Malaria could stop an army in its tracks. In 413 BC, at the height of the disastrous Sicilian Expedition, malaria sucked the life out of the Athenian army as it lay siege to Syracuse. Athens never recovered from its losses and fell to the Spartans in 404 BC.

But while malaria helped to destroy the Athenians, it provided the Roman Republic with a natural barrier against invaders. The infested Pontine Marshes south of Rome enabled successive generations of Romans to conquer North Africa, the Middle East and Europe with some assurance they wouldn’t lose their own homeland. Thus, the spread of classical civilization was carried on the wings of the mosquito. In the 5th century, though, the blessing became a curse as the disease robbed the Roman Empire of its manpower.

Throughout the medieval era, malaria checked the territorial ambitions of kings and emperors. The greatest beneficiary was Africa, where endemic malaria was deadly to would-be colonizers. The conquistadors suffered no such handicap in the New World.

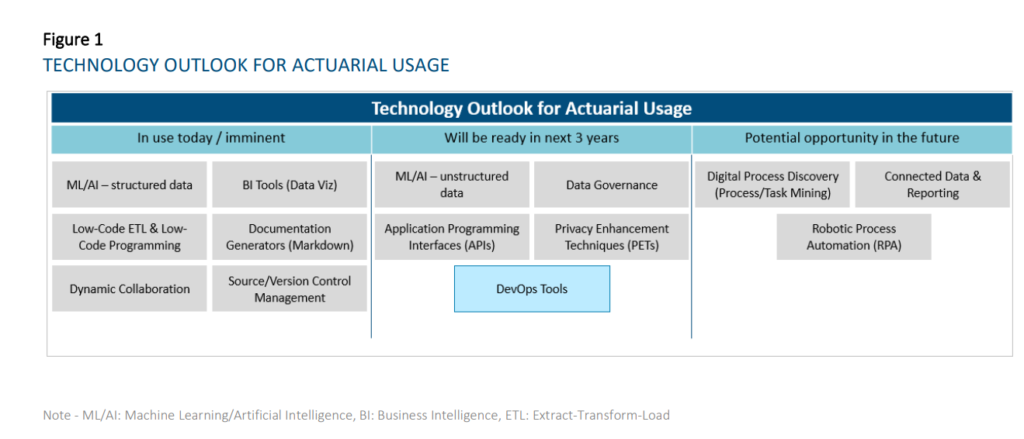

Technologies that have reached widespread adoption today: o Dynamic Collaboration Tools – e.g., Microsoft Teams, Slack, Miro – Most companies are now using this type of technology. Some are using the different functionalities (e.g., digital whiteboarding, project management tools, etc.) more fully than others at this time. • Technologies that are reaching early majority adoption today: o Business Intelligence Tools (Data Visualization component) – e.g., Tableau, Power BI — Most respondents have started their journey in using these tools, with many having implemented solutions. While a few respondents are lagging in its adoption, some companies have scaled applications of this technology to all actuaries. BI tools will change and accelerate the way actuaries diagnose results, understand results, and communicate insights to stakeholders. o ML/AI on structured data – e.g., R, Python – Most respondents have started their journey in using these techniques, but the level of maturity varies widely. The average maturity is beyond the piloting phase amongst our respondents. These are used for a wide range of applications in actuarial functions, including pricing business, modeling demand, performing experience studies, predicting lapses to support sales and marketing, producing individual claims reserves in P&C, supporting accelerated underwriting and portfolio scoring on inforce blocks. o Documentation Generators (Markdown) – e.g., R Markdown, Sphinx – Many respondents have started using these tools, but maturity level varies widely. The average maturity for those who have started amongst our respondents is beyond the piloting phase. As the use of R/Python becomes more prolific amongst actuaries, the ability to simultaneously generate documentation and reports for developed applications and processes will increase in importance. o Low-Code ETL and Low-Code Programming — e.g., Alteryx, Azure Data Factory – Amongst respondents who provided responses, most have started their journey in using these tools, but the level of maturity varies widely. The average maturity is beyond the piloting phase with our respondents. Low-code ETL tools will be useful where traditional ETL tools requiring IT support are not sufficient for business needs (e.g., too difficult to learn quickly for users or reviewers, ad-hoc processes) or where IT is not able to provision views of data quickly enough. o Source Control Management – e.g., Git, SVN – A sizeable proportion of the respondents are currently using these technologies. Amongst these respondents, solutions have already been implemented. These technologies will become more important in the context of maintaining code quality for programming-based models and tools such as those developed in R/Python. The value of the technology will be further enhanced with the adoption of DevOps practices and tools, which blur the lines between Development and Operations teams to accelerate the deployment of applications/programs

Author(s):

Nicole Cervi, Deloitte Arthur da Silva, FSA, ACIA, Deloitte Paul Downes, FIA, FCIA, Deloitte Marwah Khalid, Deloitte Chenyi Liu, Deloitte Prakash Rajgopal, Deloitte Jean-Yves Rioux, FSA, CERA, FCIA, Deloitte Thomas Smith, Deloitte Yvonne Zhang, FSA, FCIA, Deloitte

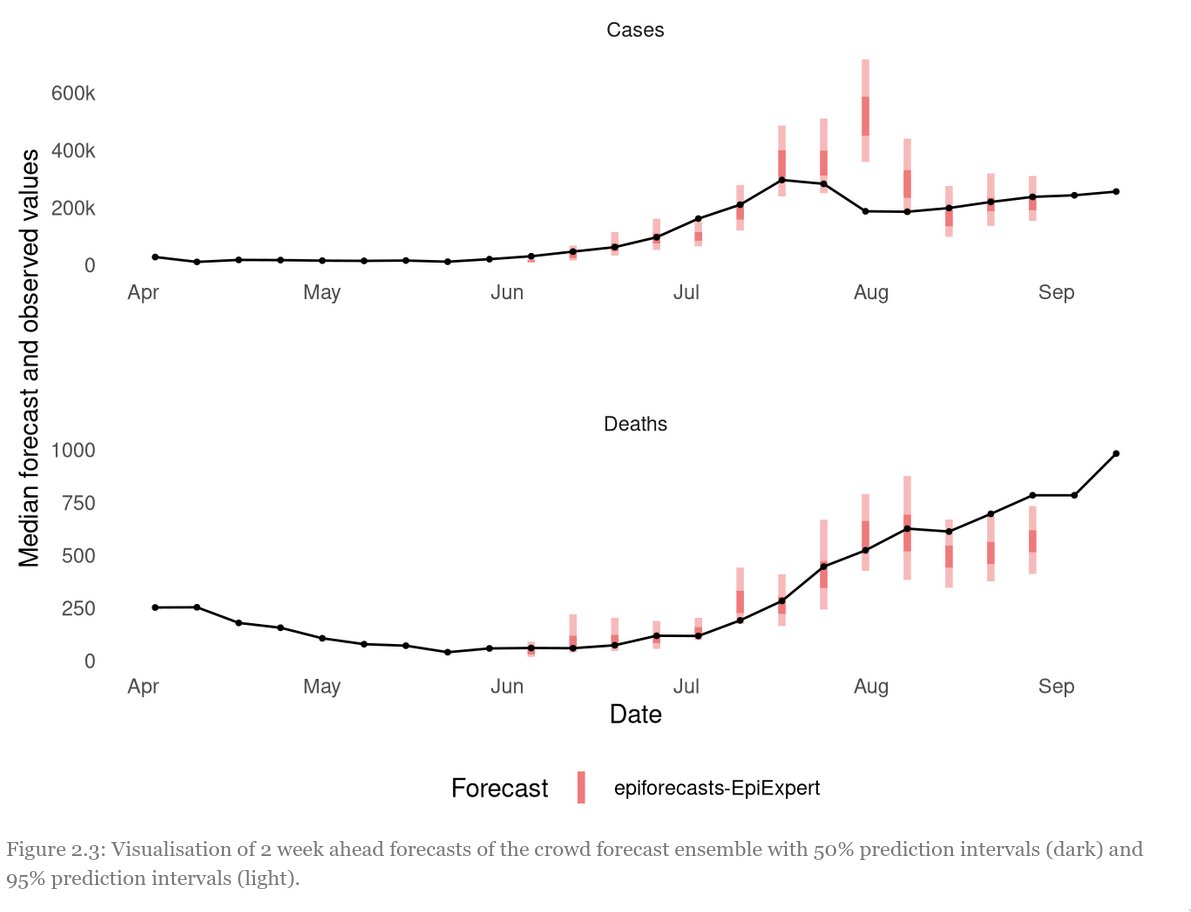

Let’s start with the data. The UK Forecasting Challenge spanned a long period of exponential growth as well as a sudden drop in cases at the end of July 3

Especially this peak was hard to predict and no forecaster really saw it coming. Red: aggregated forecast from different weeks, grey: individual participants. The second picture shows the range for which participants were 50% and 95% confident they would cover the true value

….

So what have we learned? – Human forecasts can be valuable to inform public health policy and can sometimes even beat computer models – Ensembles almost always perform better than individuals – Non-experts can be just as good as experts – recruiting participants is hard

Author(s): Nikos Bosse

Publication Date: Accessed 17 Oct 2021, twitter thread 15 Oct 21

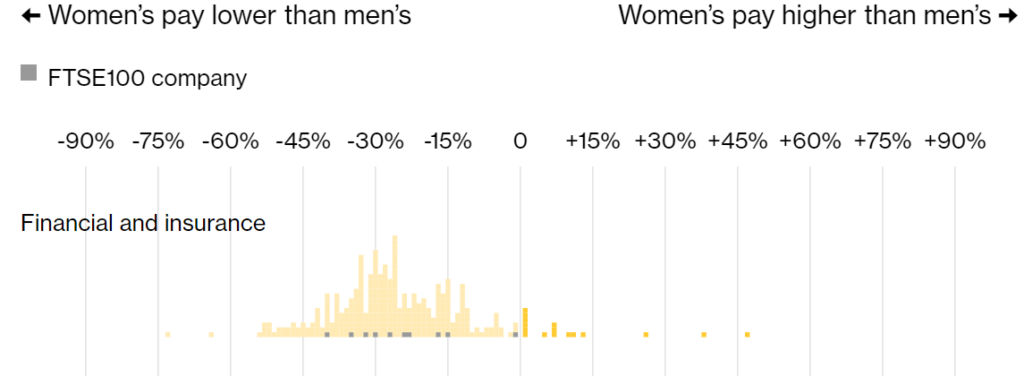

Women in finance in the U.K. still make significantly less than men. While the gender pay gap at financial firms in the country narrowed slightly last year, overall the industry continues to have the biggest disparity.

Men working in finance and insurance made 25% more than women last year, down from 28% in 2019, a Bloomberg News analysis of government data shows. The pay gap is especially wide in investment banking, where some of the highest-paid employees work.

It is the fourth straight year that finance has led the industry rankings, showing that executives are finding it difficult to shrink the gap. Mining and quarrying had the second-biggest pay gap at 23% as the commodity boom boosted the income of workers, who are largely male.

Allstate Corp. plans to sell its headquarters building, marking the U.S. finance industry’s firmest endorsement yet of the desire to offer hybrid work after the pandemic.

With many employees choosing to work remotely, the insurance giant will sell its offices in Northbrook, Illinois, according to an emailed statement Friday. The complex in a Chicago suburb has several buildings that total 1.9 million square feet on a 186-acre (75 hectares), Allstate has said in regulatory filings.

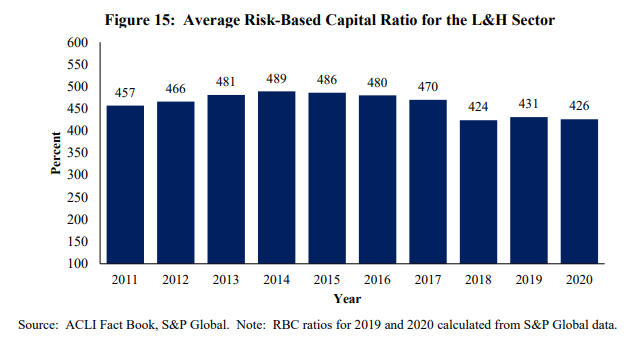

Figure 15 shows that the average risk-based capital ratio for the L&H sector declined slightly in

Specifically, statutory capital and surplus was 4.26 times the level of minimum required regulatory capital on average in 2020 compared to 4.31 times the required level in 2019.

L&H sector net income of $22 billion in 2020 was less than one-half of 2019 levels, affecting the potential for capital generation. The sector reported a nearly 10 percent increase in death and annuity benefit expenses, which contributed to a ratio of total benefit expenses to premiums earned of 50 percent in 2020, rising substantially from 44.4 percent in 2019. According to Fitch Ratings, life insurer operating results in 2020 were largely impacted by higher claims paid, primarily due to increased mortality from COVID-19.24

Certain leverage ratios indicate that L&H insurers faced balance sheet pressures in 2020. The greater financial flexibility afforded by steady leverage ratios has enabled insurers to consistently fulfill policyholder obligations by: (1) returning a profit by investing the premiums received from underwriting activities; and (2) limiting the risk exposure from the policies underwritten. Insurers also employ reinsurance in order to move some of the risks off their own balance sheets and on to those of reinsurers. Figure 16 provides a view of the L&H sector’s general account leverage for the last 10 years.

The next section is another gratuitous dunk on Confucius, but it’s also a warning about the perils of seeing strict linear relationships where there are none. Not only will you continually be disappointed/frustrated, you won’t know why.

In this story, Laozi suggests that Confucius’ model of a world in which every additional unit of virtue accumulated will receive its corresponding unit of social recognition is clearly not applicable to the age in which they lived.

Moreover, this results in a temptation is to blame others for not living up to your model. Thus, in the years following the 2007 crash, Lehman brothers were apostrophised for their greed, but in reality all they had done was respond as best they could to the incentives that society gave them. If we wanted them to behave less irresponsibly, we should have pushed government to adjust their incentives. They did precisely what we paid them to. If we didn’t want this outcome, we should have anticipated it and paid for something else.

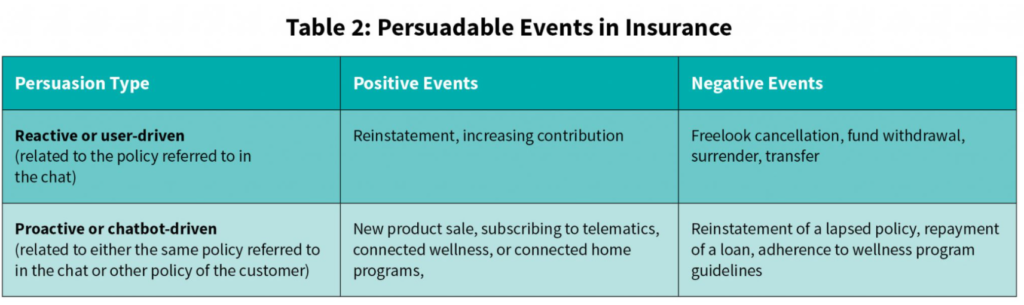

Individuals have a different kind of relationship with insurance than what they have with any other product or service. Though being the most effective risk mitigation tool, it still requires a hard push from insurers and regulators to make people purchase. The thought of insurance could evoke every other emotion except joy in an individual. The main reason for this is that insurance is a futuristic promise that assures compensation when a covered risk event happens. This operates exactly opposite to the strong impulse of scarcity and immediacy bias.

As in any other industry, the persuadable events in insurance could be based on reactive or proactive triggers to encourage positive or discourage negative events. Depending on the intelligence ingrained in the back-end systems and the extent customer data is consolidated, the proactive persuasion events could be personalized to a customer and not just limited to generalized promotion of a new product or program. It could be performed for other persuadable events of the same policy for which the chat is in progress or expand to include policy events from other policies of the customer.

An indicative list of the persuadable events in an insurance policy could be categorized as given in Table 2.

My advice for actuaries looking to succeed outside the traditional function:

Push yourself to speak up more. Actuarial leaders know how to get the best out of you. It may not be the same experience with leaders in different areas of the business. So take advantage and speak up.

Have an opinion. So often I’ve worked with young actuaries who can perform incredible analysis but will stop short of providing an opinion and often defer to their manager or a senior actuary. As you move up the corporate ladder, you’re going to have to get more comfortable with providing your input with less and less data to work with.

If you are still toying with the idea of moving outside of a traditional actuarial role, it never hurts to widen your circle. Get to know the people in different areas of your company. Sit with an underwriter while they process a policy, shadow a claims adjuster while they work to help a customer during a stressful time of their life or connect with a member of your broker distribution team to find out what brokers or customers are saying. It will give you a whole new perspective on where the data you work with comes from.

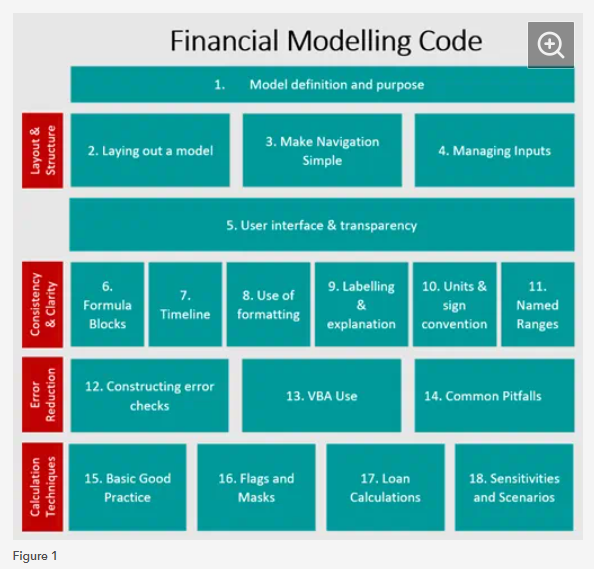

There has been significant disruption in how organisations conduct business and the way we work over the past year and a half. However, financial modellers and developers have had to continue to build, refine and test their models throughout these unprecedented times. Figure 1 below summarises the areas we have covered in the blog series and how they fit together to form the practical guidance of how to follow and implement the Financial Modelling Code.

Looking at other great tools like R and Python, it can be difficult to summarize a single reason to motivate a switch to Julia, but hopefully this article piqued an interest to try it for your next project.

That said, Julia shouldn’t be the only tool in your tool-kit. SQL will remain an important way to interact with databases. R and Python aren’t going anywhere in the short term and will always offer a different perspective on things!

In an earlier article, I talked about becoming a 10x Actuary which meant being proficient in the language of computers so that you could build and implement great things. In a large way, the choice of tools and paradigms shape your focus. Productivity is one aspect, expressiveness is another, speed one more. There are many reasons to think about what tools you use and trying out different ones is probably the best way to find what works best for you.

It is said that you cannot fully conceptualize something unless your language has a word for it. Similar to spoken language, you may find that breaking out of spreadsheet coordinates (and even a dataframe-centric view of the world) reveals different questions to ask and enables innovated ways to solve problems. In this way, you reward your intellect while building more meaningful and relevant models and analysis.