The January report by former SEC Chairman Harvey Pitt lays bare deep divisions within the Public Company Accounting Oversight Board, which oversees the audits of companies valued in total at trillions of dollars.

It also alleges organizational dysfunction. There were no records documenting the rationale for several staff firings, and confusion about the roles of the PCAOB’s board members has “created some dysfunctional behavior” by them, the report found.

Current SEC Chairman Gary Gensler this month ousted William Duhnke as PCAOB chairman and is replacing the rest of the five-member board.

A PCAOB spokeswoman didn’t return a request for comment. An SEC spokesman declined to comment. Mr. Duhnke said he hasn’t seen the report and cannot comment on it.

Colorado’s Equal Pay for Equal Work Act — a set of laws aimed at ending wage discrimination, especially for women and minorities — went into effect earlier this year.

But instead of adhering to the legislation, some companies have decided to exclude Colorado-based remote employees in job listings.

Why?

The act specifies that employers hiring in Colorado must include an expected salary range and benefits in job posts. Some reports claim that companies don’t want to reveal their cards.

…..

Even if these rules are a good idea, they demand new systems and processes for any business hiring in Colorado. Many are balking, so it’s looking like a “cobra effect” law: when a well-intentioned rule backfires.

It is becoming increasingly accepted that lowering interest rates might at some point prove contractionary (the “reversal interest rate”) if lower lending margins cut the supply of bank loans. This paper argues that there are many other reasons to question reliance on monetary policy to provide economic stimulus, particularly over successive financial cycles. By encouraging the issue of debt, often for unproductive purposes, monetary stimulus becomes increasingly ineffective over time. Moreover, it threatens financial stability in a variety of ways, it leads to real resource misallocations that lower potential growth, and it finally produces a policy “debt trap” that cannot be escaped without significant economic costs. Debt-deflation and high inflation are both plausible outcomes.

https://doi.org/10.36687/inetwp151

Author(s): William White

Publication Date: 5 March 2021

Publication Site: Institute for New Economic Thinking

A National Association of Insurance Commissioners’ task force today created a subgroup to focus solely on the index-linked annuity products.

“These products are exclusively filed in the states as variable annuities and are funded through non-unitized separate accounts,” read a notice to the task force from Pete Weber, chief life actuary at the Ohio Department of Insurance. “The task force has discussed developing a draft standard for minimum interim values for these products and providing direction for implementing the standard.”

Regulators gave the Index-Linked Variable Annuity Subgroup a 2021 charge to: Provide recommendations and changes, as appropriate, to nonforfeiture, or interim value requirements related to Index-Linked Variable Annuities.

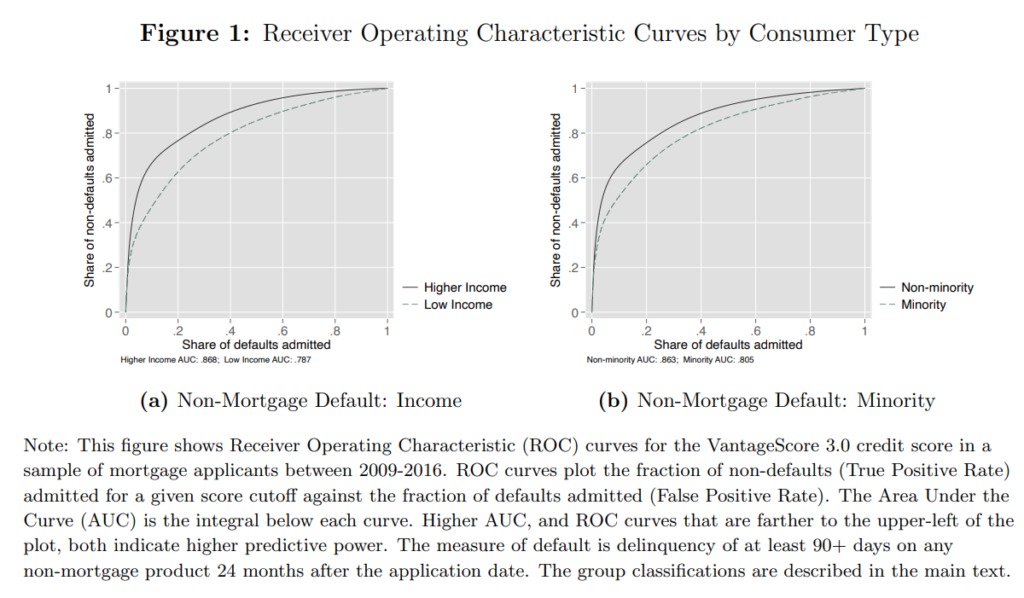

We show that lenders face more uncertainty when assessing default risk of historically under-served groups in US credit markets and that this information disparity is a quantitatively important driver of inefficient and unequal credit market outcomes. We first document that widely used credit scores are statistically noisier indicators of default risk for historically under-served groups. This noise emerges primarily through the explanatory power of the underlying credit report data (e.g., thin credit files), not through issues with model fit (e.g., the inability to include protected class in the scoring model). Estimating a structural model of lending with heterogeneity in information, we quantify the gains from addressing these information disparities for the US mortgage market. We find that equalizing the precision of credit scores can reduce disparities in approval rates and in credit misallocation for disadvantaged groups by approximately half.

But in the biggest ever study of real-world mortgage data, economists Laura Blattner at Stanford University and Scott Nelson at the University of Chicago show that differences in mortgage approval between minority and majority groups is not just down to bias, but to the fact that minority and low-income groups have less data in their credit histories.

This means that when this data is used to calculate a credit score and this credit score used to make a prediction on loan default, then that prediction will be less precise. It is this lack of precision that leads to inequality, not just bias.

…..

But Blattner and Nelson show that adjusting for bias had no effect. They found that a minority applicant’s score of 620 was indeed a poor proxy for her creditworthiness but that this was because the error could go both ways: a 620 might be 625, or it might be 615.

Decentralized Finance — or DeFi — has experienced explosive growth in the past year. But in order for DeFi to fulfill its promise as a disintermediated ecosystem that helps rather than harms, “now is the time to evaluate its benefits and dangers,” write Wharton legal studies and business ethics professor Kevin Werbach and David Gogel, a recent Wharton MBA graduate, in the article that follows. Werbach is author of the book The Blockchain and the New Architecture of Trustand leads Wharton’s Blockchain and Digital Asset Project. Werbach and Gogel recently collaborated with the World Economic Forum to create the Decentralized Finance (DeFi) Policy-Maker Toolkit, providing guidance to regulators and blockchain watchers everywhere.

….

The market experienced explosive growth beginning in 2020. According to tracking service DeFi Pulse, the value of digital assets locked into DeFi services grew from less than $1 billion in 2019 to over $15 billion at the end of 2020, and over $80 billion in May 2021. Novel business models such as yield farming — in which holders of cryptocurrencies earn rewards for providing capital to various services — and aggregation to optimize trading across exchanges in real-time are springing up rapidly. Innovations such as flash loans, which are either repaid or automatically unwound during the course of a transaction, open up both new forms of liquidity and unfamiliar risks.

The Fed has embarked on a massive expansionary quest in recent years. In 2020, total Reserve Bank assets rose from $4.2 trillion to $7.4 trillion amidst the pandemic and related government lockdown and fiscal “stimulus” policies. That was roughly three times the extraordinary growth in the consolidated balance sheet for the Reserve Banks in the 2008-2009 financial crisis. And in the latest weekly “H.4.1” release, total assets were up to $7.8 trillion – rising about a hundred billions dollars a month so far this year.

….

Today, short and long-term interest rates on government bonds rest near historic lows, important in part because the Fed massively expanded its purchases of government bonds. But low interest rates can’t be taken for granted, particularly if we get significantly higher inflationary expectations — which appear to have begun to sprout in recent weeks.

If we get significantly higher interest rates for that reason, the Reserve Bank balance sheet impact from losses on securities assets would arrive if the losses become “realized” – a realistic prospect if the Federal Reserve reverses course and starts selling off securities as a means of conducting monetary policy amidst higher inflationary expectations.

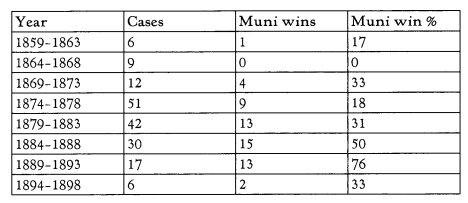

The invocation of ultra vires to escape bond obligations is nothing new, though. In the second half of the nineteenth century, municipal debtors frequently welched on their debts. In the 1850s and 1860s, cities, towns, and counties across the Midwest and West issued bonds to finance the construction of railroads and other infrastructure. Many ultimately defaulted. Rather than simply announce that they couldn’t or wouldn’t pay, however, they often contended that they needn’t pay: for one or another reason, the relevant bonds had been issued ultra vires and so were no obligation of the municipality at all. Litigation in the federal courts was common. Several hundred repudiation disputes made their way to the Supreme Court in the forty years starting 1859.

With an eye to the modern cases, we set out to understand how the Court reckoned with repudiation. We read every one of the 196 cases in which the Justices opined on bond validity (i.e. the enforceability of a bond in the hands of innocent purchasers). In a recently published article, we correct received wisdom about the cases and remark on the logical structure of the Court’s reasoning.

To the extent the municipal bond cases are remembered, modern scholars usually think of them as exemplary instances of a political model of judging. The caricature has the Court siding with bondholders even when the law called on them to rule for the repudiating municipalities. The Justices—or a majority of them—are imagined as staunch political allies of the capitalist class, set against the institutions of state government and their regard for agricultural interests. We find that this picture is inconsistent with reality. In fact, the Court ruled for the repudiating municipality in a third of all the validity cases. As importantly, the Court’s decisions reflected a readily articulable formal logic, a logic the Justices seem, to our eyes, to have applied soundly.

Citation: Buccola, Allison and Buccola, Vincent S.J., The Municipal Bond Cases Revisited (September 25, 2020). 94 American Bankruptcy Law Journal 591 (2020), Available at SSRN: https://ssrn.com/abstract=3699633

Abstract

Recent high-profile attempts to repudiate municipal bonds break from what had become a stable American norm of honoring public debt. In the nineteenth century, though, hundreds of cities, towns, and counties walked away from their bonds. The Supreme Court’s handling of repudiation in the so-called municipal bond cases conjured intense animus at the time. But the years as well as the archaic prose and sheer volume of the opinions have obscured the cases’ significance.

This article reconstructs the bond cases with an eye to modern disputes. It reports the results of our reading all 203 cases, decided 1859–1899, in which the Justices opined on bond validity. At a high level, our findings correct a stock narrative in the literature. The standard account paints the Court as a reliable champion of northeastern capitalists in what resembled regional or class politics more than law. That story does not withstand scrutiny, however. We find, for example, that the Court ruled for the repudiating municipality about a third of the time. Moreover, the decisions had a readily articulable logic at the heart of which lay a familiar law/fact distinction. Estoppel barred issuers in most instances from denying factual predicates of bond validity, but it did not prevent scrutiny of legal predicates. The Justices were willing to hold bonds void on even highly technical legal grounds.

Author(s): Allison Buccola (Independent) and Vince Buccola (Assistant Professor, The Wharton School)

Publication Date: 1 June 2021

Publication Site: Harvard Law School, Bankruptcy Roundtable

Less than half a year into the Biden Presidency, the Internal Revenue Service is already at the center of an abuse-of-power scandal. That news broke Tuesday when ProPublica, a website whose journalism promotes progressive causes, published information from what it said are 15 years of the tax returns of Jeff Bezos, Warren Buffett and other rich Americans.

Leaking such information is a crime, since under federal law tax returns are confidential. ProPublica says it received the files from “an anonymous source” and doesn’t know who provided them, how they were obtained, or what the source’s motives are.

Allow us to fill in that last blank. The story arrives amid the Biden Administration’s effort to pass the largest tax increase as a share of the economy since 1968. The main Democratic argument for a tax hike is that the rich should pay their “fair share.” The ProPublica story is a long argument that somehow the rich don’t pay enough. The timing here is no coincidence, comrade.

….

This still leaves the real scandal, which is that someone leaked confidential IRS information about individuals to serve a political agenda. This is the same tax agency that pursued a vendetta against conservative nonprofit groups during the Obama Administration. Remember Lois Lerner?

This is also the same IRS that Democrats now want to infuse with $80 billion more to chase a fanciful amount of uncollected taxes. As part of this effort, Mr. Biden wants the IRS to collect “gross inflows and outflows on all business and personal accounts from financial institutions.” Why? So the information can be leaked to ProPublica?

The bank administered a loan of some $1 billion, sending payments from Revlon to the lenders. Citibank mistakenly sent a wire transfer of the entire principal amount due when it only intended a single installment.

Under established law, the money that Citibank wired should be repaid because it was sent by mistake. But U.S. District Judge Jesse Furman upset settled law and allowed lenders to keep the money on the ground that the recipients did not have notice that the funds had been sent erroneously. If that became the rule, it would upset the important relationships among lenders, borrowers and trusted intermediaries.

….

Mistakes like this occur with surprising frequency. In 2017, the German bank KfW mistakenly transferred $5.4 billion to lenders. In China, the bank Rural Commercial Bank in Changsha thought that a customer’s 10-digit account number was actually the amount of money to be transferred, and mistakenly sent 1.2 billion yuan (around $190 million) to the customer. Deutsche Bank recently sent $6 billion to a U.S.-based hedge fund in error. In all these cases, the banks recovered the errant funds transfers almost immediately.

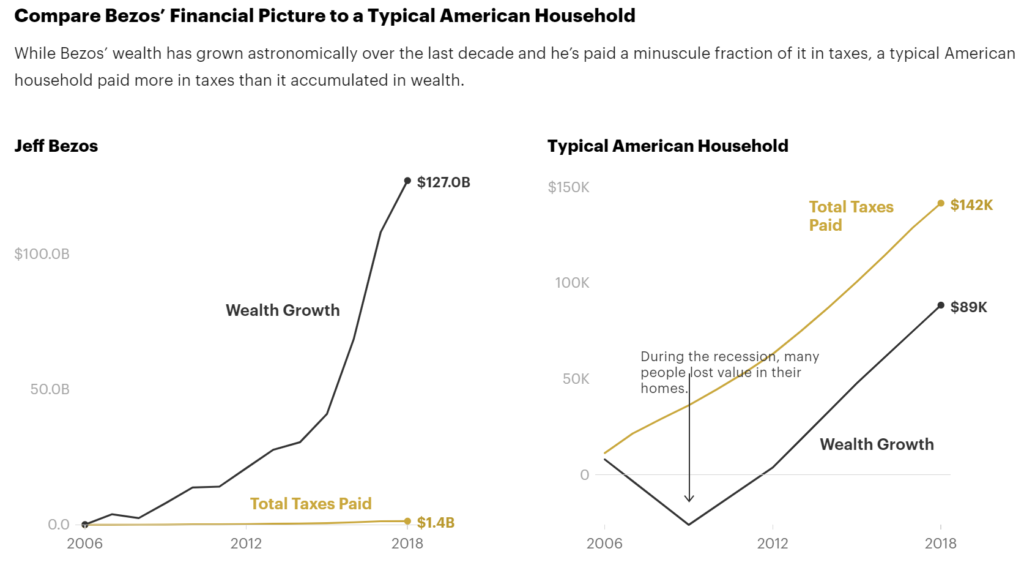

ProPublica has obtained a vast cache of IRS information showing how billionaires like Jeff Bezos, Elon Musk and Warren Buffett pay little in income tax compared to their massive wealth — sometimes, even nothing.

….

In 2011, a year in which his wealth held roughly steady at $18 billion, Bezos filed a tax return reporting he lost money — his income that year was more than offset by investment losses. What’s more, because, according to the tax law, he made so little, he even claimed and received a $4,000 tax credit for his children.

His tax avoidance is even more striking if you examine 2006 to 2018, a period for which ProPublica has complete data. Bezos’ wealth increased by $127 billion, according to Forbes, but he reported a total of $6.5 billion in income. The $1.4 billion he paid in personal federal taxes is a massive number — yet it amounts to a 1.1% true tax rate on the rise in his fortune.

Author(s): Jesse Eisinger, Jeff Ernsthausen, Paul Kiel