Link: https://www.jstor.org/stable/4138424

Graphic:

Abstract:

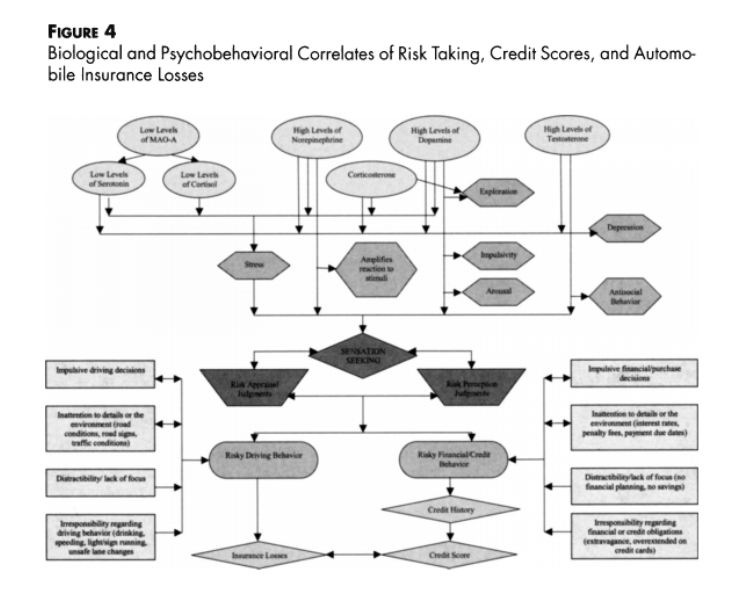

The most important new development in the past two decades in the personal lines of insurance may well be the use of an individual’s credit history as a classification and rating variable to predict losses. However, in spite of its obvious success as an underwriting tool, and the clear actuarial substantiation of a strong association between credit score and insured losses over multiple methods and multiple studies, the use of credit scoring is under attack because there is not an understanding of why there is an association. Through a detailed literature review concerning the biological, psychological, and behavioral attributes of risky automobile drivers and insured losses, and a similar review of the biological, psychological, and behavioral attributes of financial risk takers, we delineate that basic chemical and psychobehavioral characteristics (e.g., a sensation-seeking personality type) are common to individuals exhibiting both higher insured automobile loss costs and poorer credit scores, and thus provide a connection which can be used to understand why credit scoring works. Credit scoring can give information distinct from standard actuarial variables concerning an individual’s biopsychological makeup, which then yields useful underwriting information about how they will react in creating risk of insured automobile losses.

Author(s): Patrick L. Brockett and Linda L. Golden

Publication Date: originally 2007

Publication Site: jstor, The Journal of Risk and Insurance

Cite: Brockett, Patrick L., and Linda L. Golden. “Biological and Psychobehavioral Correlates of Credit Scores and Automobile Insurance Losses: Toward an Explication of Why Credit Scoring Works.” The Journal of Risk and Insurance, vol. 74, no. 1, 2007, pp. 23–63. JSTOR, http://www.jstor.org/stable/4138424. Accessed 22 May 2022.