Link: https://economics21.org/in-search-of-americas-new-debt-consensus

Graphic:

Excerpt:

When economists like Larry Summers and Olivier Blanchard, who normally support more spending, balked at the size of the Biden stimulus plan, supporters of the plan said there was no reason to worry. Clearly markets are not worried about inflation or sustainable debt, just look at low bond prices and modest inflation expectations. They argue if markets aren’t worried, maybe none of us should be.

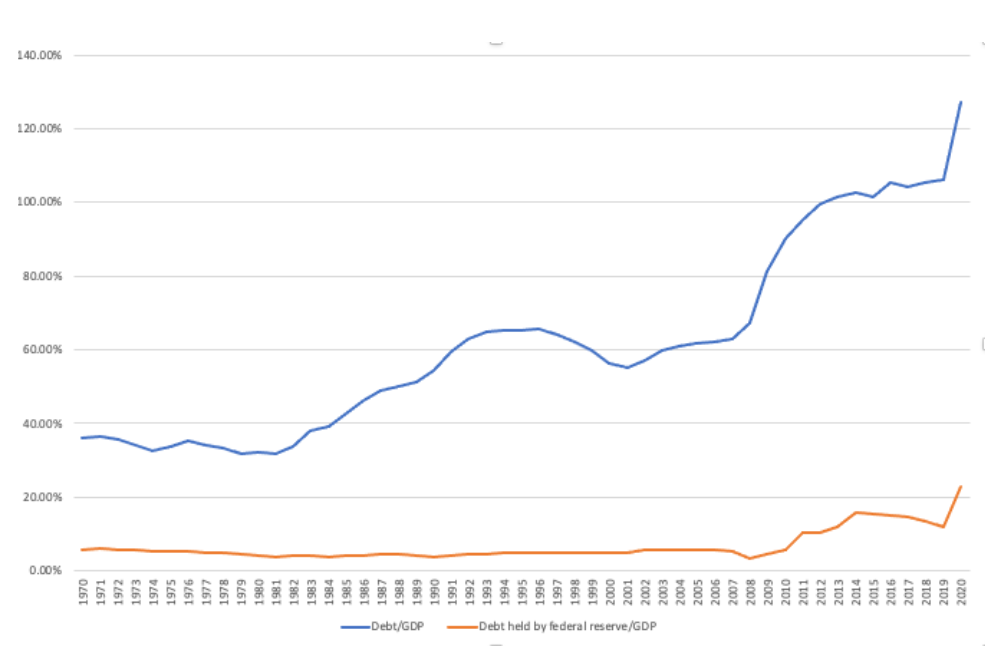

But we are in uncharted territory. The Debt-to-GDP ratio grew exponentially last year to once unthinkable levels, at least for a time of without a major military conflict.1 Piling on another $1.9 trillion (and possibly more later this year) risks higher rates in the future. The more leverage you carry, the less room you have to spend on the next disaster.

So why aren’t markets more worried? Perhaps because for the time being there are not better, safer alternatives. Also, the government has a captive buyer of its debt in the Federal Reserve, whose holdings of US government debt also reached unprecedented levels last year. Debt enthusiasts dismiss worries of an overheating economy by pointing out the Fed could raise rates and stop inflation if it takes off. But that would involve the Fed selling some of its debt and putting even more bonds on the markets, only this time there won’t be a single captive buyer.

Author(s): Allison Schrager

Publication Date: 10 February 2021

Publication Site: E21