A prolific pension fraud scheme that spread to the insurance industry before being shut down by federal investigators continues to produce fresh lawsuits.

And it also continues to claim new victims — the latest being Shurwest, a successful Scottsdale, Ariz., independent marketing organization. Shurwest filed for Chapter 11 bankruptcy Aug. 31 after executives realized “there’s not going to be anything left,” one of its attorneys said.

According to bankruptcy documents, Shurwest faces 38 pending lawsuits in state and federal courts.

per Brian Graff who has spent 25 years at ASPPA and got some recognition for it at the end of this session.

….

Hispanic and Black coverage in 401(k) plans is low and if this situation it does not improve private sector plans could be eliminated in favor of a government option as in Australia. States (first Oregon, then CA, and 8 others) are setting up their own plans and forcing companies to be in it if they don’t have their own plans. This is good for us in that companies do not want to give their money to states (especially in CA and NJ) so they set up their own plans that need to administered by us.

Proposal that may be effective in 2023 is requiring all companies with at least six employees in the last two years to set up a 401(k) plan with auto-enrollment at 6% going up to 10%. Pie would increase by 62 million participants (from 95 million now) and 600,000 plans (on top of 800,000 now).

The Treasury proposal would have banks report “gross inflows and outflows with a breakdown for physical cash, transactions with a foreign account, and transfers to and from another account with the same owner.” Banks already report interest income over $10 on Form 1099-INT; this proposal would add a few lines to that tax document.

Treasury officials have said that fears of stepped-up audits are unfounded, and the administration has pledged not to increase audits on people earning under $400,000 a year, but focus enforcement “on higher earners who do not fully report their tax liabilities.”

Officials emphasize the IRS would not learn about individual spending patterns — only total money going in or out.

“The proposal involves no reporting of individual transactions of any individual,” Treasury Secretary Janet Yellen told CBS Evening News’ Norah O’Donnell. “If somebody reports an income of $10,000 and they had 3 million [dollars] go out of their checking account, that tells the IRS that’s an individual you might audit.”

Omarova’s most out-there academic ideas include directing the Federal Reserve to handle consumer deposits, taking that power away from banks. “Having Americans park their money at the Fed would allow the central bank to more directly and efficiently pull the levers of monetary policy by enabling it to credit individual citizens’ accounts when there’s a need to stimulate the economy,” notesPolitico.

Rob Nichols, president of the American Bankers Association, has said such policies would “effectively nationalize America’s community banks,” according to The New YorkTimes. Omarova “wants to eliminate the banks she’s being appointed to regulate,” agrees the Wall Street Journal editorial board. Groups representing both big and small banks, including the American Bankers Association, the Consumer Bankers Association, and the Independent Community Bankers of America, have reached out to more moderate Democrats to lodge their opposition to the pick—a ballsy move, given that she may end up passing down the rules that these associations’ members must later comply with.

Wall Street’s three biggest municipal-bond underwriters have seen business grind to a halt in Texas after the state blocked governments from working with banks that have curtailed gun-industry ties. In June, as Goldman Sachs Group Inc. was on the hunt for a new campus in Dallas, Republican Governor Greg Abbott took a shot at ESG initiatives by banning state investments in businesses that cut ties with oil and gas companies.

That’s not to mention the brawls over Covid vaccines and mask mandates, deadly Texas blackouts along the country’s most isolated power grid and new state laws that restrict voting and all but ban abortion. It’s all happening just as Wall Street’s shareholders push the industry to fight climate change, racism and the gender gap.

….

So far, most big banks haven’t taken public positions on the new abortion restrictions. They’re being cautious about requiring Covid-19 vaccinations for employees in places where officials have assailed mandates. But the new Texas gun law is running into both the industry’s efforts to advance social causes and its ability to work with the second-largest state for muni-bond issuance.

JPMorgan Chase & Co. — which has 25,500 Texas employees, its most in any state outside New York — has said it can’t bid on most business with public entities in Texas because of ambiguities around the law. The biggest U.S. bank is assessing its potential next steps, said a person with knowledge of the company’s thinking.

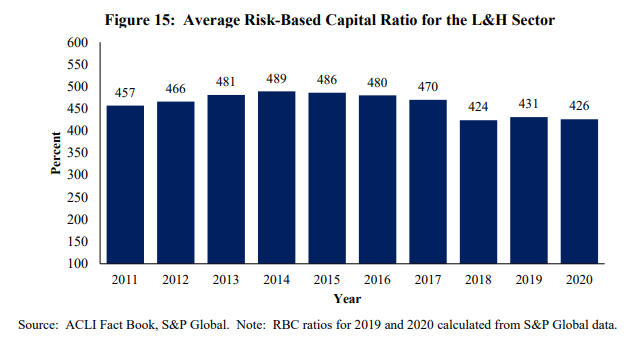

Figure 15 shows that the average risk-based capital ratio for the L&H sector declined slightly in

Specifically, statutory capital and surplus was 4.26 times the level of minimum required regulatory capital on average in 2020 compared to 4.31 times the required level in 2019.

L&H sector net income of $22 billion in 2020 was less than one-half of 2019 levels, affecting the potential for capital generation. The sector reported a nearly 10 percent increase in death and annuity benefit expenses, which contributed to a ratio of total benefit expenses to premiums earned of 50 percent in 2020, rising substantially from 44.4 percent in 2019. According to Fitch Ratings, life insurer operating results in 2020 were largely impacted by higher claims paid, primarily due to increased mortality from COVID-19.24

Certain leverage ratios indicate that L&H insurers faced balance sheet pressures in 2020. The greater financial flexibility afforded by steady leverage ratios has enabled insurers to consistently fulfill policyholder obligations by: (1) returning a profit by investing the premiums received from underwriting activities; and (2) limiting the risk exposure from the policies underwritten. Insurers also employ reinsurance in order to move some of the risks off their own balance sheets and on to those of reinsurers. Figure 16 provides a view of the L&H sector’s general account leverage for the last 10 years.

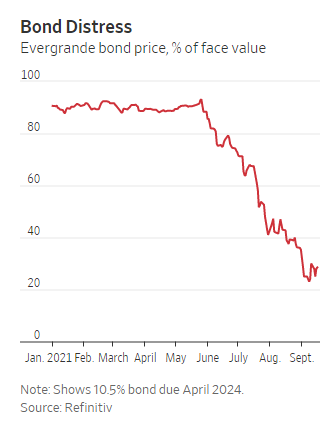

“If funding stress signs don’t emerge, don’t conclude that there is no contagion. Contagion is playing out already if you know where to look.”

The mess in China does not stop with Evergrande.

…..

Everglade shows the theft of wealth and money in a giant Ponzi scheme, not to be confused with real savings (i.e. net tangible assets at true market value)!

There is no savings glut.

The alleged savings glut is nothing but a fiat Ponzi scheme where central banks have to keep money supply soaring to keep asset prices (based on debt) from imploding!

How much longer this setup can continue before it blows up in a currency crisis, war with China, or some other major economic disruption remains a key mystery.

Tesla Inc. is readying a major upgrade of its driver-assistance software but the top federal crash investigator says the move might be premature.

Chief Executive Elon Musk said last week that drivers would soon be able to request an enhanced version of what Tesla calls its “Full Self-Driving Capability.” The upgrade is expected to add a feature intended to help vehicles navigate cities, expanding the suite of driver-assistance tools that had been designed mainly for highways.

Despite its name, Full Self-Driving doesn’t make cars fully autonomous, and Tesla instructs drivers to remain alert, with their hands on the wheel.

Jennifer Homendy, the new head of the National Transportation Safety Board, said Tesla shouldn’t roll out the city-driving tool before addressing what the agency views as safety deficiencies in the company’s technology. The NTSB, which investigates crashes and issues safety recommendations though it has no regulatory authority, has urged Tesla to clamp down on how drivers are able to use the company’s driver-assistance tools.

A MassMutual investment subsidiary has agreed to pay $4.75 million to resolve allegations by Massachusetts securities regulators including that it failed to supervise its agents, among them the social media persona “Roaring Kitty,” whose online posts helped spark January’s trading frenzy in GameStop Corp (GME.N) shares.

Massachusetts Secretary of the Commonwealth William Galvin on Thursday said MML Investors Services failed to detect the activities of Keith Gill, who touted GameStop stock in his spare time while he was working at the company.

Galvin, the state’s top securities regulator, alleged MassMutual also inadequately supervised other agents and failed to review their social media usage or catch excessive trading in their personal accounts.

The company agreed to pay a $4 million fine to resolve those allegations and another $750,000 for failing to register 478 broker-dealer agents. It also agreed to overhaul its social media policies.

Insolvency Costs Workbook – This Microsoft Excel workbook contains individual spreadsheets for all insolvency cases along with various summary schedules and assessable premium data.

Insolvency Costs Report – This PDF file contains all commentary and notes for the insolvency cost report. It includes general descriptions of categories, brief comments on individual insolvency cases, assessment and premium tax offset provisions, and premiums by state. Also included are the spreadsheets from the Costs Excel workbook, thus creating one comprehensive report. You will need Acrobat Reader to open and read this file.

Insolvency Costs Report – Comments – This file is no longer provided beginning with 2003 since all information is included in the Report PDF file. This Microsoft Word document contains all commentary and notes for the insolvency cost report. It includes general descriptions of categories, brief comments on individual insolvency cases and premium tax offset provisions.

Date Accessed: 20 Sept 2021

Publication Site: National Organization of Life & Health Insurance Guaranty Associations

Treasury Secretary Janet Yellen and IRS Commissioner Charles Rettig pressed lawmakers Wednesday to give the Internal Revenue Service more information about taxpayers’ bank accounts, as the Biden administration tries to salvage its tax-compliance proposal.

In letters to lawmakers, the administration officials again asked Congress to require banks to report annual inflows and outflows from bank accounts with at least $600 or at least $600 worth of transactions, a proposal aimed at letting the IRS target its audits more effectively. It would generate about $460 billion over a decade to cover the costs of Democrats’ planned expansion of the social safety net and climate-change policies, according to the administration.

But after a flurry of opposition from banks and credit unions, House Democrats omitted the proposal from their list of tax-policy changes this week. That was a sign that it lacked the support in the party to advance, though a scaled-back version raising about half as much money could still emerge from ongoing talks between administration officials and Congress.

The federal government ran budget surpluses from 1998 to 2001. Yet the national debt went up in every one of those four years. How can debt go up when you’re running surpluses? Easy, borrow the surpluses then flowing into the Social Security Trust Fund and call it income. Any corporate CEO who tried this stunt would go to jail. But no CEO would try because Wall Street made such boldface accounting fraud impossible more than a century ago.

…..

How can we stop politicians from so casually lying to their stockholders (you and me) for their own short-term political benefit and to the country’s long-term financial detriment? What’s needed is the equivalent of the reforms forced on corporations 140 years ago.

One justification for the Federal Reserve is to keep the power to print money out of the hands of politicians. A Federal Accounting Board would keep the power to cook the books out of their hands as well. Like the Fed, it would be run by a board of seven members, all professional accountants of long experience, serving 14-year terms. They could be removed only for cause. One member would be appointed chairman, serving a four-year term.

The board would take over the duties of the Congressional Budget Office, and the White House Office of Management and Budget would be reduced to formulating the annual budget. The board would estimate future revenue and the costs of all legislation. It would also set the rules for how the federal books must be kept (no calling borrowed money “income”), and would determine if they are accurate and complete, as a CPA does for corporate books.