Maestas, Nicole, Kathleen J. Mullen and David Powell. 2023. “The Effect of Population Aging on Economic Growth, the Labor Force, and Productivity.” American Economic Journal: Macroeconomics, 15 (2):306-32.

DOI: 10.1257/mac.20190196

Replication package link: https://www.openicpsr.org/openicpsr/project/173781/version/V1/view

Online appendix: https://assets.aeaweb.org/asset-server/files/18416.pdf

Graphic:

Abstract:

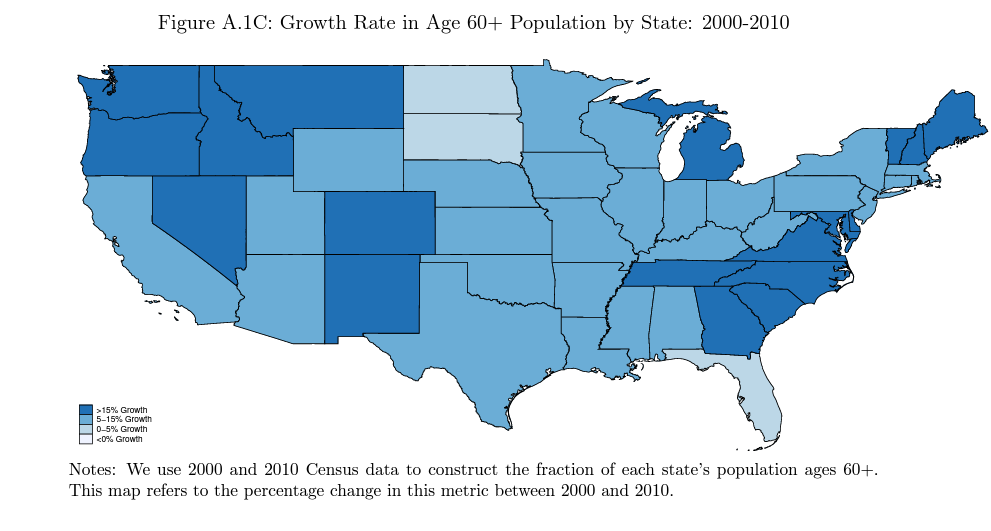

Population aging is expected to slow US economic growth. We use variation in the predetermined component of population aging across states to estimate the impact of aging on growth in GDP per capita for 1980–2010. We find that each 10 percent increase in the fraction of the population age 60+ decreased per capita GDP by 5.5 percent. One-third of the reduction arose from slower employment growth; two-thirds due to slower labor productivity growth. Labor compensation and wages also declined in response. Our estimate implies population aging reduced the growth rate in GDP per capita by 0.3 percentage points per year during 1980–2010.

Author(s): Maestas, Nicole, Kathleen J. Mullen and David Powell

Publication Date: 2023

Publication Site: American Economic Journal: Macroeconomics, AEAweb