Graphic:

Excerpt:

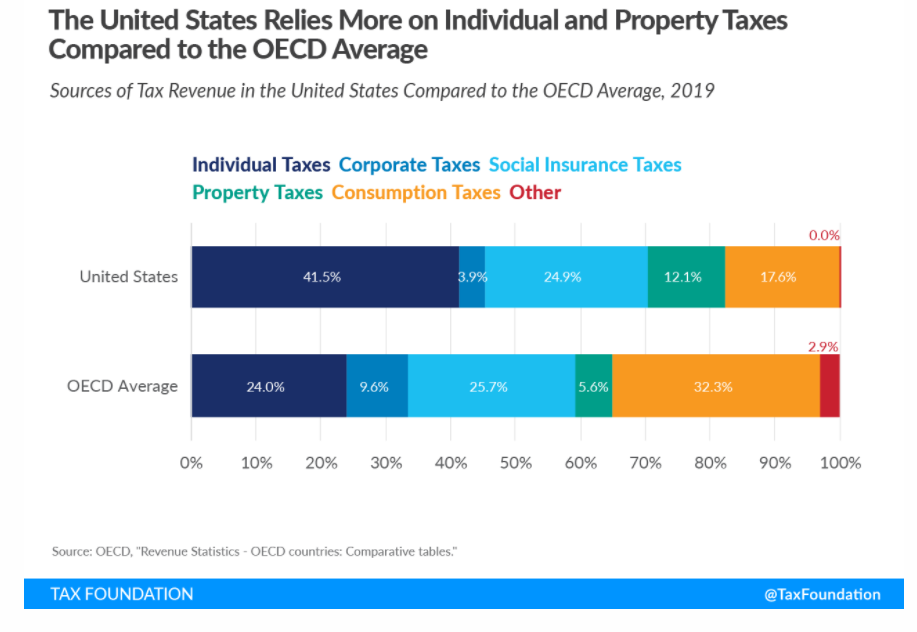

Compared to the OECD average, the United States relies significantly more on individual income taxes and property taxes. While OECD countries on average raised 24 percent of total tax revenue from individual income taxes, the share in the United States was 41.5 percent, a difference of 17.5 percentage points. This is partially because more than half of business income in the United States is reported on individual tax returns. OECD countries on average raised 5.6 percent of total tax revenue from property taxes, compared to 12.1 percent in the United States.

The United States relies much less on consumption taxes than other OECD countries. Taxes on goods and services accounted for only 17.6 percent of total tax revenue in the United States, compared to 32.3 percent in the OECD. This is because all OECD countries, except the United States, levy value-added taxes (VAT) at relatively high rates. State and local sales tax rates in the United States are relatively low by comparison.

Author(s): Cristina Enache

Publication Date: 17 February 2021

Publication Site: Tax Foundation