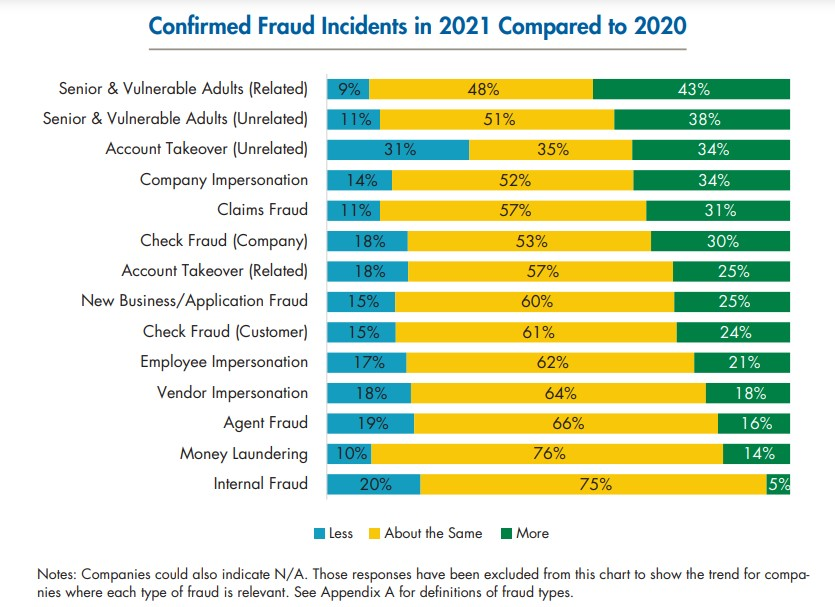

More than a third (34%) of companies reported increases in account takeover attempts in 2021 as compared to the previous year, according to LIMRA. Account takeovers occur when someone takes ownership of an online account without the owner’s knowledge, often with stolen credentials. In addition to account takeovers attempts, 34% of companies saw increases in company impersonation and 31% had increases in claims fraud.

A LIMRA report showed that fraud incidents increased in 2021 in all but two categories of fraud. (Please note that fraud “incidents” shown in the chart below are attempts and do not indicate that the account takeover attempts were successful.)

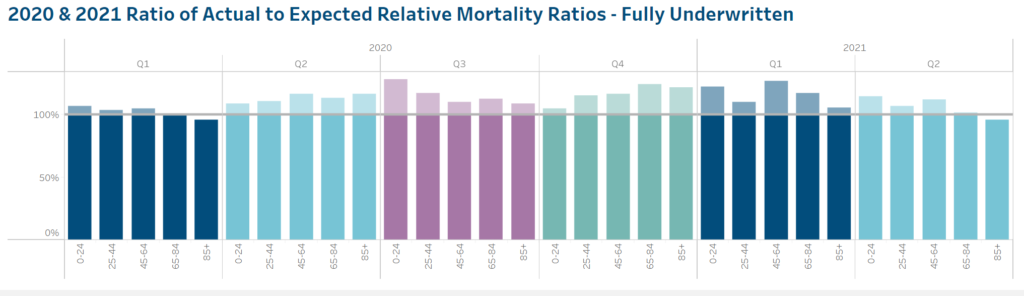

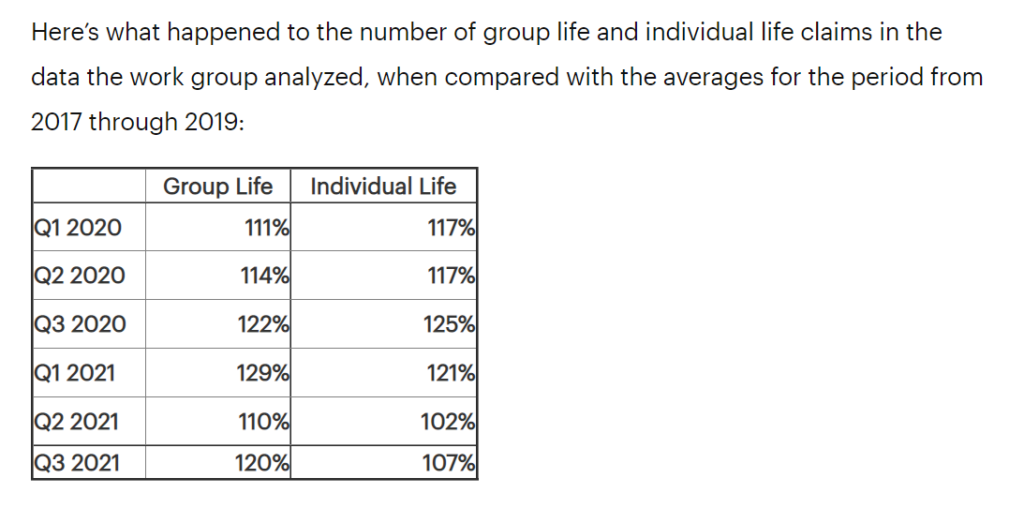

LIMRA, Reinsurance Group of America (RGA), the Society of Actuaries (SOA) Research Institute, and TAI have collaborated on an ongoing effort to analyze the impact of COVID-19 on the individual life insurance industry’s mortality experience and share the emerging results with the insurance industry and the public. The Individual Life COVID-19 Project Work Group (Work Group) was formed as a collaboration of LIMRA, RGA, the SOA Research Institute, and TAI to design, implement, and create the study and to produce and distribute a variety of analyses. This report is the fifth public release from this collaboration and contains the results of the study of excess mortality for individual life insurance to include the second quarter of 2021. Data from 31 companies representing approximately 72% of the industry face amount in force have been included in the analysis in this report. A total of 3.0 million death claims from individual life policies from 2015 through June 30, 2021 make up the basis of the analysis.

Highlights for the 2nd Quarter

The second quarter of 2021 showed a significant realignment of the actual to expected relative mortality ratios, across many different cuts of the data.

It is worth noting that the third quarter 2021 results will likely not be as favorable due to the impact of the COVID-19 Delta variant whose impact first started in July 2021 and peaked around mid- September

All age groups improved in the second quarter compared to the first quarter of 2021, but the improvement was more dramatic in the older ages. While the three age groups shown under age 65 were still significantly over the trend established by 2015-2019, the age 65-84 group was within the 95% confidence bands and the age 85+ group was significantly better than the 2015-2019 trend (p < 0.05).

Whereas the pandemic experience so far had showed substantial variations across different regions, this appears to have moderated during the 2nd quarter of 2022.

Author(s): Individual Life COVID-19 Project Work Group, SOA

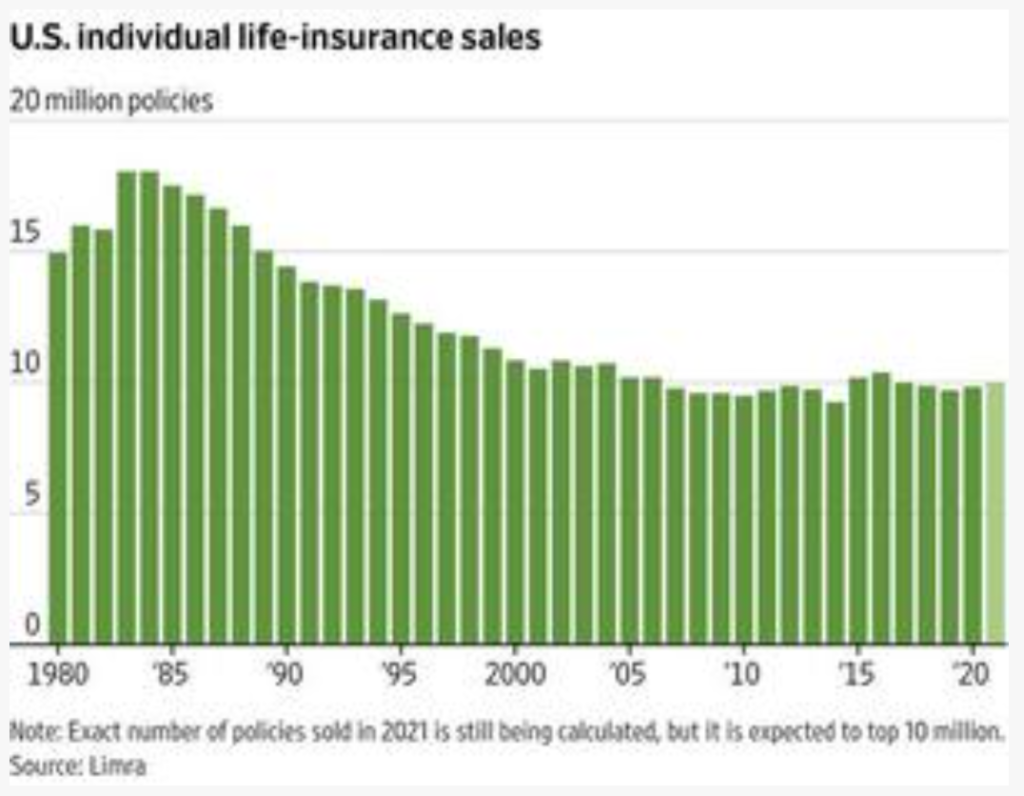

Americans went on a buying spree for life insurance in 2021, driven by concerns of death from the coronavirus pandemic.

Premium volume for new individual life-insurance policies surged 20% from 2020, while the number of policies issued rose 5%, the biggest year-over-year percentage gains since the 1980s, according to industry-funded research firm Limra.

“As we zero in on one million Americans who tragically lost their lives, it’s not a surprise that people are thinking about their own mortality and the impact on loved ones if anything were to happen to them,” said David Levenson, Limra’s chief executive.

The exact number of policies sold is still being calculated, but it is expected to top 10 million, Limra said. That milestone was last crossed in 2016. In 2020, an estimated 9.83 million policies were sold, up 1.7% from 2019.

To help participants grow their balances, employer-sponsored DC plans are also incorporating behavioral finance concepts into plan design and architecture by automating systems.

“Now we see automatic enrollment, we see target dates, we see managed accounts that are becoming more complex and having more options as baked into defined contribution plans,” says Deb Dupont, assistant vice president for retirement plans research at the LIMRA Secure Retirement Institute. “All of these things make it much easier and in fact [a] more passive decision on the part of the participant.”

Legislation, including 2019’s Setting Up Every Community for Retirement Act, has also eased plan sponsors’ responsibilities when selecting an insurer to offer annuitization options for participants’ decumulation stage. The safe harbor has prompted sponsors to increasingly build lifetime income options into their plans to provide retirement income certainty. And prior to the SECURE Act, the Pension Protection Act of 2006 led to widespread adoption of qualified default investment alternatives, including target-date funds, which helped DC plans incorporate ideas from DB plans, Dupont adds.