizabethtown College and is a member of the National Academy of Social Insurance.

Are we all really living longer? Let’s first point out that Princeton economists Anne Case and Angus Deaton, noted for their research in health and economics, recently showed that many Americans are not, in fact, enjoying extended lives. As they stated in their own New York Times op-ed, those without college degrees are “scarred by death and a staggeringly shorter life span.” According to their investigation, the expected lifespan for this group has been falling since 2010. By 2021, people without college degrees were expected to live to about 75, nearly 8.5 years shorter than their college-educated counterparts.

Overall life expectancy in America dropped in 2020 and 2021, with increases in mortality across the leading causes of death and among all ages, not just due to COVID-19. In August 2022, data confirmed that Americans are dying younger across all demographics. Again, the U.S. is an outlier. It was one of two developed countries where life expectancy did not bounce back in the second year of the pandemic.

So the argument that everyone is living longer greatly stretches the truth—unless, of course, you happen to be rich: A Harvard study revealed that the wealthiest Americans enjoy a life expectancy over a decade longer than their poorest counterparts.

Could the idea that working into our seventies and beyond boosts our health and well-being hold true? Obviously, for those in physically demanding roles, such as construction or mining, prolonged work is likely to lead to a higher risk of injury, accidents, and wearing down health-wise. But what about everybody else? What if you have a desk job? Wouldn’t it be great to get out there, do something meaningful, and interact with people, too?

Perhaps it’s easy for people like Steuerle and Kramon to imagine older people working in secure, dignified positions that might offer health benefits into old age – after all, those are the types of positions they know best.

But the reality is different. Economist Teresa Ghilarducci, a professor at the New School for Social Research, focuses on the economic security of older workers and flaws in U.S. retirement systems in her new book, Work, Retire, Repeat: The Uncertainty of Retirement in the New Economy. She calls those praising the health perks of working longer “oddballs” – those fortunate folks in cushy positions who have a lot of autonomy and purpose. Like lawmakers or tenured professors, for example.

Author(s): Lynn Parramore

Publication Date: 8 May 2024

Publication Site: Institute for New Economic Thinking

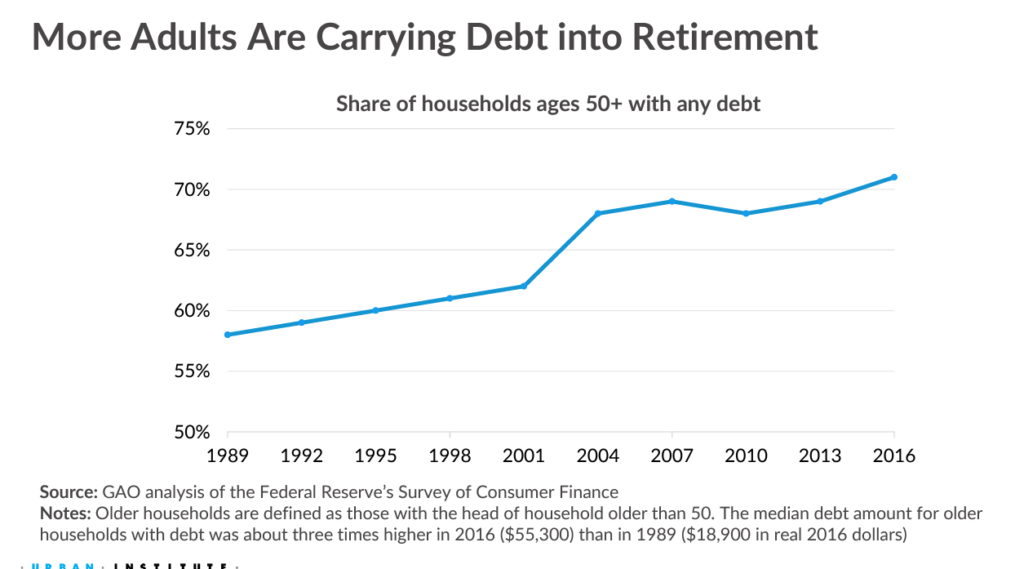

One factor undermining older Americans’ ability to prepare financially for retirement is the debt burden they carry. Increasingly, adults are carrying debt into retirement, according to Mingli Zhong, research associate, and Jennifer Andre, data scientist at the Urban Institute.

The authors also reported racial disparities in debt levels. Compared to an older adult in a majority-white community, a typical older adult in a community of color is more likely to have any type of delinquent debt, carry a higher balance of total delinquent debt, and have a higher balance of medical debt in collections. The older adult living in a majority-white area has a higher balance of delinquent student loan debt and delinquent credit card debt, they also found.

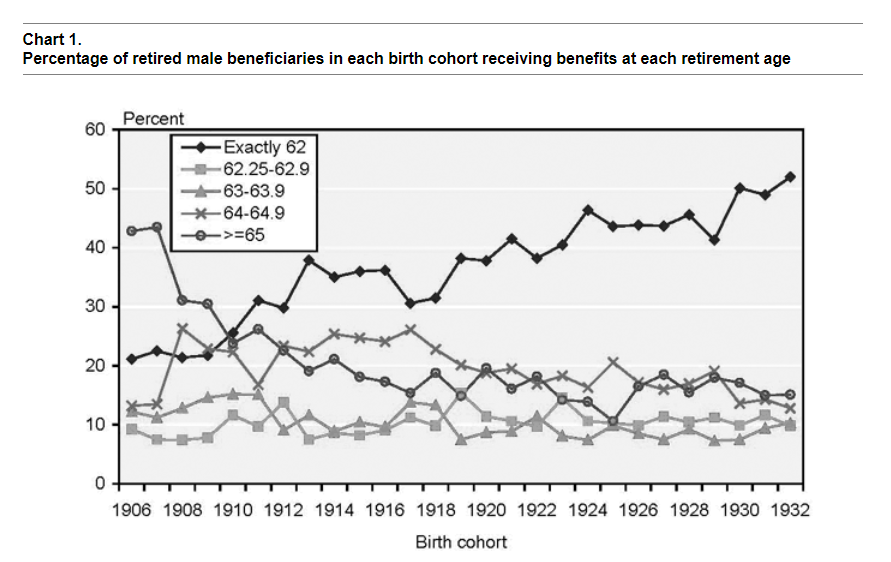

In this paper I use the 1973 cross-sectional Current Population Survey (CPS) matched to longitudinal Social Security administrative data (through 1998) to examine the relationship between retirement age and mortality for men who have lived to at least age 65 by year 1997 or earlier.1 Logistic regression results indicate that controlling for current age, year of birth, education, marital status in 1973, and race, men who retire early die sooner than men who retire at age 65 or older. A positive correlation between age of retirement and life expectancy may suggest that retirement age is correlated with health in the 1973 CPS; however, the 1973 CPS data do not provide the ability to test that hypothesis directly.

Regression results also indicate that the composition of the early retirement variable matters. I represent early retirees by four dummy variables representing age of entitlement to Social Security benefits—exactly age 62 to less than 62 years and 3 months (referred to as exactly age 62 in this paper), age 62 and 3 months to 62 and 11 months, age 63, and age 64. The reference variable is men taking benefits at age 65 or older. I find that men taking benefits at exactly age 62 have higher mortality risk than men taking benefits in any of the other four age groups. I also find that men taking benefits at age 62 and 3 months to 62 and 11 months, age 63, and age 64 have higher mortality risk than men taking benefits at age 65 or older. Estimates of mortality risk for “early” retirees are lowered when higher-risk age 62 retirees are combined with age 63 and age 64 retirees and when age 62 retirees are compared with a reference variable of age 63 and older retirees. Econometric models may benefit by classifying early retirees by single year of retirement age—or at least separating age 62 retirees from age 63 and age 64 retirees and age 63 and age 64 retirees from age 65 and older retirees—if single-year breakdowns are not possible.

The differential mortality literature clearly indicates that mortality risk is higher for low-educated males relative to high-educated males. If low-educated males tend to retire early in relatively greater numbers than high-educated males, higher mortality risk for such individuals due to low educational attainment would be added to the higher mortality risk I find for early retirees relative to that for normal retirees. Descriptive statistics for the 1973 CPS show that a greater proportion of age 65 retirees are college educated than age 62 retirees. In addition, a greater proportion of age 64 retirees are college educated than age 62 retirees, and a lesser proportion of age 64 retirees are college educated than age 65 or older retirees. Age 63 retirees are only slightly more educated than age 62 retirees.

Despite a trend toward early retirement over the birth cohorts in the 1973 CPS, I do not find a change in retirement age differentials over time. However, I do find a change in mortality risk by education over time. Such a change may result from the changing proportion of individuals in each education category over time, a trend toward increasing mortality differentials by socioeconomic status, or a combination of the two.

This paper does not directly explore why a positive correlation between retirement age and survival probability exists. One possibility is that men who retire early are relatively less healthy than men who retire later and that these poorer health characteristics lead to earlier deaths. One can interpret this hypothesis with a “quasidisability” explanation and a benefit optimization explanation. Links between these interpretations and my analysis of the 1973 CPS are fairly speculative because I do not have the appropriate variables needed to test these interpretations.

A quasi-disability explanation, following Kingson (1982), Packard (1985), and Leonesio, Vaughan, and Wixon (2000), could be that a subgroup of workers who choose to take retired-worker benefits at age 62 is significantly less healthy than other workers but unable to qualify for disabled-worker benefits. An econometric model with a mix of both these borderline individuals and healthy individuals retiring at age 62 and with almost no borderline individuals retiring at age 65 could lead to a positive correlation between retirement and mortality, even if a greater percentage of individuals who retire at age 62 are healthy than unhealthy. Evidence for this hypothesis can be inferred from the finding that retiring at exactly age 62 increases the odds of dying in a unit age interval by 12 percent relative to men retiring at 62 and 3 months to 62 and 11 months for men in the 1973 CPS. In addition, retiring exactly at age 62 increases the odds of dying by 23 percent relative to men retiring at age 63 and by 24 percent relative to men retiring at age 64. A group with relatively severe health problems waiting for their 62nd birthday to take benefits could create this result.

An explanation based on benefit optimization follows Hurd and McGarry’s research (1995, 1997) in which they find that individuals’ subjective survival probabilities roughly predict actual survival. If men in the 1973 CPS choose age of benefit receipt based on expectations of their own life expectancy, then perhaps a positive correlation between age of retirement and life expectancy implies that their expectations are correct on average. If actuarial reductions for retirement before the normal retirement age are linked to average life expectancy and an individual’s life expectancy is below average, it may be rational for that individual to retire before the normal retirement age. Evidence for this hypothesis can be inferred from the fact that men retiring at age 62 and 3 months to age 62 and 11 months, age 63, and age 64 all experience greater mortality risk than men retiring at age 65 or older. If only men with severe health problems who are unable to qualify for disability benefits are driving the results, we probably would not expect to see this result. We might expect most of these individuals to retire at the earliest opportunity (exactly age 62).2

Author(s): Hilary Waldron

Publication Date: August 2001

Publication Site: Social Security Office of Policy, ORES Working Paper No 93

Before she exited the Republican primary race, Nikki Haley advocated gradually increasing the retirement age to match the growth in life expectancy. Her political rivals swiftly criticized her proposal, but it enjoys widespread support among those looking to rein in soaring entitlement costs. A new book by economist Teresa Ghilarducci, Work, Retire, Repeat, offers reasons to seek an alternative path to reform.

Pay-as-you-go retirement systems such as Social Security or Medicare use taxes on current workers to pay benefits to retirees. Even if individuals on average fully pay for what they later get, such an arrangement will not be sustainable if declining birth rates and rising life expectancy reduce the ratio of workers to retirees. In 1960, there were five workers for each retiree. By 2000, the ratio had fallen to three-to-one. By 2040, there will be only two workers for each retiree. Raising the retirement age would both reduce the cost of benefits and increase payroll tax revenues to pay for them.

But Ghilarducci’s book argues against pushing back retirement. She suggests that, whereas policymaking elites view retirement as boring, low-paid workers typically can’t wait for relief from “heavy lifting, crushing work schedules, arbitrary changes in work duties, and the fear of being laid off.”

Ghilarducci acknowledges that employment can be a valuable source of meaning, personal identity, achievement, social interaction, and structure in people’s lives. But she disputes the claim that the correlation of retirement with declining mental health proves that it is bad for people.

….

By allowing younger workers to opt for a lower payroll tax rate for the remainder of their careers, in return for a uniform safety-net benefit when they reach retirement, Social Security could be made more effective at preventing poverty while also being less of a burden on the young. Such a benefit structure would likely also motivate higher-earning workers to retire later than the poor—the arrangement for which Ghilarducci provides her strongest arguments.

A “pension dashboard” could be useful in the United States to help participants track their retirement savings when they change jobs, but Congress would need to authorize a federal agency to establish and oversee such a dashboard. It also would have to give the agency the authority to consolidate retirement account information, the GAO stated in its report—“401(k) Plans: Additional Federal Actions Would Help Participants Track and Consolidate Their Retirement Savings.”

GAO was asked to review, among other things, the challenges that 401(k) plan participants have in keeping track of their retirement savings, as well as the challenges they have in rolling over their savings from one plan to another and federal actions that can improve the process.

In fact, this issue is not new, as the dashboard concept was raised in late 2020 in a white paper (A Retirement Dashboard for the United States) by authors David John of the AARP Public Policy Institute, Grace Enda of the Urban-Brookings Tax Policy Center, and William Gale and J. Mark Iwry of the Brookings Institution who called for the creation of a retirement dashboard to help savers better manage and keep track of their savings.

….

Consequently, GAO recommends that Congress grant authority to a federal agency to develop and oversee a comprehensive pension dashboard that can provide participants’ information to them in one location. GAO notes this “would reduce the burden on plan sponsors and providers, who must otherwise track or manage lost accounts or missing participants.”

The report also suggests that DOL and IRS establish a system to facilitate automatic plan-to-plan rollovers to help participants maintain consolidated savings as they change jobs. GAO also recommended that the government (PBGC, Labor and Treasury) help 401(k) participants by improving the information they receive about options for their plan savings and the process they must undergo to consolidate their savings after changing jobs.

In its written response, DOL stated that it would consider actions related to GAO’s disclosure recommendation to ensure participants “receive easily understandable, timely, and comprehensive information.” DOL also noted that it is engaged in joint agency efforts and that it would be appropriate for them to consider the recommendation as part of such efforts with Treasury, IRS, and PBGC, as required under the SECURE 2.0 Act. Under the act, the agencies are to study, analyze, and report to Congress on the effectiveness of their reporting and disclosure requirements before the end of 2025.

Author(s): Ted Godbout

Publication Date: 20 Feb 2024

Publication Site: NAPA – National Association of Plan Advisors

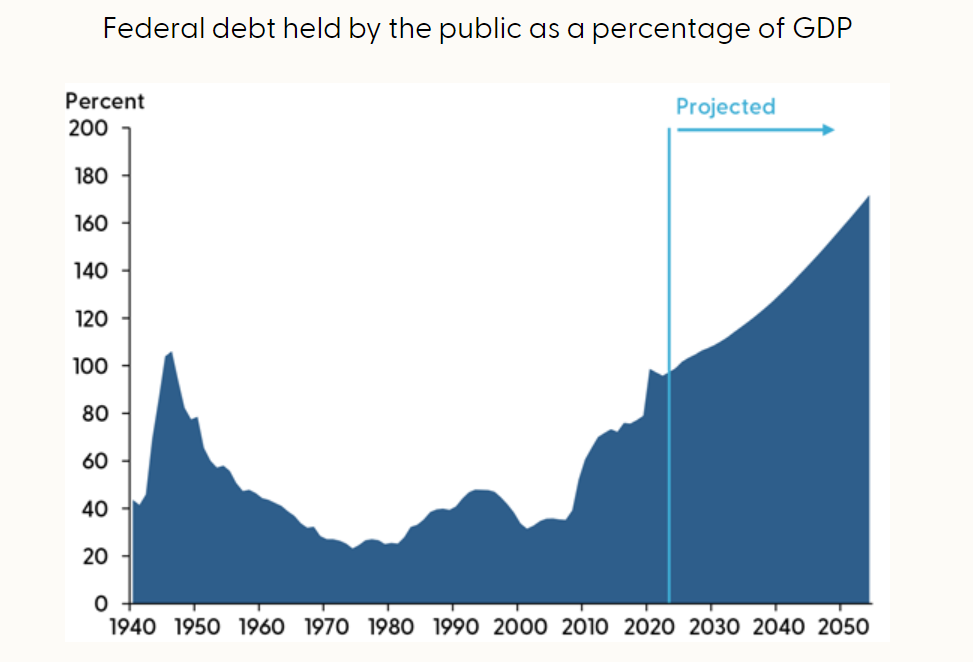

The current setup is nothing like the situation following WWII. Don’t expect another baby boom.

Instead, expect a massive wave of boomer retirements (already started) that will pressure Medicare and Social Security.

Depending on the kindness of foreigners to increase demand for US treasuries is not exactly a great plan.

Artificial Intelligence (AI) will undoubtedly increase productivity. But that is not going to offset the willingness of Congress to spend more and more money on wars, defense, foreign aid, child tax credits, free education, and other free money handouts, while trying to be the world’s policeman.

Former New York Mayor Rudy Giuliani said he regrets not taking a city pension now that he’s facing a $148m civil court payout for defaming a pair of Georgia election workers.

The former mayor has since filed for bankruptcy, according to the New York Post.

Empire Centre for Public Policy, a taxpayer watchdog group in New York, found no evidence of Mr Giuliani ever filing to receive a pension.

Had he applied, he would have been eligible for approximately $26,000 per year once he turned 62.

The former mayor would have an extra $442,000 in his coffers if he had applied for a pension.

When The New York Post asked him why he never took a pension, he suggested he was “giving back to the city I love.”

“Although I would like to take it now,” he added.

The former mayor then admitted that he also didn’t “know how to go about it.”

He also is not receiving a federal pension for the time he spent working as Manhattan’s US Attorney and for other government work he performed.

Department of Labor Inspector General Larry Turner issued a semi-annual report Tuesday arguing that the Employee Benefit Security Administration lacks both the resources and authority to fulfill its mandate to employee benefit plans. The report particularly emphasized EBSA’s limited authority to conduct thorough audits of workplace retirement plans.

My takeaways from the report:

The OIG remains concerned about the Employee Benefits Security Administration’s (EBSA) ability to protect the integrity of pension, health, and other benefit plans of about 153 million workers, retirees, and their families under the Employee Retirement Income Security Act of 1974 (ERISA). In particular, the OIG is concerned about the statutory limitations on EBSA’s oversight authority and inadequate resources to conduct compliance and enforcement. A decades-long challenge to EBSA’s compliance program, ERISA provisions allow billions of dollars in pension assets to escape full audit scrutiny. The act generally requires every employee benefit plan with more than 100 participants to obtain an audit of the plan’s financial statements each year. However, an exemption in the law allowed auditors to perform “limited-scope audits.” These audits excluded pension plan assets already certified by certain banks or insurance carriers and provided little to no confirmation regarding the actual existence or value of the assets. (page 23)