Graphic:

Excerpt:

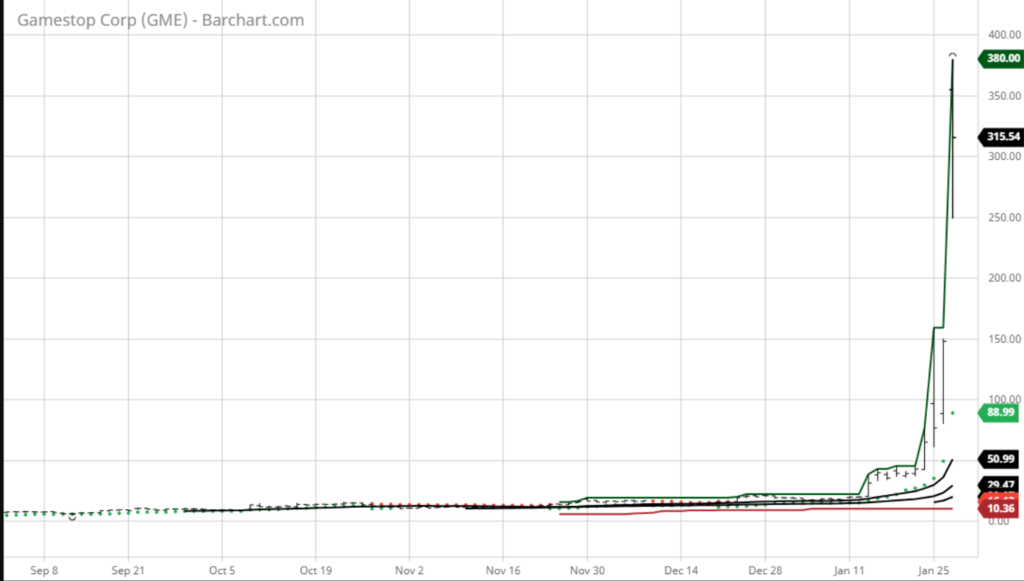

That chart ends at yesterday’s close. Things have been even more crazy overnight, with the price hitting $500/share. There have been gyrations caused by the shutdown of the chatrooms and some retail platforms stopping trading in this and other heavily shorted stocks. But the fundamental dynamic in play now–shorts slitting their own throats in panicked buying to cover–means that attempts to constrain the long herd will not have a lasting impact.

The short interest that had to (and has to) be covered is huge–short interest in GME was 140 percent of outstanding shares–and a larger share of the float. (How can there be more shorts than shares? The same share can be borrowed and lent multiple times!) The effects of the short covering are seen not only in the price, but in the stratospheric cost of borrowing shares. Earlier this week it was about 30 percent–juice loan territory. Now it is at 100 percent.

In many respects, this is reminiscent of some of the more storied episodes in Wall Street history, or more recently the 2008 VW corner which punished shorts severely. But there is a major difference. In some of the earlier episodes (including major corners of shorts in railroad stocks in the 19th century, or battles between shorts and stock pools in the 1920s, or the VW case), there was a single dominant long squeezing the overextended shorts. Here, it seems that the driving force is a relatively large group of small longs, acting with a common purpose.

Author(s): Craig Pirrong

Publication Date: 28 January 2021

Publication Site: Streetwise Professor