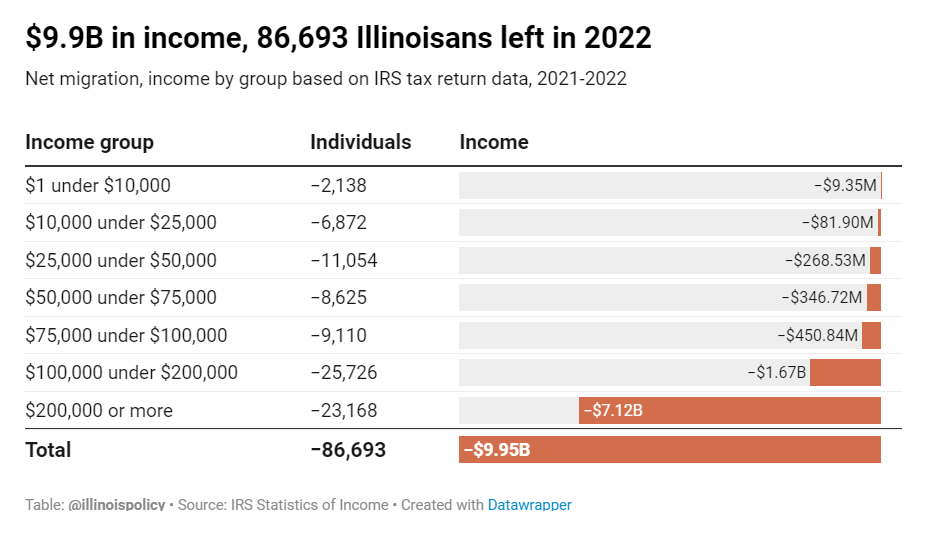

New data shows $9.9 billion flowed from Illinois to other states because people moved out in 2022. Most of those leaving earned $100,000 or more.

When Illinoisans move away, they take their money with them: $9.9 billion in 2022, according to new data from the Internal Revenue Service.

Tax returns for 2021 and 2022 show Illinois lost 86,693 individuals and $9.9 billion because of outmigration. Most of them were high-income Illinoisans.

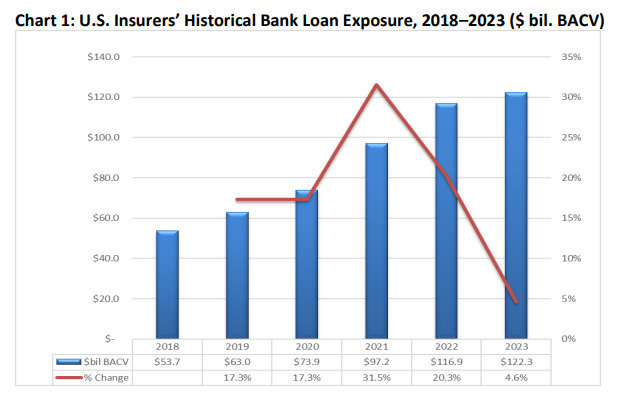

Bank loan investments increased to about $122 billion in book/adjusted carrying value (BACV) at year-end 2023 from $117 billion at year-end 2022.

Despite the 4.6% growth, bank loansremained at 1.4% of U.S. insurers’ total cash and invested assets at year-end 2023—the same as year-end 2022.

Approximately 70% of U.S. insurers’ bank loan investments were acquired, and 85% were held by life companies.

In particular, large life companies, or those with more than $10 billion in assets under management, accounted for 82% of U.S. insurers’ bank loan exposure, up from nearly 80% in 2022.

The top 25 insurance companies accounted for 75% of U.S. insurers’ total bank loan investments at year-end 2023; the top 10 accounted for about 60%.

Improvement in credit quality for U.S. insurer-bank loans continued, evidenced by a fourpercentage-point increase in those carrying NAIC 1 and NAIC 2 designations and a corresponding four-percentage-point decrease in bank loans carrying NAIC 3 and NAIC 4 designations.

Author(s): Jennifer Johnson

Publication Date: 16 July 2024

Publication Site: NAIC Capital Markets Special Report

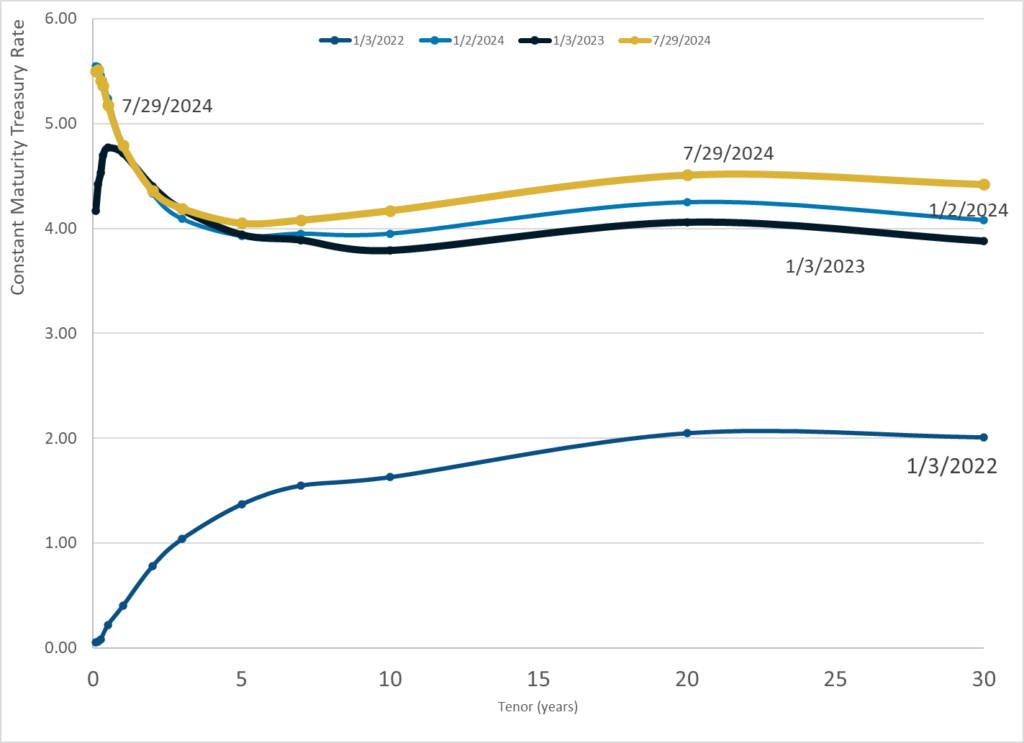

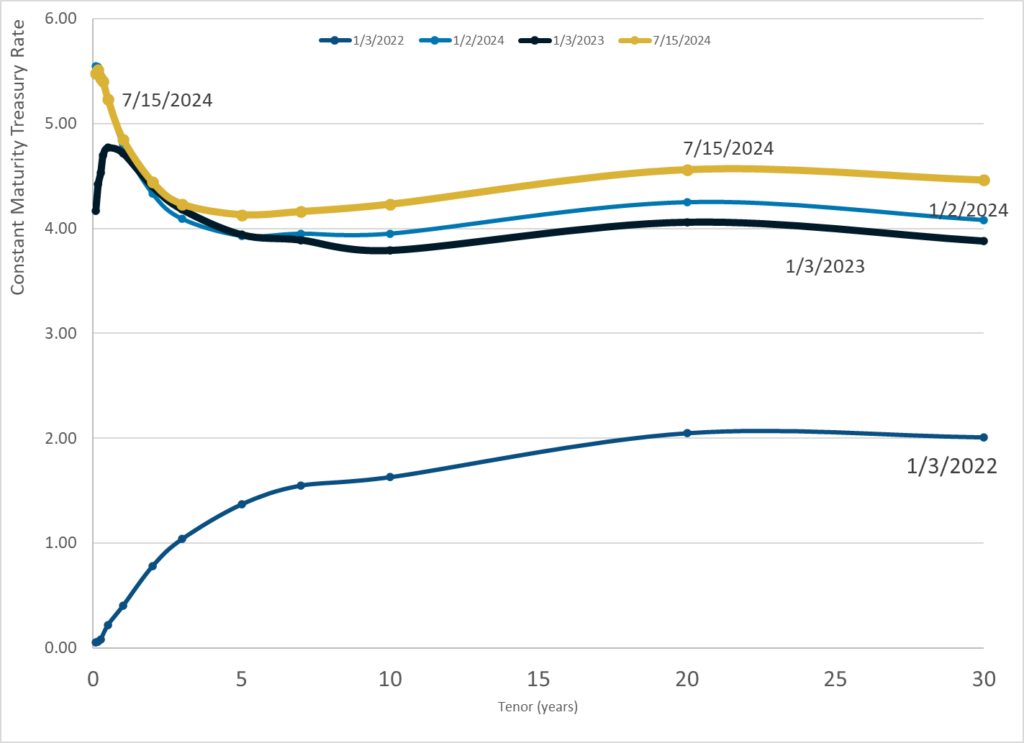

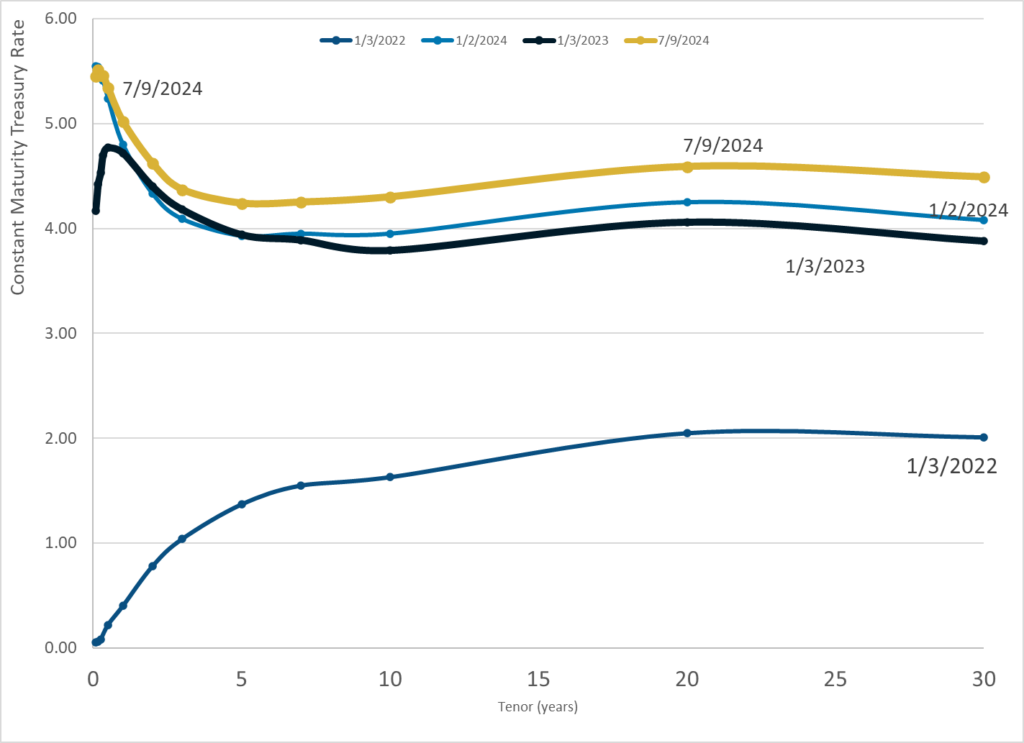

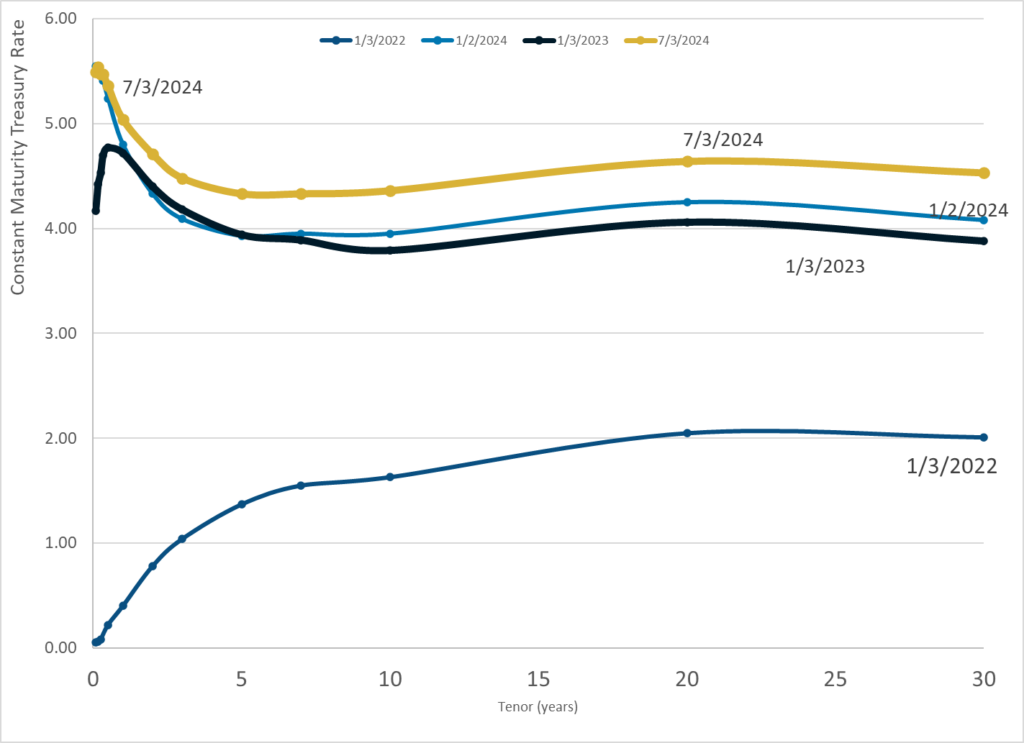

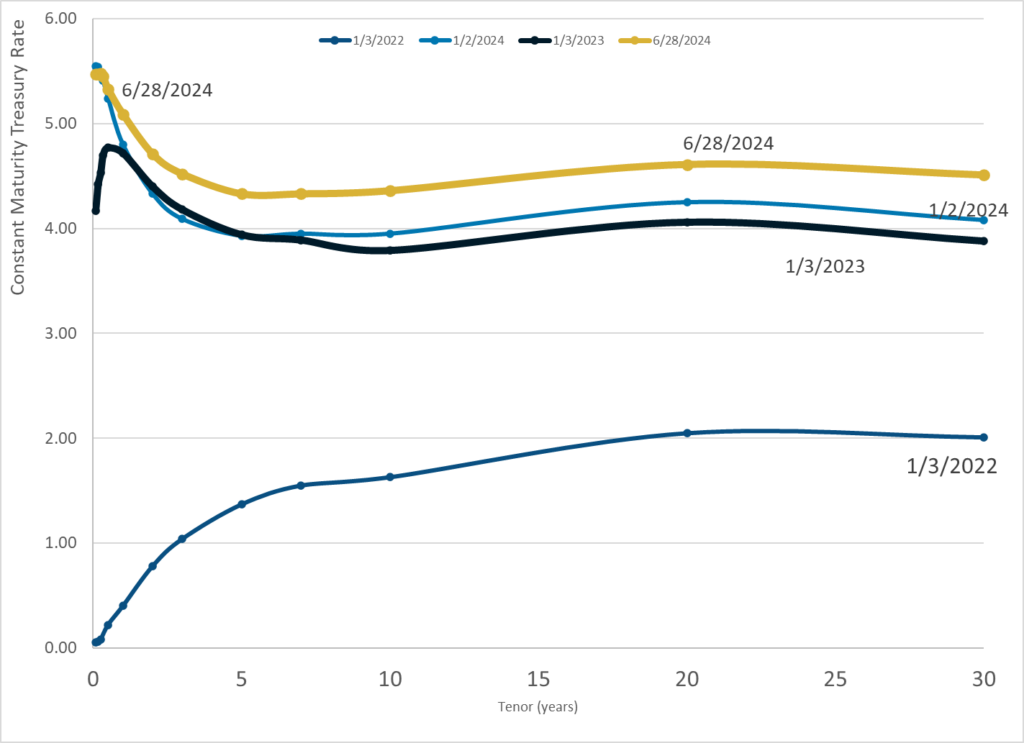

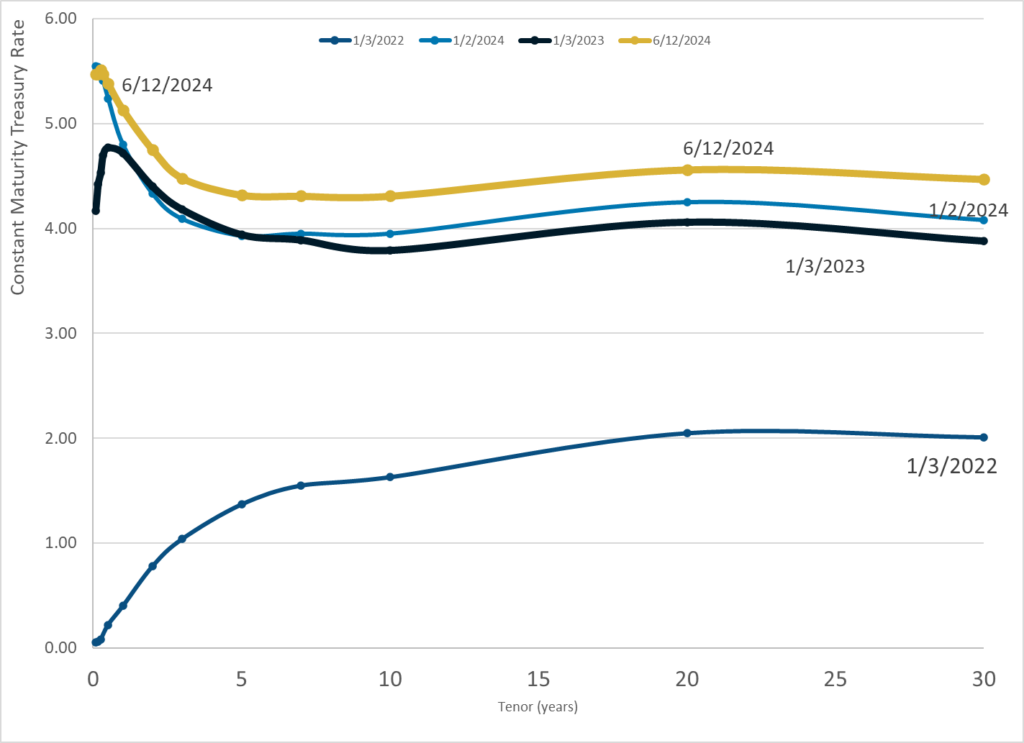

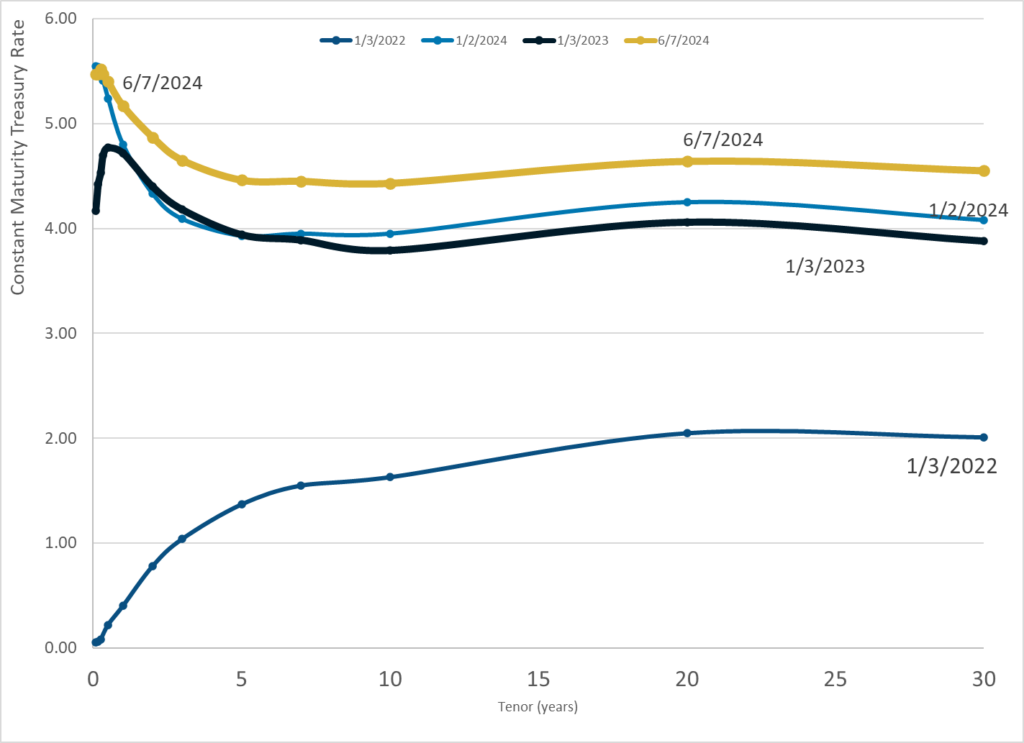

Yield on the 10-year treasury is 4.59 percent on May 29, right where it started the month. A quarter-point rally on hopes of rate cuts vanished today.

Yields are still lower than the 2024 intraday peak of 4.74 percent, but they are nearly 70 basis points higher than the start of the year as rate cut after rate cut hopes keep getting priced out.

Minneapolis Federal Reserve President Neel Kashkari says he wants to see “many more months” of positive inflation numbers before interest rates start to come down — and refused to rule out a rate hike if needed.

When and how should text-generating artificial intelligence (AI) programs such as ChatGPT help write research papers? In the coming months, 4000 researchers from a variety of disciplines and countries will weigh in on guidelines that could be adopted widely across academic publishing, which has been grappling with chatbots and other AI issues for the past year and a half. The group behind the effort wants to replace the piecemeal landscape of current guidelines with a single set of standards that represents a consensus of the research community.

Known as CANGARU, the initiative is a partnership between researchers and publishers including Elsevier, Springer Nature, Wiley; representatives from journals eLife, Cell, and The BMJ; as well as industry body the Committee on Publication Ethics. The group hopes to release a final set of guidelines by August, which will be updated every year because of the “fast evolving nature of this technology,” says Giovanni Cacciamani, a urologist at the University of Southern California who leads CANGARU. The guidelines will include a list of ways authors should not use the large language models (LLMs) that power chatbots and how they should disclose other uses.

Since generative AI tools such as ChatGPT became public in late 2022, publishers and researchers have debated these issues. Some say the tools can help draft manuscripts if used responsibly—by authors who do not have English as their first language, for example. Others fear scientific fraudsters will use them to publish convincing but fake work quickly. LLMs’ propensity to make things up, combined with their relative fluency in writing and an overburdened peer-review system, “poses a grave threat to scientific research and publishing,” says Tanya De Villiers-Botha, a philosopher at Stellenbosch University.