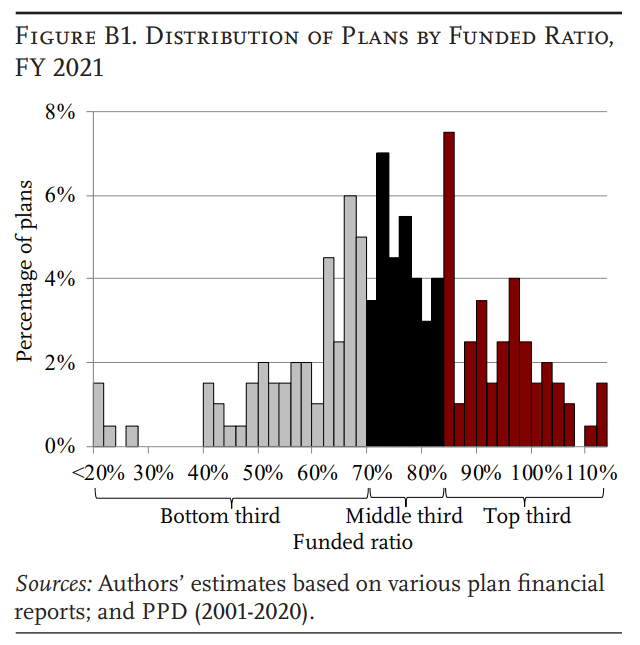

The aggregate funded ratio improved from 73 to 75 percent from FY 2020 to 2021. At the same time, contribution rates rose from 21 to 22 percent of payrolls.

While initial expectations for public pensions were low due to COVID, financial markets rebounded and municipal tax revenues were quite resilient.

Yet one other COVID-related factor – cuts to the state and local workforce – impacted public pension finances in FY 2021.

These cuts had little impact on funded status and required contribution amounts, but they do explain the rise in contribution rates, which are expressed as a share of lower payrolls.

Author(s): Jean-Pierre Aubry, Kevin Wandrei

Publication Date: June 2021

Publication Site: Center for Retirement Research at Boston College

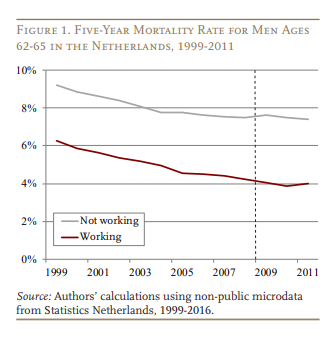

As expected, the raw data show that Dutch men who worked at ages 62-65 were less likely to die over the subsequent five years than men who were not working (see Figure 1). Importantly, Figure 1 shows that mortality decreased at nearly identical rates for working and non-working men between 1999 and 2008, before the policy became available. The fact that these trends are parallel provides more confidence in the policy experiment, indicating that whatever was happening to working men prior to the DWB was also happening to non-working men. In contrast, the mortality rate in 2009-2011 continued to improve somewhat for working men, who were benefiting from the DWB, while the mortality rate for non-working men plateaued.

Author(s): Alice Zulkarnain, Matthew S. Rutledge

Publication Date: May 2021

Publication Site: Center for Retirement Research at Boston College

Abstract Workers have the option of claiming Social Security retirement benefits at any age between 62 and 70, with later claiming resulting in higher monthly benefits. These higher monthly benefits reflect an actuarial adjustment designed to keep lifetime benefits equal, for an individual with average life expectancy, regardless of when benefits are claimed. The actuarial adjustments, however, are decades old. Since then, interest rates have declined; life expectancy has increased; and longevity improvements have been much greater for high earners than low earners. This paper explores how changes in longevity and interest rates have affected the fairness of the actuarial adjustment over time and how the disparity in life expectancy affects the equity across the income distribution. It also looks at the impact of these developments on the costs of the program and the progressivity of benefits.

The paper found that: • The increases in life expectancy and the decline in interest rates argue for smaller reductions for early claiming and a smaller delayed retirement credit for later claiming. • Specifically, the benefit at 62 should equal 77.5 percent, as opposed to 70.0 percent, of the full age-67 benefit, and the benefit at 70 should equal 119.9 percent, instead of 124.0 percent, of the full benefit. • The outdated actuarial adjustments are a modest moneymaker for the program – about $1.9 billion in 2018, with most of the gains coming from those claiming at 62, who are typically lower earners. Surprisingly, the correlations between earnings and life expectancy and between earnings and claiming behavior have only modest implications for both the cost and progressivity of Social Security benefits. • Finally, the cost and distributional effects of earnings-related life expectancy and claiming cannot be addressed through the actuarial adjustments for early and late claiming. They reflect the fact that high earners get their large benefits for a long time and low earners get their more modest benefits for a shorter time.

Authors: Andrew G. Biggs, Anqi Chen, and Alicia H. Munnell

Publication Date: January 2021

Publication Site: Center for Retirement Research at Boston College

Workers have the option of claiming Social Security retirement benefits at any age between 62 and 70, with later claiming resulting in higher monthly benefits. These higher monthly benefits reflect an actuarial adjustment designed to keep lifetime benefits equal, for an individual with average life expectancy, regardless of when benefits are claimed. The actuarial adjustments, however, are decades old. Since then, interest rates have declined; life expectancy has increased; and longevity improvements have been much greater for high earners than low earners. This paper explores how changes in longevity and interest rates have affected the fairness of the actuarial adjustment over time and how the disparity in life expectancy affects the equity across the income distribution. It also looks at the impact of these developments on the costs of the program and the progressivity of benefits.

The paper found that:

The increases in life expectancy and the decline in interest rates argue for smaller reductions for early claiming and a smaller delayed retirement credit for later claiming.

Specifically, the benefit at 62 should equal 77.5 percent, as opposed to 70.0 percent, of the full age-67 benefit, and the benefit at 70 should equal 119.9 percent, instead of 124.0 percent, of the full benefit.

The outdated actuarial adjustments are a modest moneymaker for the program – about $1.9 billion in 2018, with most of the gains coming from those claiming at 62, who are typically lower earners. Surprisingly, the correlations between earnings and life expectancy and between earnings and claiming behavior have only modest implications for both the cost and progressivity of Social Security benefits.

Finally, the cost and distributional effects of earnings-related life expectancy and claiming cannot be addressed through the actuarial adjustments for early and late claiming. They reflect the fact that high earners get their large benefits for a long time and low earners get their more modest benefits for a shorter time.

The policy implications of the findings are:

Increases in life expectancy and the decline in interest rates suggest smaller reductions for early claiming and a smaller delayed retirement credit for later claiming.

Accounting for differential mortality would involve changing benefits, and is not a problem that can be solved by tinkering with the actuarial adjustments.