State and local policymakers face a growing pension cost burden, but often lack understanding of the root causes.

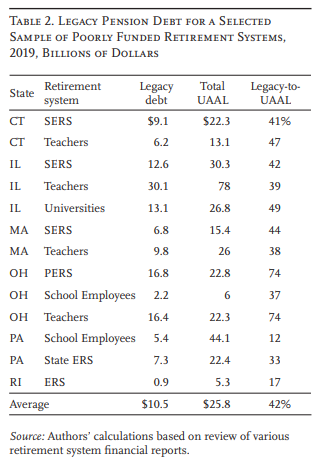

One underappreciated cause is “legacy debt” – unfunded liabilities accumulated long ago, before plans adopted modern funding practices.

Legacy debt still exists today because historical unfunded liabilities were ultimately paid in full using some of the money intended to fund later benefits.

In a sample of plans with particularly low funded ratios, legacy debt averaged more than 40 percent of unfunded liabilities.

A failure to recognize the legacy debt has provided misleading information about benefit generosity, hindering progress toward effective solutions.

Author(s): Jean-Pierre Aubry

Publication Date: April 2022

Publication Site: Center for Retirement Research at Boston College

The research showed that the rate at which older workers left employment increased dramatically during the pandemic.

This was especially the case with women — an 8-percentage-point increase vs. 7 points for men; Asian Americans — a 13-point increase; those with less than a college degree — a 10-point increase; and workers with occupations that did not lend themselves to remote work.

….

There was one exception: Workers 70 and older were 5.9 percentage points more likely to leave the workforce and retire. The study noted that these workers were likely already receiving Social Security benefits, so claiming did not markedly increase.

Among all workers 55 and older, the monthly claiming rate for Social Security benefits remained constant between April 2019 and June 2021, the researchers found.

At the outset of the pandemic recession, many feared it would undermine workers’ employer-sponsored retirement plans.

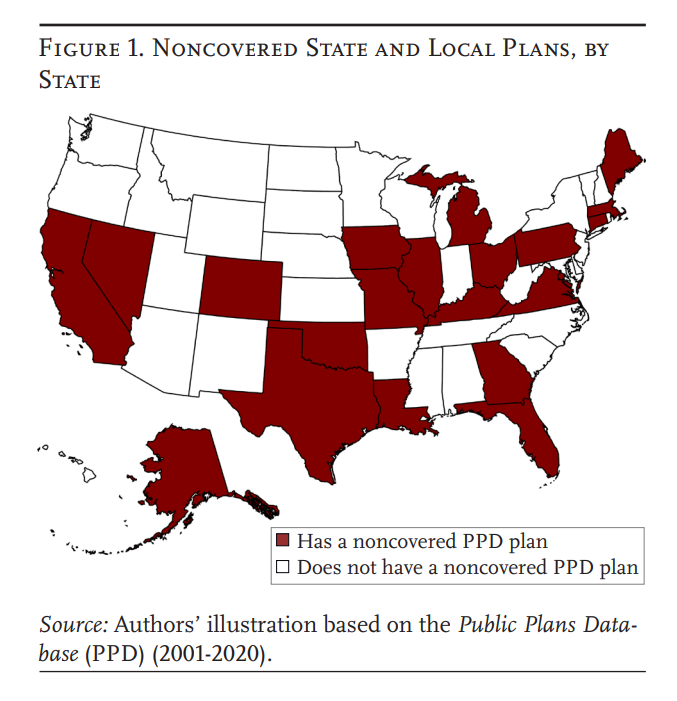

State and local employees who are not covered by Social Security would have been particularly vulnerable, as they lack the buffer this program offers.

Their employer defined benefit plans would have been hurt by a long recession with poor investment returns and reduced contributions due to tax shortfalls.

Instead, these plans exceeded their return targets; tax revenues held up; and government sponsors got stimulus aid, so plan funded ratios actually improved.

And long-term structural headwinds such as negative cash flows and aggressive return targets still pose little risk to their ability to pay future benefits.

Author(s):Jean-Pierre Aubry and Kevin Wandrei

Publication Date: January 2022

Publication Site: Center for Retirement Research at Boston College, Working Paper

Many U.S. towns and cities are years behind on their pension obligations. Now some are effectively planning to borrow money and put it into stocks and other investments in a bid to catch up.

State and local governments have borrowed about $10 billion for pension funding this year through the end of August, more than in any of the previous 15 full calendar years, according to an analysis of Bloomberg data by Municipal Market Analytics. The number of individual municipalities borrowing for pensions soared to 72 from a 15-year average of 25.

Among those considering what is known as pension obligation borrowing is Norwich, a city in southeastern Connecticut with a population of 40,000. Its yearly payment toward its old pension debts has climbed to $11 million in 2022—four times the annual retirement contribution for current workers and 8% of the city’s budget. The city will vote in November on whether to sell $145 million in 25-year bonds to cover the pensions of retired police officers, firefighters, city workers and school employees.

….

In 2009, Boston College’s Center for Retirement Research examined pension obligation bonds issued since 1986 and found that most of the borrowers had lost money because their pension-fund investments returned less than the amount of interest they were paying. A 2014 update found those losses had reversed and returns were exceeding borrowing costs by 1.5 percentage points.

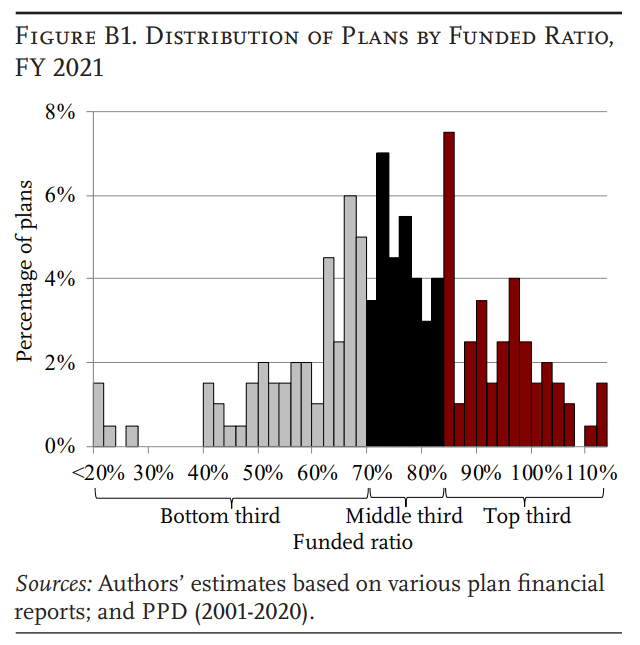

The aggregate funded ratio improved from 73 to 75 percent from FY 2020 to 2021. At the same time, contribution rates rose from 21 to 22 percent of payrolls.

While initial expectations for public pensions were low due to COVID, financial markets rebounded and municipal tax revenues were quite resilient.

Yet one other COVID-related factor – cuts to the state and local workforce – impacted public pension finances in FY 2021.

These cuts had little impact on funded status and required contribution amounts, but they do explain the rise in contribution rates, which are expressed as a share of lower payrolls.

Author(s): Jean-Pierre Aubry, Kevin Wandrei

Publication Date: June 2021

Publication Site: Center for Retirement Research at Boston College

As expected, the raw data show that Dutch men who worked at ages 62-65 were less likely to die over the subsequent five years than men who were not working (see Figure 1). Importantly, Figure 1 shows that mortality decreased at nearly identical rates for working and non-working men between 1999 and 2008, before the policy became available. The fact that these trends are parallel provides more confidence in the policy experiment, indicating that whatever was happening to working men prior to the DWB was also happening to non-working men. In contrast, the mortality rate in 2009-2011 continued to improve somewhat for working men, who were benefiting from the DWB, while the mortality rate for non-working men plateaued.

Author(s): Alice Zulkarnain, Matthew S. Rutledge

Publication Date: May 2021

Publication Site: Center for Retirement Research at Boston College

Eight states have seen the biggest drops in nursing home use: Florida, Georgia, Louisiana, New Jersey, New Mexico, North Carolina, South Carolina, and Tennessee. Many of these states have experienced fast growth in their minority populations or have more generous state allocations of Medicaid funds for long-term care services delivered in the home.

Growing diversity is actually the second-biggest reason for lower nursing home residence, accounting for one-fifth of the decline, according to the study, which was funded by the U.S. Social Security Administration and is based on U.S. Census data.

Abstract Workers have the option of claiming Social Security retirement benefits at any age between 62 and 70, with later claiming resulting in higher monthly benefits. These higher monthly benefits reflect an actuarial adjustment designed to keep lifetime benefits equal, for an individual with average life expectancy, regardless of when benefits are claimed. The actuarial adjustments, however, are decades old. Since then, interest rates have declined; life expectancy has increased; and longevity improvements have been much greater for high earners than low earners. This paper explores how changes in longevity and interest rates have affected the fairness of the actuarial adjustment over time and how the disparity in life expectancy affects the equity across the income distribution. It also looks at the impact of these developments on the costs of the program and the progressivity of benefits.

The paper found that: • The increases in life expectancy and the decline in interest rates argue for smaller reductions for early claiming and a smaller delayed retirement credit for later claiming. • Specifically, the benefit at 62 should equal 77.5 percent, as opposed to 70.0 percent, of the full age-67 benefit, and the benefit at 70 should equal 119.9 percent, instead of 124.0 percent, of the full benefit. • The outdated actuarial adjustments are a modest moneymaker for the program – about $1.9 billion in 2018, with most of the gains coming from those claiming at 62, who are typically lower earners. Surprisingly, the correlations between earnings and life expectancy and between earnings and claiming behavior have only modest implications for both the cost and progressivity of Social Security benefits. • Finally, the cost and distributional effects of earnings-related life expectancy and claiming cannot be addressed through the actuarial adjustments for early and late claiming. They reflect the fact that high earners get their large benefits for a long time and low earners get their more modest benefits for a shorter time.

Authors: Andrew G. Biggs, Anqi Chen, and Alicia H. Munnell

Publication Date: January 2021

Publication Site: Center for Retirement Research at Boston College

Workers have the option of claiming Social Security retirement benefits at any age between 62 and 70, with later claiming resulting in higher monthly benefits. These higher monthly benefits reflect an actuarial adjustment designed to keep lifetime benefits equal, for an individual with average life expectancy, regardless of when benefits are claimed. The actuarial adjustments, however, are decades old. Since then, interest rates have declined; life expectancy has increased; and longevity improvements have been much greater for high earners than low earners. This paper explores how changes in longevity and interest rates have affected the fairness of the actuarial adjustment over time and how the disparity in life expectancy affects the equity across the income distribution. It also looks at the impact of these developments on the costs of the program and the progressivity of benefits.

The paper found that:

The increases in life expectancy and the decline in interest rates argue for smaller reductions for early claiming and a smaller delayed retirement credit for later claiming.

Specifically, the benefit at 62 should equal 77.5 percent, as opposed to 70.0 percent, of the full age-67 benefit, and the benefit at 70 should equal 119.9 percent, instead of 124.0 percent, of the full benefit.

The outdated actuarial adjustments are a modest moneymaker for the program – about $1.9 billion in 2018, with most of the gains coming from those claiming at 62, who are typically lower earners. Surprisingly, the correlations between earnings and life expectancy and between earnings and claiming behavior have only modest implications for both the cost and progressivity of Social Security benefits.

Finally, the cost and distributional effects of earnings-related life expectancy and claiming cannot be addressed through the actuarial adjustments for early and late claiming. They reflect the fact that high earners get their large benefits for a long time and low earners get their more modest benefits for a shorter time.

The policy implications of the findings are:

Increases in life expectancy and the decline in interest rates suggest smaller reductions for early claiming and a smaller delayed retirement credit for later claiming.

Accounting for differential mortality would involve changing benefits, and is not a problem that can be solved by tinkering with the actuarial adjustments.