Link: https://www.wsj.com/articles/covid-19-endemic-or-not-will-still-make-us-poorer-11642608213

Excerpt:

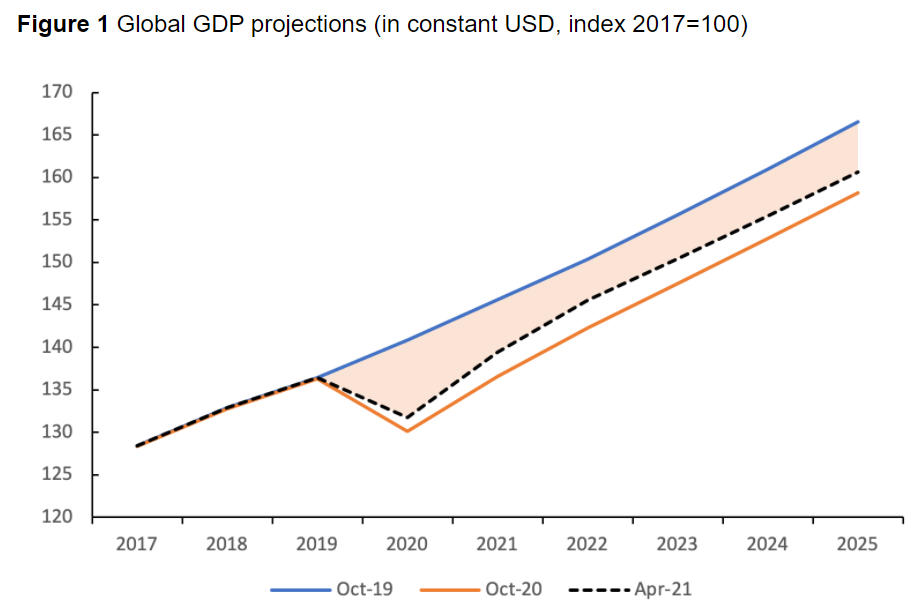

Endemic Covid-19 could thus become a lasting “supply shock” that degrades how much economies can produce, similar to the surge in oil prices in the 1970s. In October, the International Monetary Fund estimated global output this year would still be 3% lower than it had projected in 2019, with Western Europe and Latin America showing much bigger hits than China and Japan, where Covid-19’s toll has been much lower.

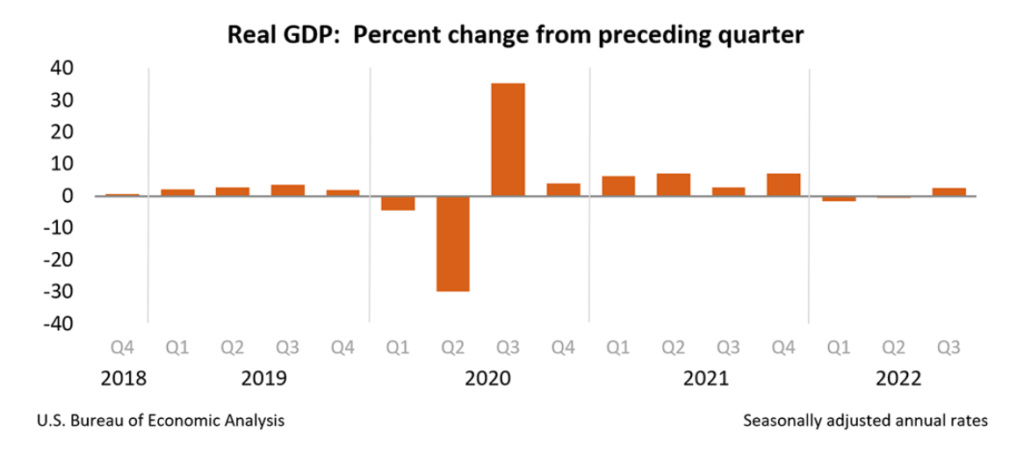

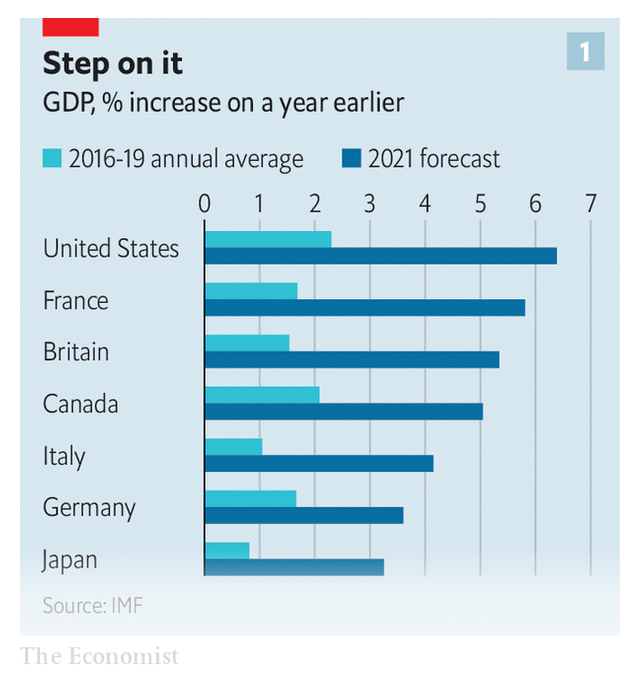

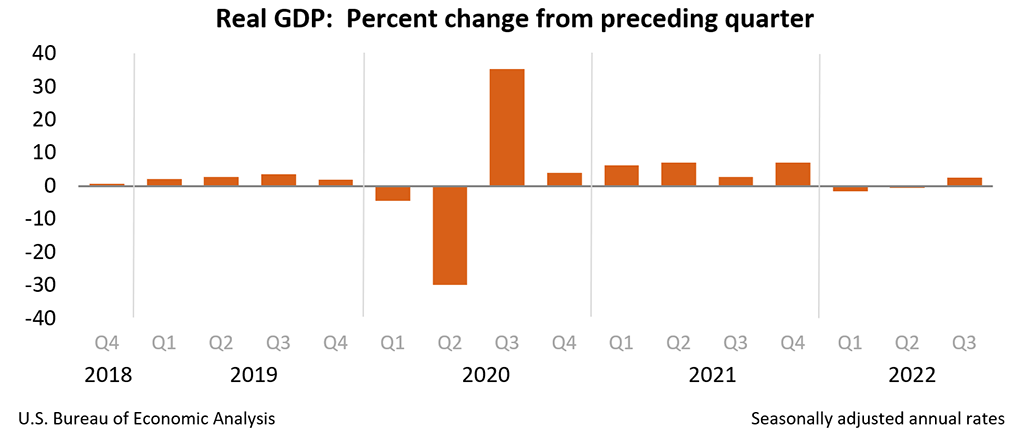

The U.S. is an exception: Output in the last quarter of 2021 was roughly back to its pre-pandemic trend. But the economy, distorted and disrupted by Covid-19, is struggling to sustain this level of output, as the surge in inflation to 7% demonstrates.

Covid-19 might have boosted efficiency in some industries by speeding up digitization and adoption of remote work. Goldman Sachs economists estimate this delivered a 3% to 4% boost to U.S. productivity.

But some of the shift to remote operations is involuntary, and some of the rise in productivity might reflect an overworked workforce. Indeed, the pandemic has left the labor force smaller, sicker and less happy. Absences due to illness among employed workers have averaged 50% higher in the last two years. In early January, nearly 12 million people weren’t working because they were sick with Covid-19, caring for someone with coronavirus, or concerned about getting or spreading the disease, according to a regular Census Bureau survey. The figure hasn’t been below 4 million since June 2020.

In the past year, workers have reported declining satisfaction with their wages and a rising “reservation wage,” that is, how much they would have to be paid to accept a new job, according to the Federal Reserve Bank of New York. This might reflect inflation, changed expectations, or stress due to Covid-19 testing, masks and vaccine mandates, or their absence.

For employers, this makes it much harder to attract the necessary staff. Nursing homes have boosted hourly wages 14% since the start of the pandemic, yet staffing has plummeted 12%, impairing their ability to accept new patients. Such shortages impose a cost that doesn’t show up in gross domestic product.

Author(s): Greg Ip

Publication Date: 19 Jan 2022

Publication Site: WSJ

{kind=link}