Graphic:

Publication Date: 12 May 2023

Publication Site: Treasury Department

All about risk

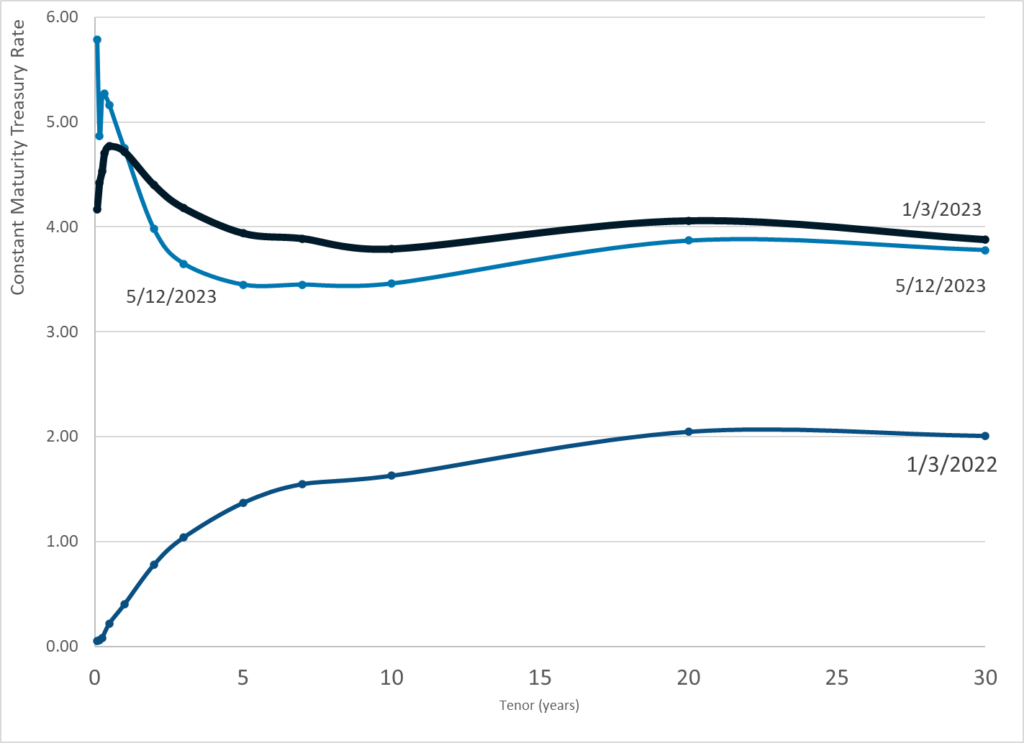

Graphic:

Publication Date: 12 May 2023

Publication Site: Treasury Department

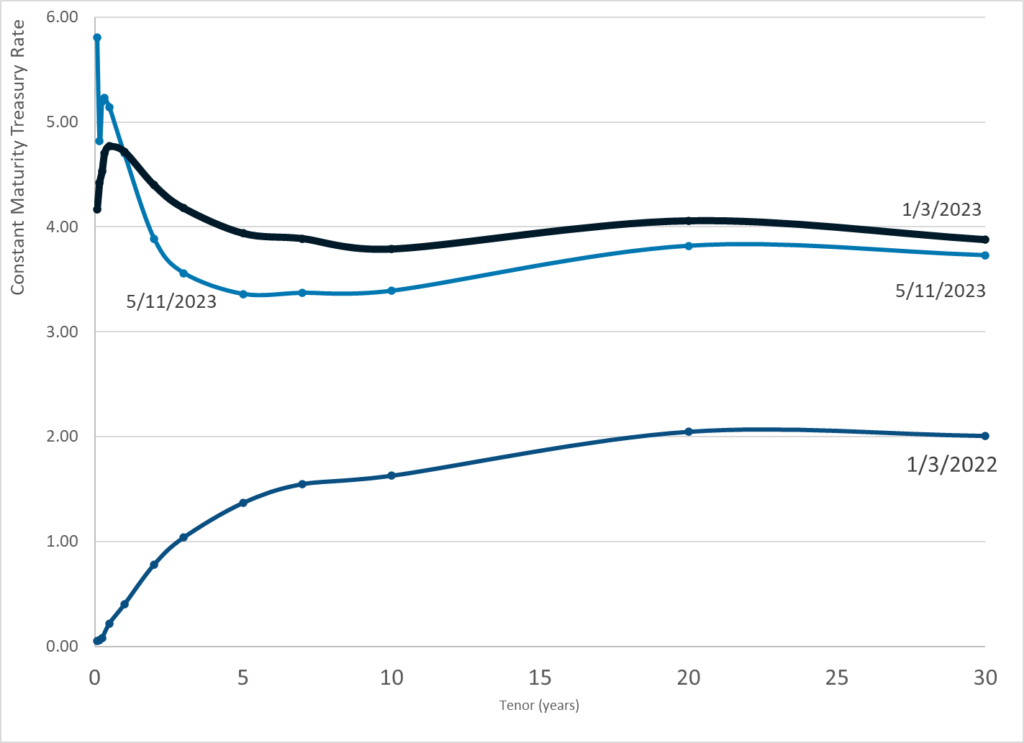

Graphic:

Publication Date: 11 May 2023

Publication Site: Treasury Department

Graphic:

Excerpt:

The five biggest auto insurers in Illinois have raised automobile insurance rates a whopping $527 million since January, an analysis by two consumer groups shows.

That follows about $1.1 billion in rate increases last year by the top 10 Illinois car insurers.

The analysis by the nonprofit Illinois Public Interest Research Group and Consumer Federation of America looked at auto insurance rate increases by the five largest companies in Illinois: State Farm, Allstate, Progressive, Geico and Country Financial, which together make up 62% of the Illinois market.

…..

Now, state Rep. Will Guzzardi, D-Chicago, has introduced legislation to address those issues and crack down on insurers. Guzzardi’s bill would:

It’s already illegal to use race, ethnicity and religion in setting rates. That would continue under Guzzardi’s proposal.

Author(s): Stephanie Zimmermann | Chicago Sun-Times

Publication Date: 6 May 2023

Publication Site: WBEZ in Chicago

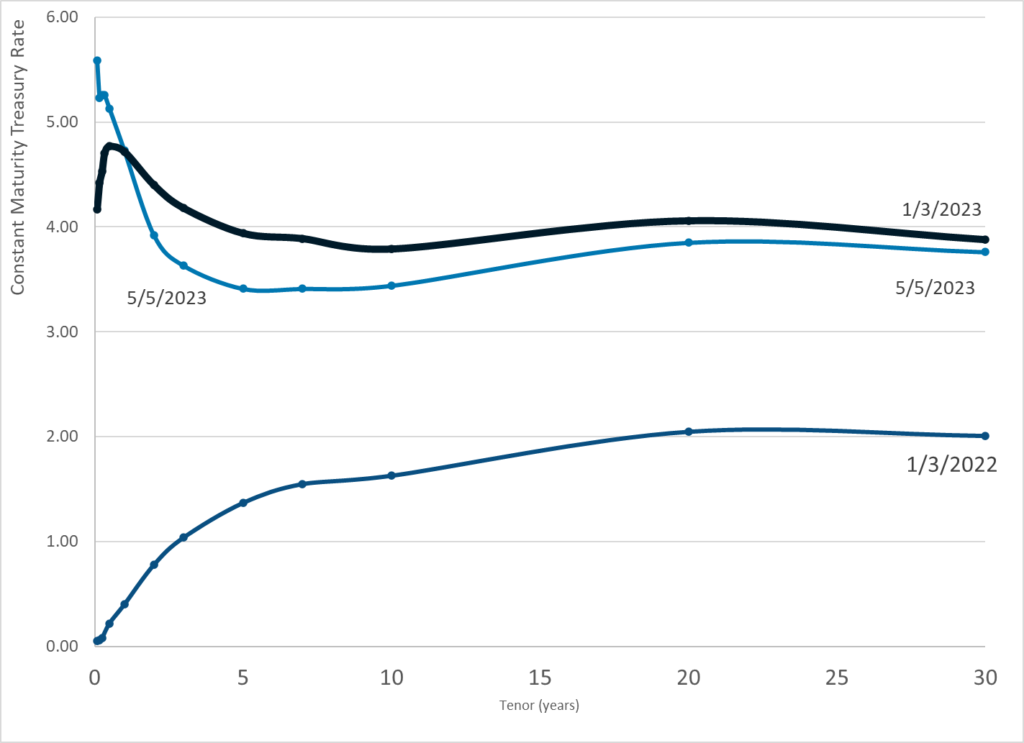

Graphic:

Publication Date: 9 May 2023

Publication Site: Treasury Dept

Link: https://mishtalk.com/economics/hello-president-biden-the-ball-is-in-your-court

Graphic:

Excerpt:

Key Provisions

Hello Joe, the Ball is in Your Court

Republicans only had 4 votes to spare but with some last minute haggling, the bill passed 217-215.

It wasn’t a pretty serve by McCarthy, but the ball cleared the net and landed in play.

The only way to get the ball back in the Republican court would be for the Senate to pass a measure or amend the House bill.

Author(s): Mike Shedlock

Publication Date: 8 May 2023

Publication Site: Mish Talk

Link: https://alec.org/article/calpers-and-calstrs-know-fossil-fuel-divestment-is-a-recipe-for-disaster/

Excerpt:

In the Golden State, the California State Teachers’ Retirement System (CalSTRS) and the California Public Employees’ Retirement System (CalPERS) are waking up to the fact that divestment hurts retirees and taxpayers.

CalPERS and CalSTRS are two of the largest pension funds in the country (by both membership and portfolio size). As California Senate Bill 252, a bill calling for fossil fuel divestment from public retirement systems in California, continues to move along in committee, CalPERS and CalSTRS have publicly opposed the bill because it conflicts with their duties as pension plan managers.

As ALEC VP of Policy Lee Schalk and I mentioned in our OC Register column last month, politicized investment strategies are a recipe for disaster. Research from Mike Edleson and Andy Puzder found that ESG investing yields lower returns than investing without political constraints. Additionally, researchers at Boston College found that ESG has failed to achieve its stated social goals.

Both CalPERS and CalSTRS realize that divestment hampers their ability to put members’ retirements benefits first, and the research shows divestment does not achieve its stated social goals.

Author(s): Thomas Savidge

Publication Date: 28 April 2023

Publication Site: ALEC

Graphic:

Publication Date: 5 May 2023

Publication Site: Treasury Department

Link: https://rajivsethi.substack.com/p/the-new-mortgage-fee-structure

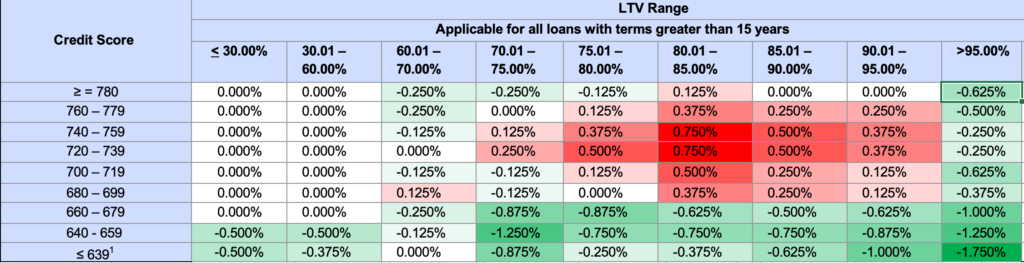

Graphic:

Excerpt:

Notice that credit scores below 639 have been consolidated into a single row, and those above 740 have been split into three. In addition, loan-to-value ratios at 60% and below are now in two separate columns rather than one. This makes direct visual comparisons a little difficult, but one thing is clear—at no level of the loan-to-value ratio does someone with a lower credit score pay less than someone with a higher score. That is, one cannot gain by sabotaging one’s own credit rating.

In general, there are two types of borrowers who stand to gain under the new fee structure: those with low credit scores, and those with low down payments. In fact, those at the top of the credit score distribution gain under the new structure if they have down payments less than 5% of the value of the home. The following table shows gains and losses relative to the old structure, with reduced fees in green and elevated ones in red (a comparable color-coded chart with somewhat different cells may be found here):

What might the rationale be for rewarding those making especially low down payments? Perhaps the goal is to make housing more affordable for people without substantial accumulated savings or inherited wealth. But there will be an unintended consequence as those with reasonably high credit scores and substantial wealth choose to lower their down payments strategically in order to benefit from lower fees. They may do so by simply borrowing more for any given property, or buying more expensive properties relative to their accumulated savings. The incentive to do so will be strongest for those hit hardest by the changes, with credit scores in the 720-760 range and down payments between 15% and 20%.

Author(s): Rajiv Sethi

Publication Date: 23 Apr 2023

Publication Site: Imperfect Information at Substack

Link: https://angrybearblog.com/2023/04/income-tax-withholding-payments-stumble-again

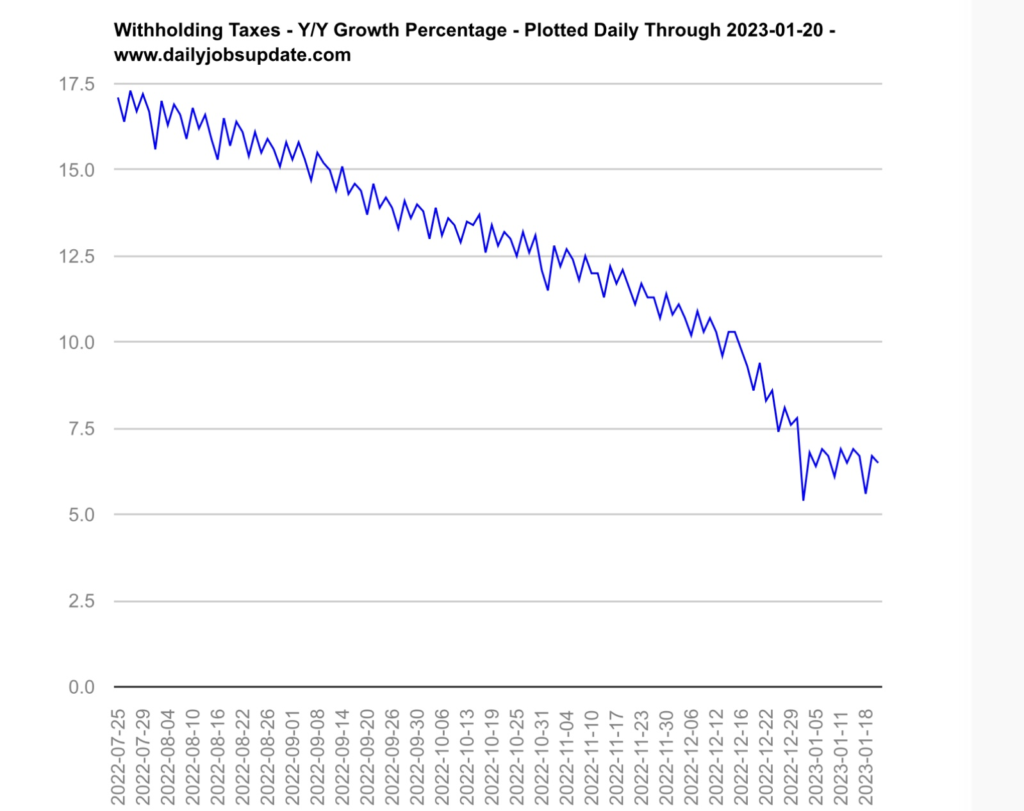

Graphic:

Excerpt:

The important data this week will include new home sales tomorrow, Q1 GDP and initial jobless claims on Thursday, and most importantly of all (imo) real personal income and spending, along with real manufacturing and trade sales on Friday.

In the meantime, today let me take another look at a significant coincident indicator, income tax withholding payments, because the situation has changed in the past week.

….

For the nation as a whole Matt Trivisonno has the YoY data, measuring the entire 365 day total of tax withholding vs. the entire previous 365 days, and has a public graph with a 3 month delay. Here’s his latest:

Like the California graph, it shows a steep deceleration during 2022, which had been as high as +21% YoY in March, down to only about +6% by the end of December. Thereafter through January, the YoY data stabilizes.

Indeed, by my own calculations, for the first three months of fiscal 2023 ending December 31, withholding tax payments were only up +1.2% YoY. But for Q2 they rebounded sharply, up +5.4% YoY.

But in the last 10 days they have stumbled. For the first 14 withholding days in April, payments are down -3.4%, $189.7 Billion vs. $196.3 Billion one year ago. For the last 4 weeks as a whole, withholding payments are down -5.0%, $270.2 Billion vs. $284.5 Billion.

Author(s): New Deal democrat

Publication Date: 25 April 2023

Publication Site: Angry Bear

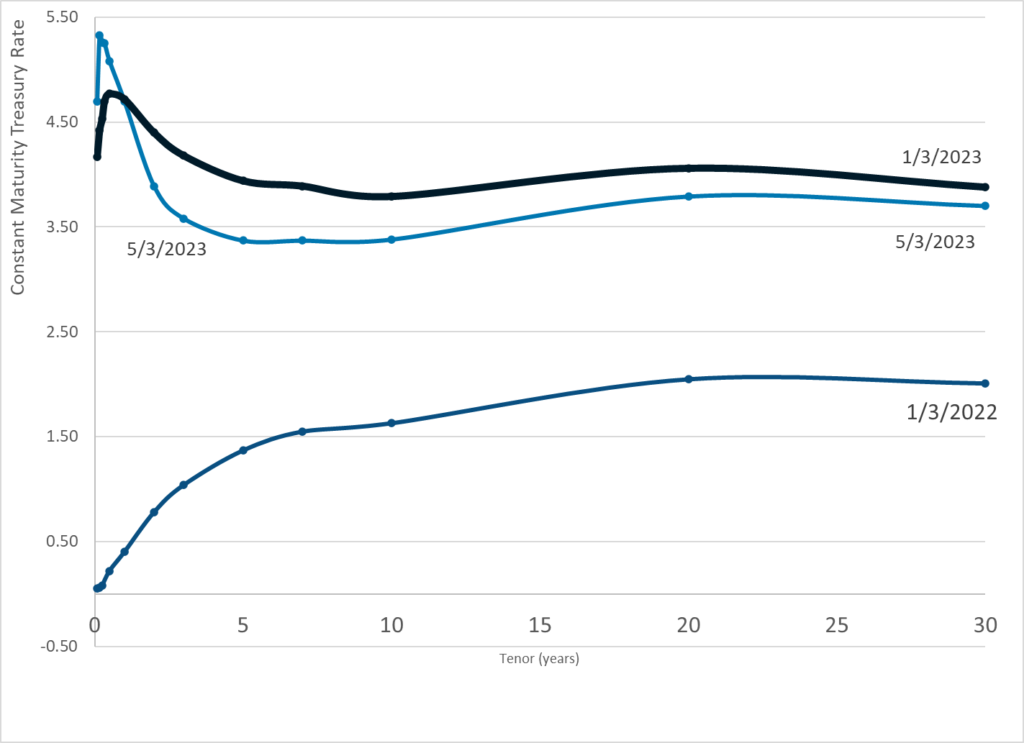

Graphic:

:

Publication Date: 3 May 2023

Publication Site: Treasury Dept

Graphic:

Excerpt:

Please use the sharing tools found via the share button at the top or side of articles. Copying articles to share with others is a breach of FT.comT&Cs and Copyright Policy. Email licensing@ft.com to buy additional rights. Subscribers may share up to 10 or 20 articles per month using the gift article service. More information can be found here.

https://www.ft.com/content/ad3a97fc-6394-471b-95b6-a46576808f4a?accessToken=zwAF-p9xpktIkdOtOpf8Y5RHG9OVtqRldoCPSg.MEUCIDgGL7wEhhf0DcMprg_1VYV0TDGsyWYpn56E-cBhCGWoAiEA_YjdblG4oKzNoagG66jcPOhEtvtht7Du5gnihbZVDfU&sharetype=gift&token=82960010-bfb1-44e4-a677-de6e47ba5545

Any predictions are by their nature uncertain, yet a longevity modelling firm has forecasted that both candidates are likely to live well beyond the end of the next presidency in 2029. According to Club Vita, actuarial data suggests both men could have more than another decade ahead of them.

The company, which offers analytical services to insurers, said its US model suggested Biden has a life expectancy of another 11 years, taking him to 91. Trump has 14 more years to look forward to, per the model, meaning he would die at 90.

The model’s inputs include affluence, marital status, and employment. These key demographics for both Biden and Trump put them in the same favourable categories for the main factors, including addresses in the top category for life expectancy: the analysts used Trump’s Palm Beach address and Biden’s Delaware home.

Erik Pickett, a New Jersey-based actuary for Club Vita, said a wide range of factors could prove its model wrong, from whether the candidates “are in significantly different health to the average of someone with the same characteristics” to the fact that presidents have “access to higher quality medical treatments” than the typical American.

Author(s): Ian Smith in London and David Crow in New York

Publication Date: 30 April 2023

Publication Site: FT.com

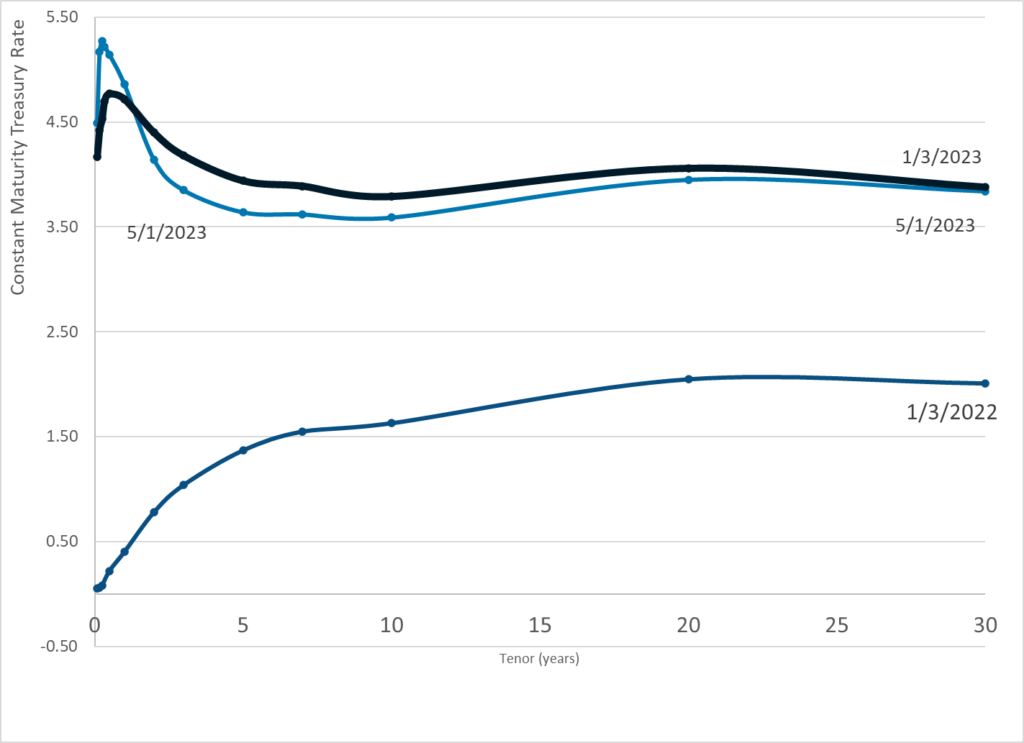

Graphic:

Publication Date: 1 May 2023

Publication Site: Treasury Department