Housing affordability continues to soar out of reach of most buyers. Not only are prices at a new record level, mortgage rates remain close to 7.0 percent.

Chart Notes

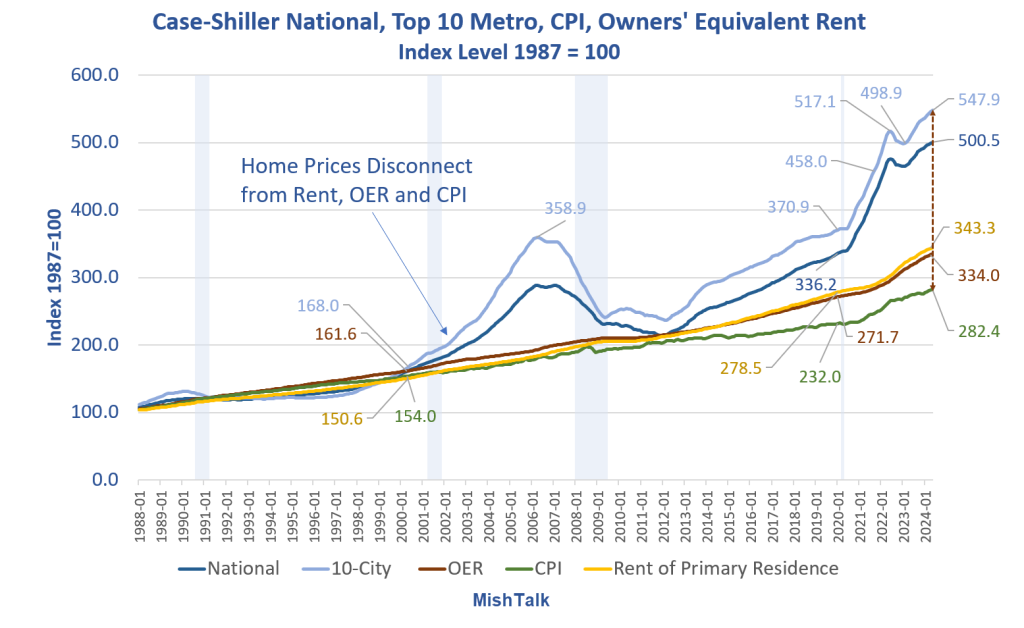

Case-Shiller measures repeat sales of the same price over time. It is the best measure of price, but it lags. Current data is as of May which reflects sales 1-3 months prior.

The CPI, OER, and Rent of Primary Residence are all from the BLS.

OER stands for Owners’ Equivalent Rent. It is the rent one would pay if someone was renting instead of paying a mortgage.

The Federal Reserve Bank of New York on Wednesday released its quarterly report on household debt and credit for the final three months of 2020, with its strategists and statisticians deciding to dig deeper into mortgage originations, the types of homebuyers during the Covid-19 pandemic and to what extent Americans are taking out cash against their home equity. While much of what they found confirms many of the narratives about the housing market, it’s the sheer magnitude of the move that’s breathtaking and puts into context where the economy stands almost one year after the coronavirus crisis began in the U.S.

At the highest level, mortgage originations reached almost $1.2 trillion in the final three months of 2020, the highest quarterly volume in the history of the New York Fed’s data, which begins in 2000. Americans refinanced more mortgage debt last year than any time since 2003, while mortgages taken out to purchase a home surged to the highest since 2006. First-time buyers took on more debt than at any time in history, while mortgages for repeat buyers and those looking for a second home or an investment property reached the highest in more than a decade.

Meanwhile, home prices soared across the U.S., with the S&P CoreLogic Case-Shiller index jumping 9.5% in November, the most since 2014 (December’s figures will be released next week). This surge led to “a notable increase in cashout refinance volumes, which spiked in the fourth quarter of 2020 and show no sign of abating,” the New York Fed researchers said in a blog post. Collectively, homeowners withdrew $182 billion in home equity in 2020, or an average of about $27,000 for each household. Even those who chose not to take out extra cash saved an average of $200 a month on their mortgage payments.