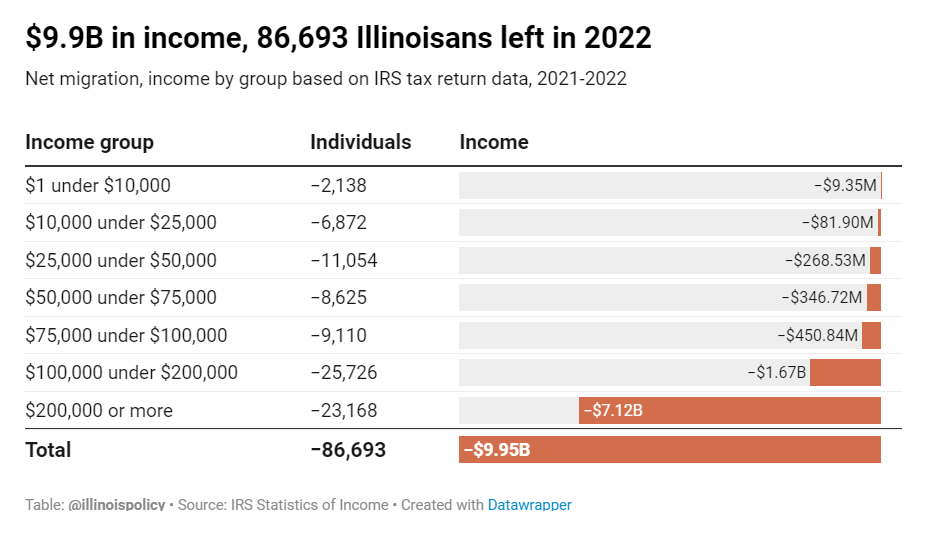

New data shows $9.9 billion flowed from Illinois to other states because people moved out in 2022. Most of those leaving earned $100,000 or more.

When Illinoisans move away, they take their money with them: $9.9 billion in 2022, according to new data from the Internal Revenue Service.

Tax returns for 2021 and 2022 show Illinois lost 86,693 individuals and $9.9 billion because of outmigration. Most of them were high-income Illinoisans.

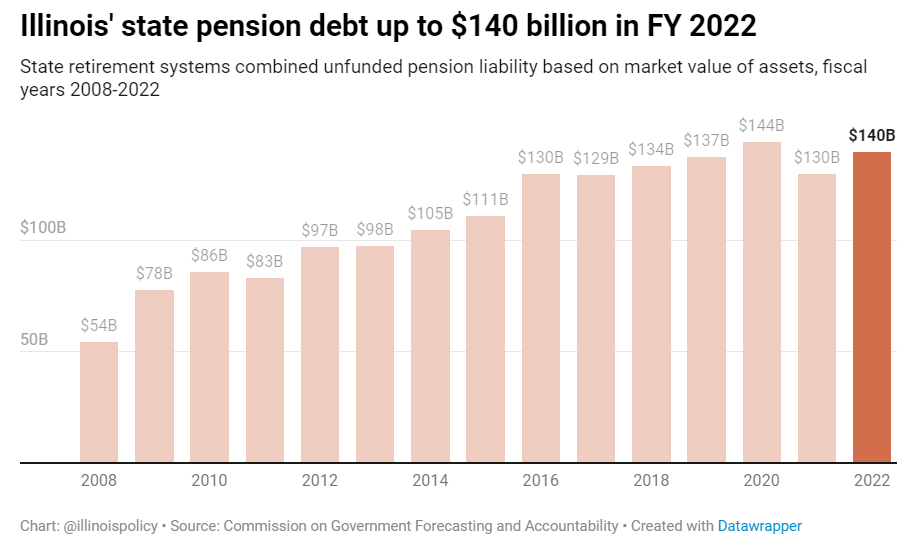

Illinois’ five statewide pensions system saw their debt increase by nearly $10 billion to a grand total of $140 billion in fiscal year 2022. Pensions will cost the state nearly $11 billion next year, but that’s still $4.4 billion too little.

Illinois’ state pension debt now stands at $139.7 billion, according to a new report from the Illinois General Assembly’s Commission on Government Forecasting and Accountability.

That is up $9.8 billion from 2021, when state pensions were benefitting from healthy investment returns. After markets cooled substantially, state pension debt in the fiscal year that ended July 1 continued to grow, increasing for the 11th time in 15 years.

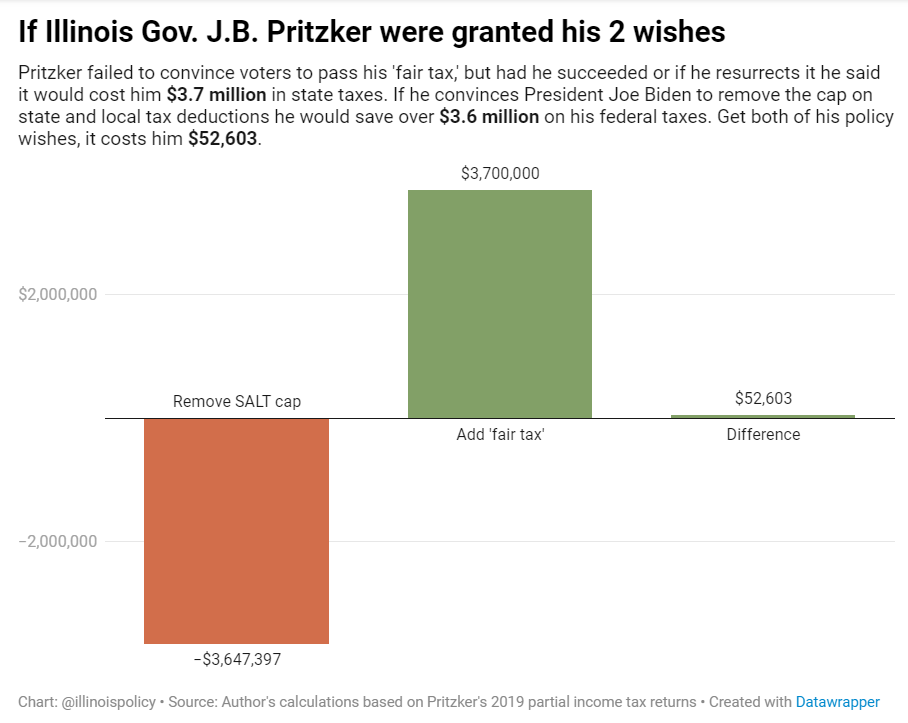

Of course, no one can know the true extent to which Pritzker has been able to reduce his tax bills through loopholes and carve-outs over the years, because he refuses to release his full tax returns. In recent years it has been revealed Pritzker went to great lengths to avoid paying taxes, removing toilets from his Gold Coast mansion to skimp on his property tax bill by $331,000 and establishing shell corporations in the Bahamas in a likely attempt to avoid U.S. income taxes. The toilet ploy earned him a federal investigation.

The letter, which pushes for tax reforms that would almost exclusively benefit the wealthy, comes less than six months after Pritzker’s progressive income tax amendment was rejected by voters and is a significant departure from his previous stance on taxation. In the letter, Pritzker claims the cap hurts middle-class taxpayers and is “untenable” during these dire economic times. Because the data is clear on who directly benefits from the SALT deduction, one can only assume the governor is implying higher taxes on the wealthy also hurt Americans with lower incomes.

That is precisely the argument opponents of the “fair tax” made after the governor first unveiled his tax-the-rich scheme in 2019.

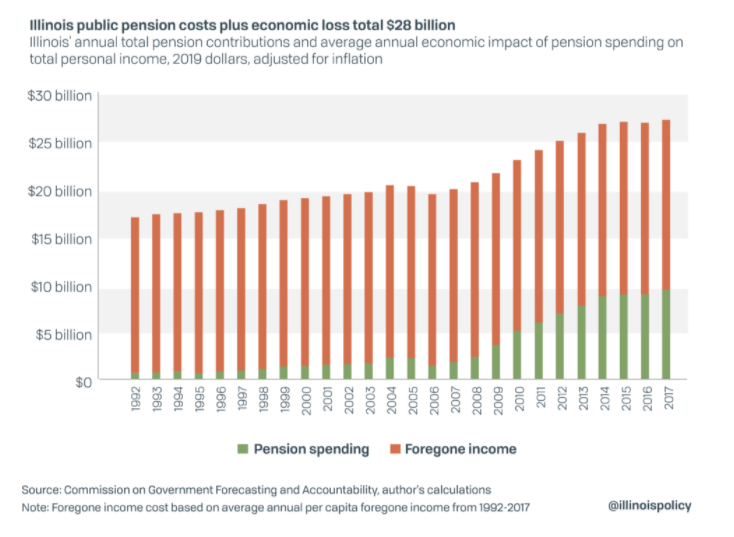

Despite the record increase in pension expenditures in the past several decades, Illinois’ pension system remains the nation’s worst by multiple measures. According to Moody’s Investors Service, Illinois’ pension debt was equal to 500% of the state’s revenues in fiscal year 2018 and almost 30% of the entire state economy, both the highest rates in the nation. At the same time, Illinois’ credit rating has been in precipitous decline and now sits at the lowest credit rating in the nation.

As pension debt continues to increase, so do required pension contributions. Pension contributions now consume 26.5% of the state’s general funds budget, up from less than 4% during the years 1990 through 1997.

Increase the public pensions funding target to 100% from 90% in accordance with actuarial best practices. The goal year for 100% funding would remain 2045.

Gradually increase retirement ages for current workers under age 45 by a maximum of five years.

Apply a pensionable salary cap of $100,000 that grows with inflation. Government workers could still earn more than $100,000, but their pensions could not be based on more than the cap. The cap would only apply to employees not currently receiving a retirement check.

Replace Tier 1 retirees’ 3% compounding benefit increase with true cost-of-living adjustments tied to inflation. Annual increases would be simple, not compounding, and rise with the consumer price index for urban consumers, as reported by the U.S. Bureau of Labor Statistics.

Increase Tier 2 COLAs from half of inflation to full inflation. This would end the unfair subsidization of older workers by younger workers and could prevent a potential lawsuit.

Implement COLA holidays to allow inflation to catch up to past benefit increases. If a worker has been retired for eight years or more, they would skip every other year for 16 years for a total of eight adjustment periods at 0%. If a retiree has been receiving benefits for seven years, they would skip one payment every other year for 14 years, and so on.

Enroll all newly hired employees in a defined contribution personal retirement account with a 4% guaranteed employer match. This would ensure the state never gets into pension trouble again. This would also provide state workers with a portable retirement benefit they could take with them from employer to employer, rather than being forced to stay with the state in order to maximize retirement benefits.