Link:https://taxfoundation.org/corporate-tax-rates-by-country-2021/?

Graphic:

Excerpt:

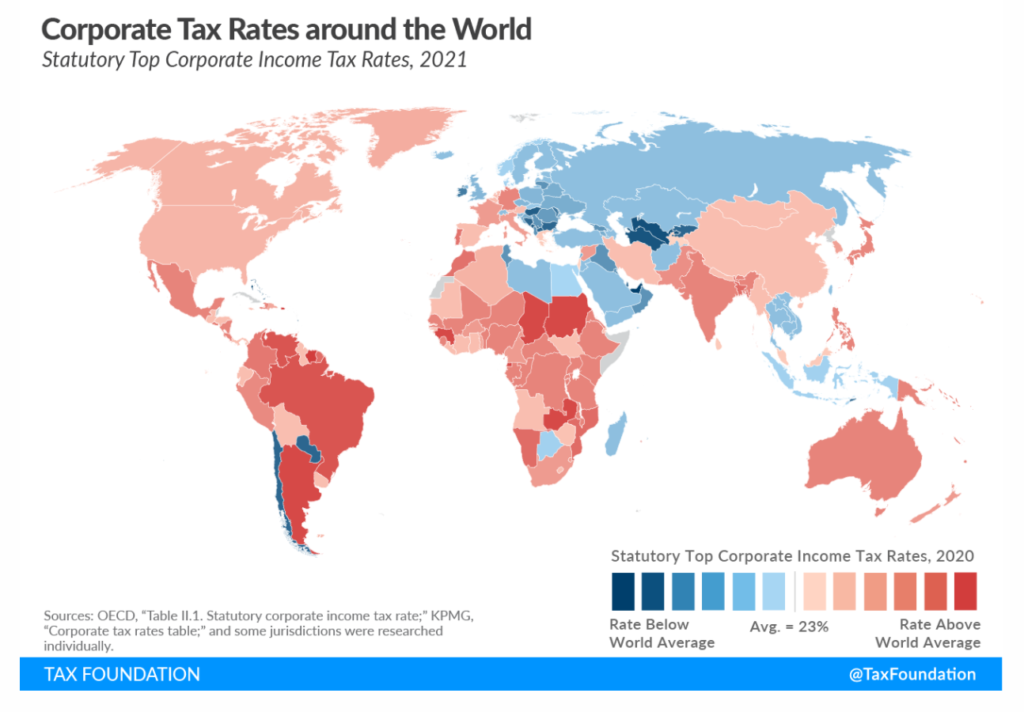

In 2021, 20 countries made changes to their statutory corporate income tax rates. Three countries—Bangladesh, Argentina, and Gibraltar—increased their top corporate tax rates, while 17 countries—including Chile, Tunisia, and France—reduced their corporate tax rates.

Comoros (50 percent), Puerto Rico (37.5 percent), and Suriname (36 percent) are the jurisdictions with the highest corporate tax rates in the world, while Barbados (5.5 percent), Uzbekistan (7.5 percent), and Turkmenistan (8 percent) levy the lowest corporate rates. Fifteen jurisdictions do not impose corporate tax.

The worldwide average statutory corporate income tax rate, measured across 180 jurisdictions, is 23.54 percent. When weighted by GDP, the average statutory rate is 25.44 percent.

Asia has the lowest regional average rate, at 19.62 percent, while Africa has the highest regional average statutory rate, at 27.97 percent. However, when weighted for GDP, Europe has the lowest regional average rate at 23.97 percent and South America has the highest at 31.03 percent.

The average top corporate rate among EU27 countries is 21.30 percent, 23.04 percent among OECD countries, and 69 percent in the G7.

The worldwide average statutory corporate tax rate has consistently decreased since 1980, with the largest decline occurring in the early 2000s.

The average statutory corporate tax rate has declined in every region since 1980.

Author(s): Sean Bray

Publication Date: 9 Dec 2021

Publication Site: Tax Foundation