Brain fog is a colloquial term that describes a state of mental sluggishness or lack of clarity and haziness that makes it difficult to concentrate, remember things and think clearly.

Fast-forward four years and there is now abundant evidence that being infected with SARS-CoV-2 – the virus that causes COVID-19 – can affect brain health in many ways.

In addition to brain fog, COVID-19 can lead to an array of problems, including headaches, seizure disorders, strokes, sleep problems, and tingling and paralysis of the nerves, as well as several mental health disorders.

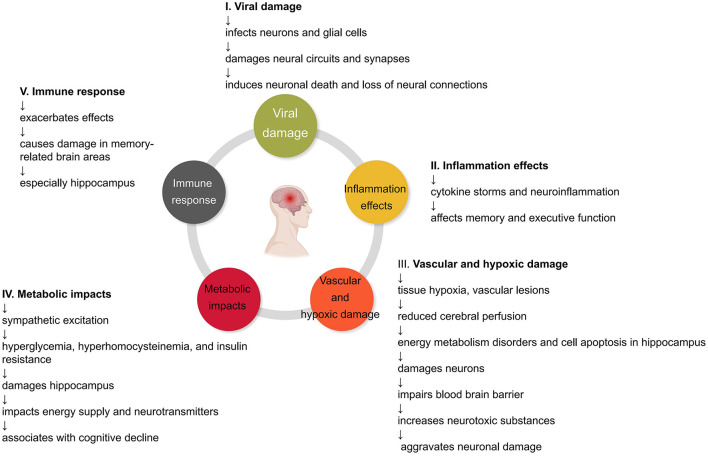

COVID-19, caused by the SARS-CoV-2 virus, is a respiratory infectious disease. While most patients recover after treatment, there is growing evidence that COVID-19 may result in cognitive impairment. Recent studies reveal that some individuals experience cognitive deficits, such as diminished memory and attention, as well as sleep disturbances, suggesting that COVID-19 could have long-term effects on cognitive function. Research indicates that COVID-19 may contribute to cognitive decline by damaging crucial brain regions, including the hippocampus and anterior cingulate cortex. Additionally, studies have identified active neuroinflammation, mitochondrial dysfunction, and microglial activation in COVID-19 patients, implying that these factors may be potential mechanisms leading to cognitive impairment. Given these findings, the possibility of cognitive impairment following COVID-19 treatment warrants careful consideration. Large-scale follow-up studies are needed to investigate the impact of COVID-19 on cognitive function and offer evidence to support clinical treatment and rehabilitation practices. In-depth neuropathological and biological studies can elucidate precise mechanisms and provide a theoretical basis for prevention, treatment, and intervention research. Considering the risks of the long-term effects of COVID-19 and the possibility of reinfection, it is imperative to integrate basic and clinical research data to optimize the preservation of patients’ cognitive function and quality of life. This integration will also offer valuable insights for responding to similar public health events in the future. This perspective article synthesizes clinical and basic evidence of cognitive impairment following COVID-19, discussing potential mechanisms and outlining future research directions.

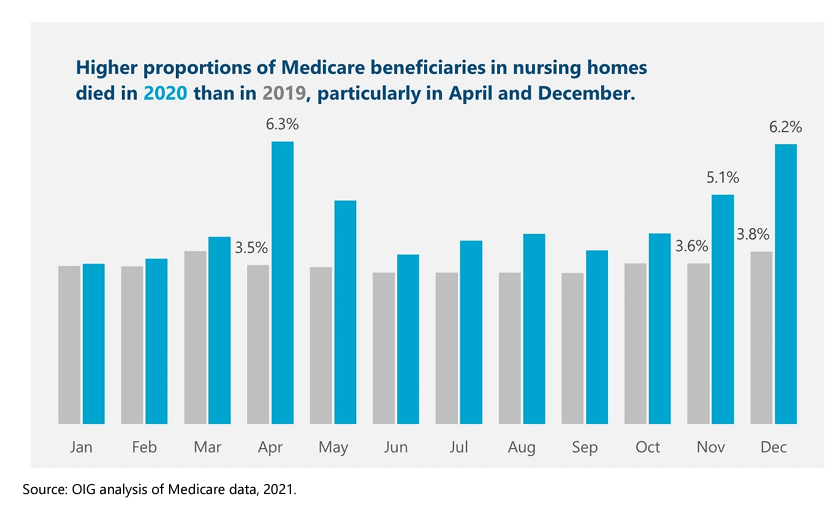

The overall mortality rate in nursing homes rose 32 percent in 2020. The pandemic had far-reaching implications for all nursing home beneficiaries, beyond those who had or likely had COVID-19. Among all Medicare beneficiaries in nursing homes, 22.5 percent died in 2020, which is an increase of one-third from 2019 when 17.0 percent of Medicare beneficiaries in nursing homes died. This 32-percent increase amounts to 169,291 more deaths in 2020 than if the mortality rate had remained the same as in 2019. Each month of 2020 had a higher mortality rate than the corresponding month a year earlier.

Almost 1,000 more beneficiaries died per day in April 2020 than in the previous year. In April 2020 alone, a total of 81,484 Medicare beneficiaries in nursing homes died. This is almost 30,000 more deaths—an average of about 1,000 per day—compared to the previous year. This increase in number occurred even though the nursing home population was smaller in April 2020. Overall, Medicare beneficiaries in nursing homes were almost twice as likely to die in April 2020 than in April 2019. In April 2020, 6.3 percent of all Medicare beneficiaries in nursing homes died, whereas 3.5 percent died in April 2019.

The mortality rates also rose at the end of 2020. In November, 5.1 percent of all Medicare beneficiaries in nursing homes died, and in December that increased to 6.2 percent. Again, these rates are markedly higher than the previous year. In November 2019, 3.6 percent of all Medicare beneficiaries in nursing homes died, and, in December 2019, 3.8 percent did.

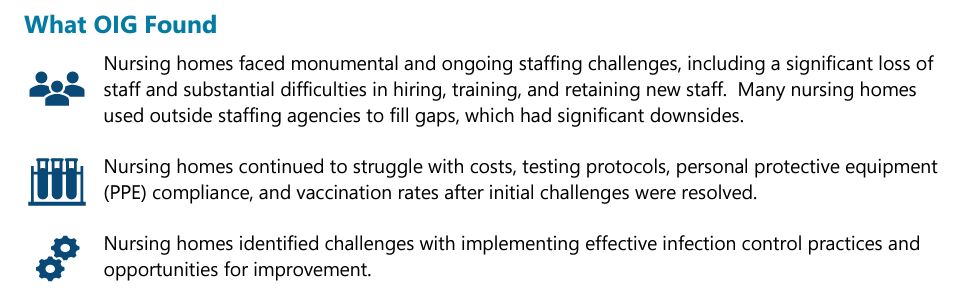

Author(s): Jenell Clarke-Whyte and team

Publication Date: June 2021

Publication Site: Office of Inspector General, HHS

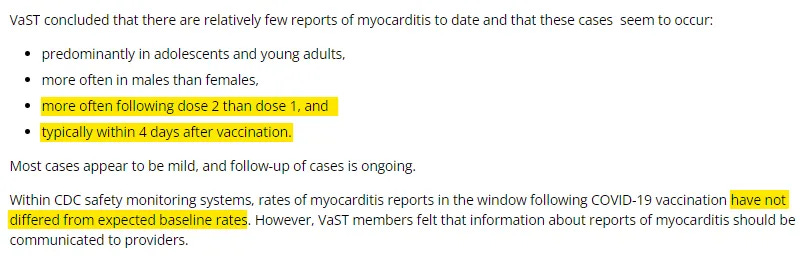

With the recent discovery that the CDC drafted — but never sent — a Health Alert in May 2021 about myocarditis after mRNA vaccination, I put together this timeline about vaccine myocarditis news and updates from government officials. I include a combination of documents from CDC and FDA, as well as what was covered in the mainstream media.

I think this timeline shows a pattern in which CDC & FDA failed to adequately investigate and inform the public about the risks of myocarditis early in the vaccine rollout. However, there was public acknowledgement by the CDC, as early as May 20, 2021, about a potential pattern of myocarditis after the 2nd dose of mRNA vaccines, particularly in young men.

On June 1, 2021, the CDC confirmed that they had identified a higher than expected signal of myocarditis for young men after mRNA vaccination, but that they still recommended Covid vaccination for everyone in this age group. Despite a lot more analysis and discussion of myocarditis after that, and a changing landscape with widespread natural immunity, the CDC & FDA position has changed very little since that time.

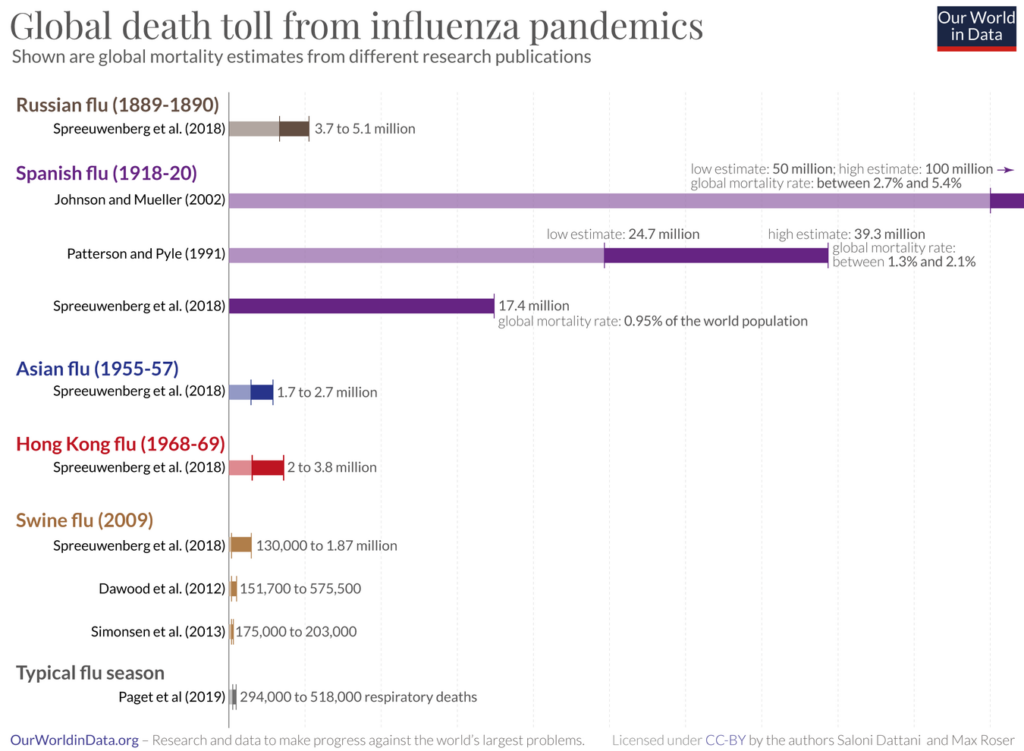

Estimates suggest that the world population in 1918 was 1.8 billion.

Based on this, the low estimate of 17.4 million deaths by Spreeuwenberg et al. (2018) implies that the Spanish flu killed almost 1% of the world population.9

The estimate of 50 million deaths published by Johnson and Mueller implies that the Spanish flu killed 2.7% of the world population. And if it was in fact higher – 100 million as these authors suggest – then the global death rate would have been 5.4%.10

The world population was growing by around 13 million every year in this period which suggests that the period of the Spanish flu was likely the last time in history when the world population was declining.11

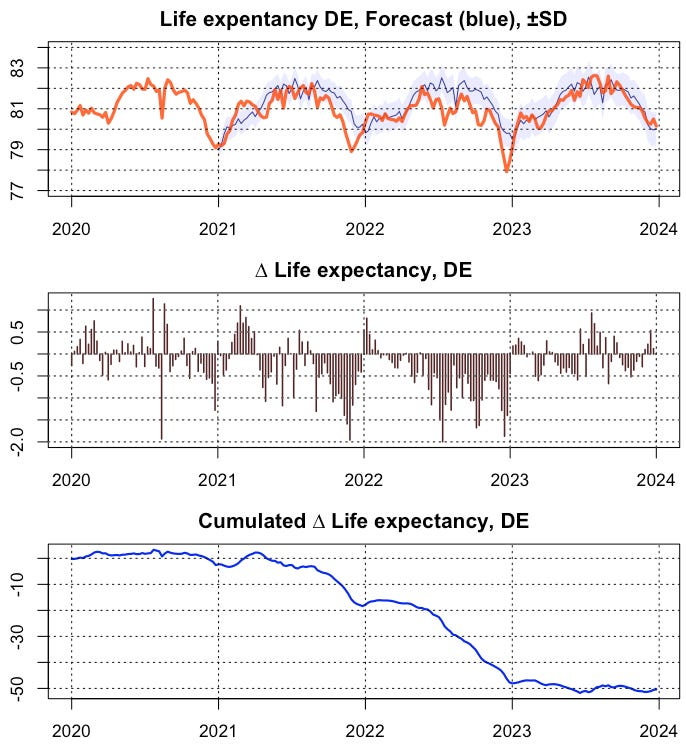

Destatis yesterday published deaths figures for the whole of 2023. In order to obtain a reliable assessment of the situation, I calculated the weekly time series of life expectancy, applied an ARIMA forecast from the reference epoch 2016-2020 and compared it with the actual values. In this way, results are now available for all 4 pandemic years to date (Fig. 1)

Many countries, including the UK, have continued to experience an apparent excess of deaths long after the peaks associated with the COVID-19 pandemic in 2020 and 2021. Numbers of excess deaths estimated in this period are considerable. The UK Office for National Statistics (ONS) has calculated that there were 7.2% or 44,255 more deaths registered in the UK in 2022 based on comparison with the five-year average (excluding 2020). This persisted into 2023 with 8.6% or 28,024 more deaths registered in the first six months of the year than expected. The Continuous Mortality Investigation (CMI) found a similar excess (28,500 deaths) for the same period using different methods. Several methods can be used to estimate excess deaths, each with limitations which should be considered in interpretation, however the overall trends tend to be consistent across the various methods.

The causes of these excess deaths are likely to be multiple and could include the direct effects of Covid-19 infection, acute pressures on NHS acute services resulting in poorer outcomes from episodes of acute illness, and disruption to chronic disease detection and management. Further analysis by cause and by age- and sex-group may help quantify the relative contributions of these causes.

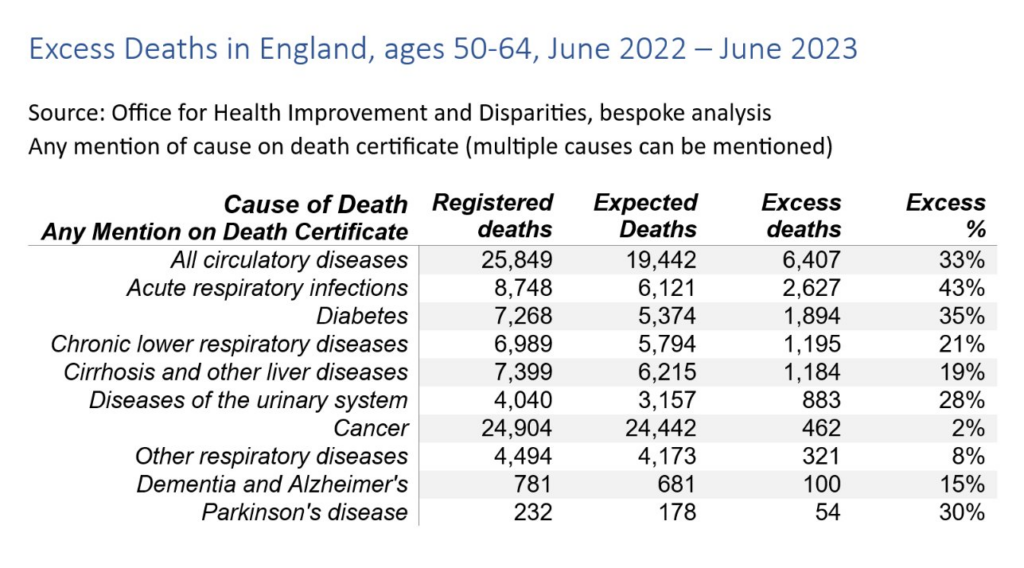

Since July 2020, the Office for Health Improvement and Disparities (OHID) has published estimates of excess mortality based on a Poisson regression model for England week by week, overall and decomposed by age, ethnicity, region and cause. This model finds that in the period from week ending 3rd June 2022 to 30th June 2023, excess deaths for all causes were relatively greatest for 50–64 year olds (15% higher than expected), compared with 11% higher for 25–49 and < 25 year olds, and about 9% higher for over 65 year old groups. While the median age of these groups has changed since 2020, age-standardised mortality analysis breaking down death rates by sex find clearer age differences still. The age-standardised CMI found similar patterns with the largest relative excess deaths for 2022 observed in young (20–44 years) and middle-aged (45–64 years) adults. These findings should be interpreted carefully because of greater than usual delay in registration of deaths in the latter part of 2022.

Several causes, including cardiovascular diseases, show a relative excess greater than that seen in deaths from all-causes (9%) over the same period (week ending 3rd June 2022–30th June 2023), namely: all cardiovascular diseases (12%), heart failure (20%), ischaemic heart diseases (15%), liver diseases (19%), acute respiratory infections (14%), and diabetes (13%).

For middle-aged adults (50–64) in this 13-month period, the relative excess for almost all causes of death examined was higher than that seen for all ages. Deaths involving cardiovascular diseases were 33% higher than expected, while for specific cardiovascular diseases, deaths involving ischaemic heart diseases were 44% higher, cerebrovascular diseases 40% higher and heart failure 39% higher. Deaths involving acute respiratory infections were 43% higher than expected and for diabetes, deaths were 35% higher. Deaths involving liver diseases were 19% higher than expected for those aged 50–64, the same as for deaths at all ages.

Looking at place of death, from 3rd June 2022 to 30th June 2023 there were 22% more deaths in private homes than expected compared with 10% more in hospitals, but there was no excess in deaths in care homes and 12% fewer deaths than expected in hospices. For deaths involving cardiovascular diseases the relative excess in private homes was higher than all causes at 27%. Deaths in hospital were 8% higher and deaths in care homes only 3% higher.

The greatest numbers of excess deaths in the acute phase of the pandemic were in older adults. The pattern now is one of persisting excess deaths which are most prominent in relative terms in middle-aged and younger adults, with deaths from CVD causes and deaths in private homes being most affected. Timely and granular analyses are needed to describe such trends and so to inform prevention and disease management efforts. Leveraging such granular insights has the potential to mitigate what seems to be a continued and unequal impact on mortality, and likely corresponding impacts on morbidity, across the population.

Author(s): Jonathan Pearson-Stuttard Sarah Caul Stuart McDonald Emily Whamond John N. Newton

Publication Date: 1 Dec 2023

Publication Site: The Lancet Regional Health Europe

Question Was political party affiliation a risk factor associated with excess mortality during the COVID-19 pandemic in Florida and Ohio?

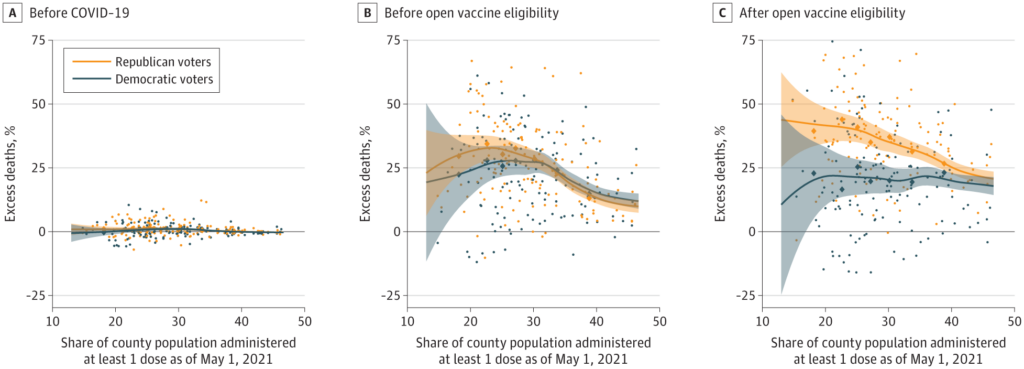

Findings In this cohort study evaluating 538 159 deaths in individuals aged 25 years and older in Florida and Ohio between March 2020 and December 2021, excess mortality was significantly higher for Republican voters than Democratic voters after COVID-19 vaccines were available to all adults, but not before. These differences were concentrated in counties with lower vaccination rates, and primarily noted in voters residing in Ohio.

Meaning The differences in excess mortality by political party affiliation after COVID-19 vaccines were available to all adults suggest that differences in vaccination attitudes and reported uptake between Republican and Democratic voters may have been a factor in the severity and trajectory of the pandemic in the US.

Abstract

Importance There is evidence that Republican-leaning counties have had higher COVID-19 death rates than Democratic-leaning counties and similar evidence of an association between political party affiliation and attitudes regarding COVID-19 vaccination; further data on these rates may be useful.

Objective To assess political party affiliation and mortality rates for individuals during the initial 22 months of the COVID-19 pandemic.

Design, Setting, and Participants A cross-sectional comparison of excess mortality between registered Republican and Democratic voters between March 2020 and December 2021 adjusted for age and state of voter registration was conducted. Voter and mortality data from Florida and Ohio in 2017 linked to mortality records for January 1, 2018, to December 31, 2021, were used in data analysis.

Exposures Political party affiliation.

Main Outcomes and Measures Excess weekly deaths during the COVID-19 pandemic adjusted for age, county, party affiliation, and seasonality.

Results Between January 1, 2018, and December 31, 2021, there were 538 159 individuals in Ohio and Florida who died at age 25 years or older in the study sample. The median age at death was 78 years (IQR, 71-89 years). Overall, the excess death rate for Republican voters was 2.8 percentage points, or 15%, higher than the excess death rate for Democratic voters (95% prediction interval [PI], 1.6-3.7 percentage points). After May 1, 2021, when vaccines were available to all adults, the excess death rate gap between Republican and Democratic voters widened from −0.9 percentage point (95% PI, −2.5 to 0.3 percentage points) to 7.7 percentage points (95% PI, 6.0-9.3 percentage points) in the adjusted analysis; the excess death rate among Republican voters was 43% higher than the excess death rate among Democratic voters. The gap in excess death rates between Republican and Democratic voters was larger in counties with lower vaccination rates and was primarily noted in voters residing in Ohio.

Conclusions and Relevance In this cross-sectional study, an association was observed between political party affiliation and excess deaths in Ohio and Florida after COVID-19 vaccines were available to all adults. These findings suggest that differences in vaccination attitudes and reported uptake between Republican and Democratic voters may have been factors in the severity and trajectory of the pandemic in the US.

Author(s): Jacob Wallace, PhD1; Paul Goldsmith-Pinkham, PhD2; Jason L. Schwartz, PhD1

Researchers in Japan have found a significant increase in the number of suicides among women and girls between the ages of 10 and 24 during the pandemic, while there was no significant change in the suicide rate for boys and men in the same age group.

The research team analyzed data on suicides by gender across three age groups — 10 to 14, 15 to 19 and 20 to 24 — comparing the number of suicides after July 2020 with the number of suicides before the pandemic began.

According to the health ministry, the number of suicides among women and girls age between 10 and 24 in 2022 was 745, an increase of 233 compared with the 2019 figure. The data also showed that the number of boys and men in that age range who committed suicide was 1,278, an increase of 100 cases from 2019.

The research was led by Nobuyuki Horita from Yokohama City University Hospital and Sho Moriguchi from the Department of Neuroscience at Keio University using data on deaths by suicide from July 2012 to June 2022 provided by the health ministry.

…..

Over the past 10 years, a total of 13,263 young people age 10 to 24 — 9,428 male and 3,835 female — died by suicide.

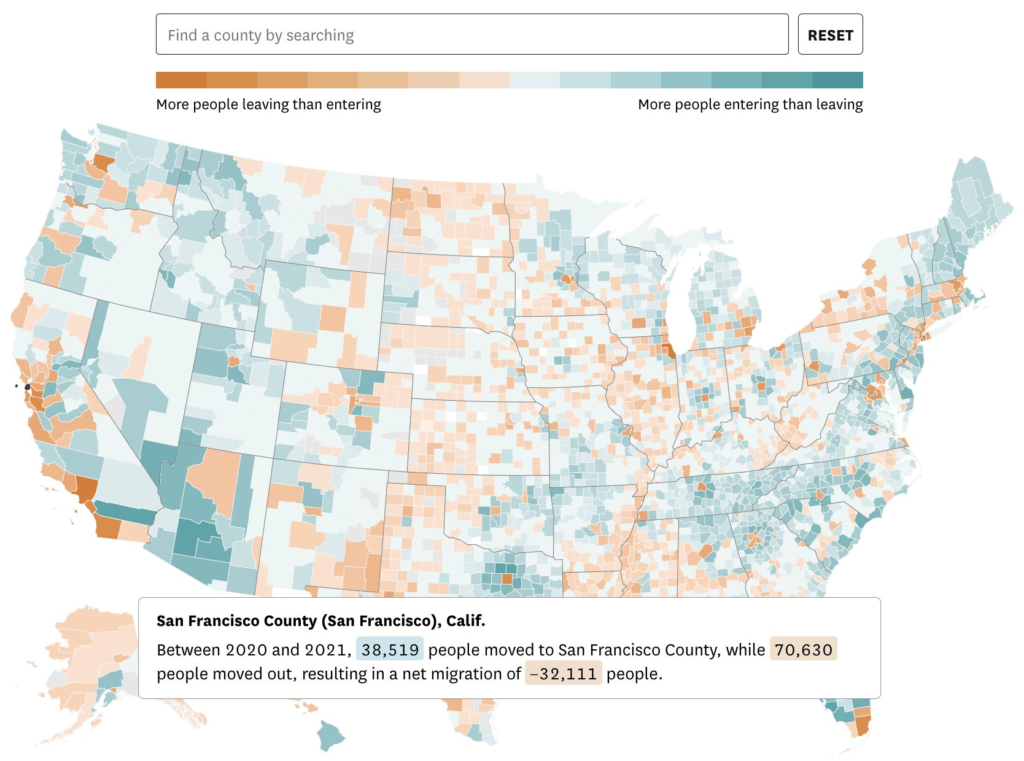

Where did people move to during the pandemic? It's a common question that's been explored using various sources, but the most accurate & detailed data recently came out from the IRS

Question How many excess deaths and years of potential life lost for the Black population, compared with the White population, occurred in the United States from 1999 through 2020?

Findings Based on Centers for Disease Control and Prevention data, excess deaths and years of potential life lost persisted throughout the period, with initial progress followed by stagnation of improvement and substantial worsening in 2020. The Black population had 1.63 million excess deaths, representing more than 80 million years of potential life lost over the study period.

Meaning After initial progress, excess mortality and years of potential life lost among the US Black population stagnated and then worsened, indicating a need for new approaches.

Author(s): César Caraballo, MD1,2; Daisy S. Massey, BA3; Chima D. Ndumele, PhD4; et al