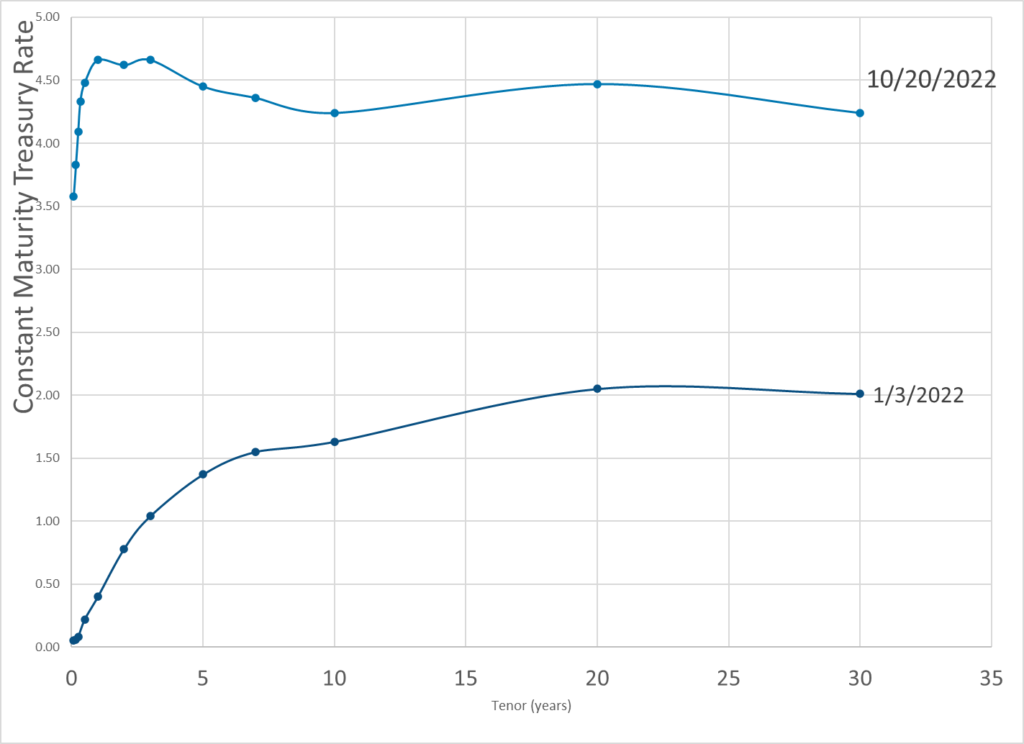

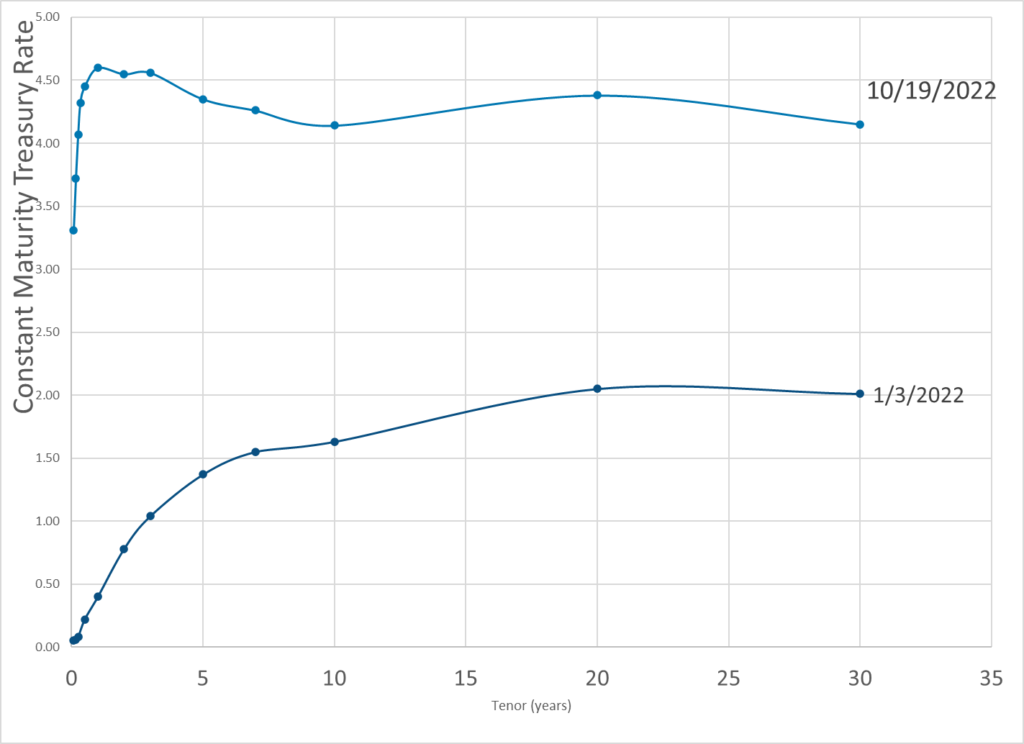

Debate now rages about whether the Federal Reserve should continue to raise interest rates to tame inflation or slow down these hikes and see what happens. This is not the first debate we’ve had recently about inflation and Fed actions. The lesson we should learn, and I fear we won’t, is that government officials and those advising them from inside or outside the government don’t know as much as they claim to about the interventions they design to control the economy.

As a reminder, in 2021, the dominant voices including Fed Chairman Jerome Powell asserted that the emerging inflation would be “transitory” and disappear when pandemic-induced supply constraints dissolve. That was wrong. When this fact became obvious, the messaging shifted: Fed officials could and would fight inflation in a timely manner by raising rates to the exact level needed to avoid recession and higher unemployment. Never mind that the whole point of raising interest rates is precisely to soak money out of the economy by slowing demand, which often causes unemployment to rise.

…..

Over at Discourse magazine, my colleague Thomas Hoenig—a former president of the Fed’s Kansas City branch—explains how Fed officials faced similar pressures during the late 1960s and 1970s. Unfortunately, he writes, “Bowing to congressional and White House pressure, [Fed officials] held interest rates at an artificially low level….What followed was a persistent period of steadily higher inflation, from 4.5% in 1971 to 14% by 1980. Only then did the [Federal Reserve Open Market Committee], under the leadership of Paul Volcker, fully address inflation.”

Often overlooked is Volcker’s accomplishment: the willingness to stay the course despite a painful recession. Indeed, it took about three years from when he pushed interest rates up to about 20 percent in 1979 for the rate of inflation to fall to a manageable level. As such, Hoenig urges the Fed to stay strong today. He writes, “Interest rates must rise; the economy must slow, and unemployment must increase to regain control of inflation and return it to the Fed’s 2% target.” There is a cost in doing this; a soft landing was never in the cards.

Republicans have seized upon the issues of net-zero and environmental, social and governance investing to call attention to what they claim are negative effects of so-called ‘woke’ orthodoxy on portfolio performance, and harm the U.S. energy industry.

They have also raised the potential for a lapse in fiduciary duty by arguing that allocating towards long-term ESG goals may create short-term underperformance, harming plan beneficiaries.

The attorneys general of 14 states – Arizona, Arkansas, Indiana, Kansas, Kentucky, Louisiana, Mississippi, Missouri, Montana, Nebraska, Oklahoma, Tennessee, Texas, Virginia, and five more that have joined but can’t be named due to state laws or regulations regarding confidentiality –have sent civil investigative demands to the six U.S. banks the investigation targets

The six banks did not respond to requests for comment.

The coalition argues that the banks’ membership in the Net-Zero Banking Alliance is damaging U.S. energy companies. The CIDs, similar to subpoenas, are legally enforceable requests for information related to state or federal investigations.

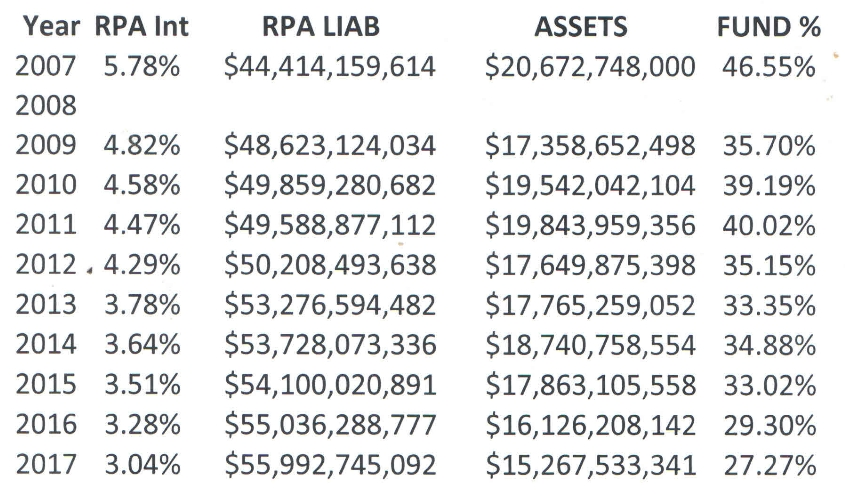

With the 5500 filing season done it is time to tentatively get back to some blogging – starting with the plan that was likely to bring the PBGC (and the entire private pension system) down before the SFA bailout and now will be another cog in the hyperinflation wheelbarrow.

We had some 5500 history in an earlier blog through 2016. This is where the plan was last year based on their 5500 filing for 2021:

Plan Name: Central States, Southeast & Southwest Areas Pension Plan

EIN/PN: 36-6044243/001

Total participants @ 12/31/21: 357,056 including:

Retirees: 189,449

Separated but entitled to benefits: 117,511

Still working: 50,096

Asset Value (Market) @ 1/1/21: 10,409,440,502

Value of liabilities using RPA rate (2.43%) @ 1/1/21: $58,623,837,073 including:

Retirees: $34,084,275,398

Separated but entitled to benefits: $15,801,905,005

A more realistic assumption would be that by investing the good at T=0, it cannot be paid out and consumed at T=1. This is only possible at T=2. With this assumption, the model has two different assets:

– a liquid asset, i.e. the all-purpose asset has not been invested in T=0 and it can be consumed at T=1,

– an illiquid asset, i.e. the all-purpose asset been invested in T=0 and can only be consumed at T=2.

Without banks, risk-averse agents would not be able to participate in the returns of the investment good. As they all are confronted with the risk of being type 1, it would be very risky to invest the commodity. In T=1, Type 1 agents would then not be able to consume.

In such a model, banks can provide an obvious improvement if one assumes again that they know the share of type 1 and type 2 agents. In T=0, all agents deposit their endowment of the commodity with the bank. Assuming that the share of type 1 agents is 25 %, the bank keeps 25 % of the all-purpose asset unchanged and invests 75 % as illiquid long-term investment. It thus performs maturity transformation by transforming liquid assets into illiquid assets (Figure 2).

Author(s): Peter Bofinger and Thomas Haas

Publication Date: 18 Oct 2022

Publication Site: Institute for New Economic Thinking

Starting Monday, consumers will be able to buy hearing aids directly off store shelves and at dramatically lower prices as a 2017 federal law finally takes effect.

Where for decades it cost thousands of dollars to get a device that could be purchased only with a prescription from an audiologist or other hearing professional, now a new category of over-the-counter aids are selling for hundreds of dollars. Walmart says it will sell a hearing aid for as little as $199.

The over-the-counter aids are intended for adults with mild to moderate hearing loss — a market of tens of millions of people, many of whom have until now avoided getting help because devices were so expensive.

Insurance companies that have long said they’ll cover anything, at the right price, are increasingly ruling out fossil fuel projects because of climate change – to cheers from environmental campaigners.

More than a dozen groups that track what policies insurers have on high-emissions activities say the industry is turning its back on oil, gas and coal.

The alliance, Insure Our Future, said Wednesday that 62% of reinsurance companies – which help other insurers spread their risks – have plans to stop covering coal projects, while 38% are now excluding some oil and natural gas projects. (The Insure Our Future report on re/insurers’ fossil fuel activities can be viewed here).

In part, investors are demanding it. But insurers have also begun to make the link between fossil fuel infrastructure, such as mines and pipelines, and the impact that greenhouse gas emissions are having on other parts of their business.