When planning for retirement, it’s important to consider all the risks, and one consideration that individuals often overlook is “longevity risk.” Longevity risk refers to the chance a person could outlive their savings. Understanding longevity and reasonably estimating the probabilities of living to various advanced ages and the risk of outliving resources are important for planning a secure retirement.

As a result of healthy lifestyles, medical advancements and scientific discoveries, it has become much more common for people these days to live into their 80s and 90s — or even their 100s! In fact, Pew Research Center writes that, according to estimates by the U.S. Census Bureau, there are about 101,000 centenarians in the U.S. in 2024, and this population could quadruple to about 422,000 in 2054.

While a long life is something most people desire, it requires planning for a longer retirement than in the past. For example, if a worker retires at 67, planning for a 20-year retirement may not be enough, and if they live to be in their 90s, or even past 100, they could outlive their savings or end up with fewer assets to leave their heirs.

PEK: Your research reveals a conundrum when comparing a variable annuity with systematic withdrawals from investment accounts (assuming similar investment returns): the annuity will generally outperform. How do we convey this very basic equivalency to our clients?

BG: In my experience, I’ve seen that when some people get to retirement, they may have upwards of a half a million dollars in their accounts. Financial planners owe their clients more than just plans to help them accumulate assets and some well-wishes. Most people do not understand how to generate income from their savings that will last the rest of their lives.

Savings are exposed to market risk that can erode account balances before or in retirement, as we saw in The Great Recession of 2009 and the economic contraction during the coronavirus pandemic. And fifty percent of the population can expect to live beyond the average life expectancy in retirement, exposing them to longevity risk.

The practical reality is that most individuals cannot insulate themselves from risk on their own. Annuitizing a portion of a portfolio’s assets can help mitigate these issues.

PEK: You demonstrate that delaying the start of an annuity by five years may cost 5% in future income, which delaying ten years may cost 15%. Please talk about the time factor and the cost of delay.

BG: The concept is based on something called “mortality credits.” When buying an annuity, you join an annuity pool. Every time someone dies early (before he spent all the money he contributed) the leftover money stays in the pool and is shared by all those still in the pool. The money becomes a mortality ‘credit’ for those who did not die. These mortality credits allow the former to get lifetime income. They start adding value from the day someone enters the pool. Those who purchase the annuity at a later time were not in that pool and do not get that credit. Purchasers only receive mortality credits for those people who died after the purchasers joined the pool. Lower mortality credit means lower lifetime income. Mortality credits have value by adding to income.

….

PEK: Likewise, how real is the prospect of outliving one’s assets today?

BG: It’s very real. Data from EBRI indicates that about 40% of Americans face the risk of running out of money in retirement.

Now, not many people continuously spend and then one day look at their account and say, “Oh no! There is no money left!” But well before that day, they will start adjusting their spending downward so as to make sure they don’t outlive their money. And some have to make drastic and painful decisions, like choosing between paying for rent or healthcare; to pay for the electric bill or for medicine. Some retirees will even take half the dosage of their prescribed medicine to conserve it. It may even require that retirees move in with a child rather than live in poverty. In certain family dynamics, living with elderly parents is expected, but it may not be ideal for many.

Any predictions are by their nature uncertain, yet a longevity modelling firm has forecasted that both candidates are likely to live well beyond the end of the next presidency in 2029. According to Club Vita, actuarial data suggests both men could have more than another decade ahead of them.

The company, which offers analytical services to insurers, said its US model suggested Biden has a life expectancy of another 11 years, taking him to 91. Trump has 14 more years to look forward to, per the model, meaning he would die at 90.

The model’s inputs include affluence, marital status, and employment. These key demographics for both Biden and Trump put them in the same favourable categories for the main factors, including addresses in the top category for life expectancy: the analysts used Trump’s Palm Beach address and Biden’s Delaware home.

Erik Pickett, a New Jersey-based actuary for Club Vita, said a wide range of factors could prove its model wrong, from whether the candidates “are in significantly different health to the average of someone with the same characteristics” to the fact that presidents have “access to higher quality medical treatments” than the typical American.

Author(s): Ian Smith in London and David Crow in New York

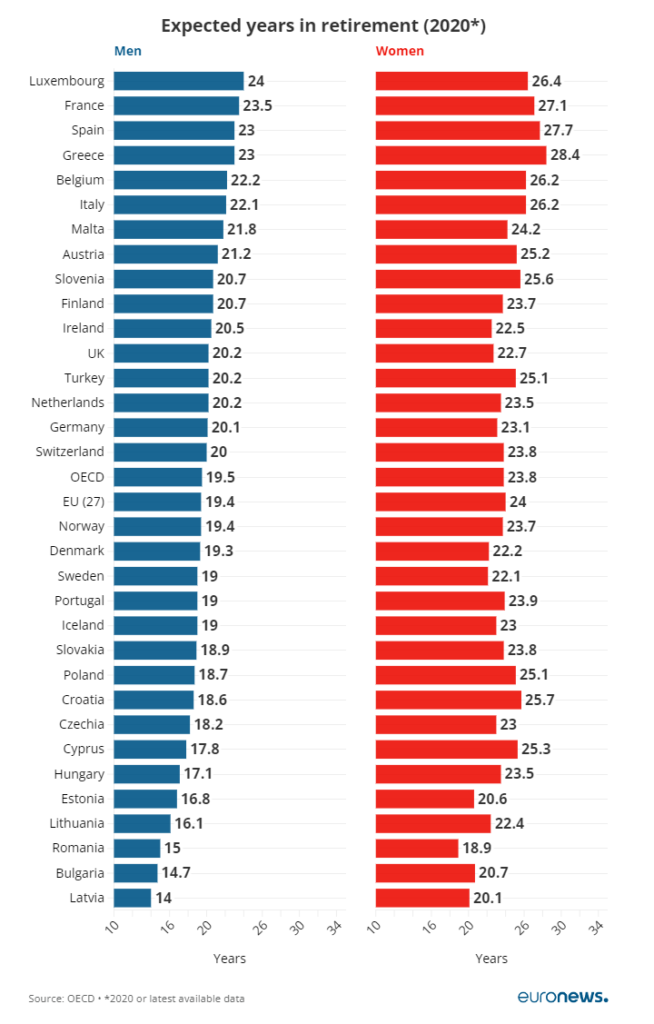

The gap between women and men in expected years of retirement varies from 2.0 years in Ireland to 7.5 years in Cyprus.

By 2020, European women typically can expect to live 4.3 years more than men after they exit the labour market.

While the EU average is 4.6 years, in France, the gender gap stands in favour of women by a total of 3.6 years.

Interestingly, life expectancy in retirement for both highly varies across Europe. For men, it ranges from 14 years in Latvia to 24 years in Luxembourg.

For women, it varies from 18.9 years in Latvia to 28.4 years in Greece. Women are expected to have 26 years or more to spend while retired in Belgium, France, Greece, Italy, Luxembourg and Spain.

Demographers and actuaries make the following distinction between life expectancy and longevity: Life expectancy refers to the average number of years someone will live from a given age, whereas longevity refers to how long he or she might live if everything goes well, typically expressed as the probability of living beyond a certain age such as 85, 90 or even 100.

A growing body of evidence shows that many people are ignorant of their so-called longevity risk—the probability of living a very long time—and the complications that presents.

….

Drs. Hurwitz and Mitchell note that retirement calculators provide information about average life expectancy, but not longevity. They have found that about five times as many Census Bureau publications relate to life expectancy as longevity. Thus, people who have planned appropriately for their life expectancy might miss how likely they are to live longer.

….

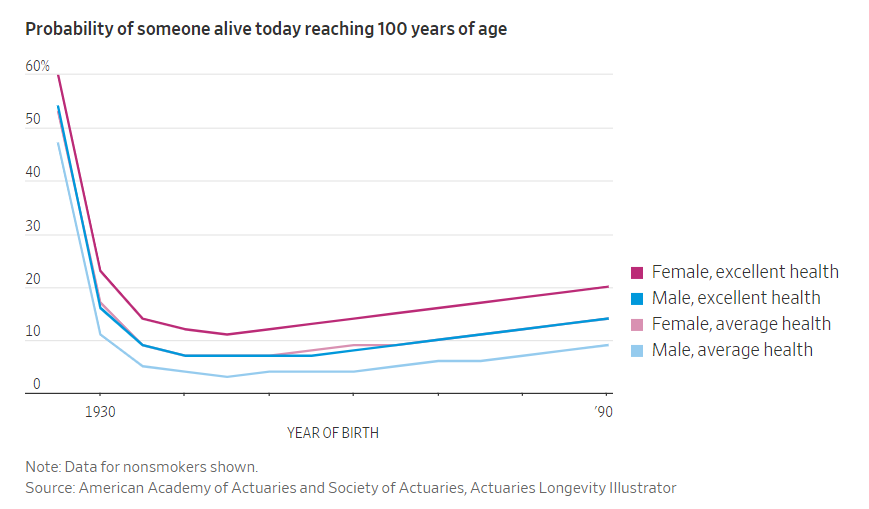

People can look up their longevity risk with an online Longevity Illustrator maintained by the American Academy of Actuaries and Society of Actuaries, based off the latest mortality data from the Social Security Administration.

“The human genome – the full set of genetic instructions for a human being – is made up of 20,000 instructions called genes.

But add all the genes in our microbiome together and the figure comes out between two and 20 million microbial genes.

Prof Sarkis Mazmanian, a microbiologist from Caltech, argues: “We don’t have just one genome, the genes of our microbiome present essentially a second genome which augment the activity of our own.

“What makes us human is, in my opinion, the combination of our own DNA, plus the DNA of our gut microbes.”

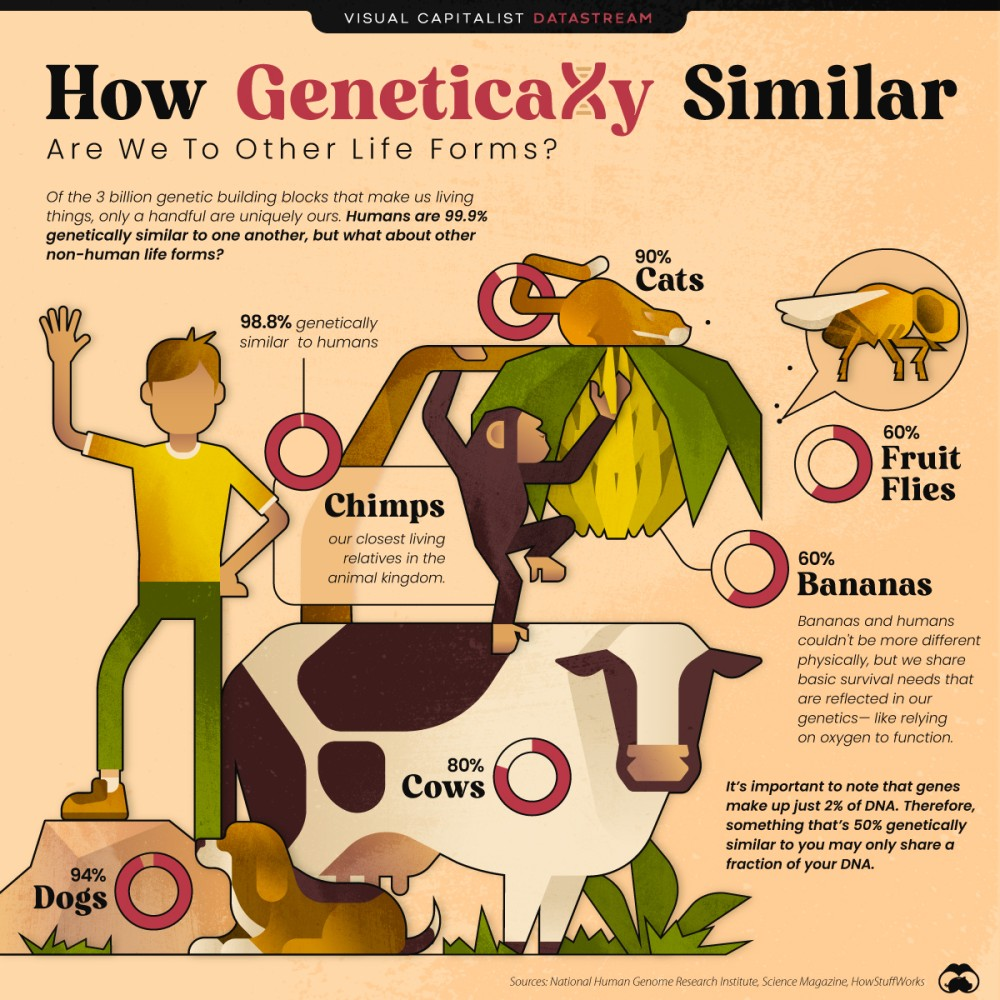

2- We share DNA with Bananas and Copied Viral DNA: Our closest genetic relative is the chimp, but we are connected to dogs and cats and even fruit flies and yes, bananas.

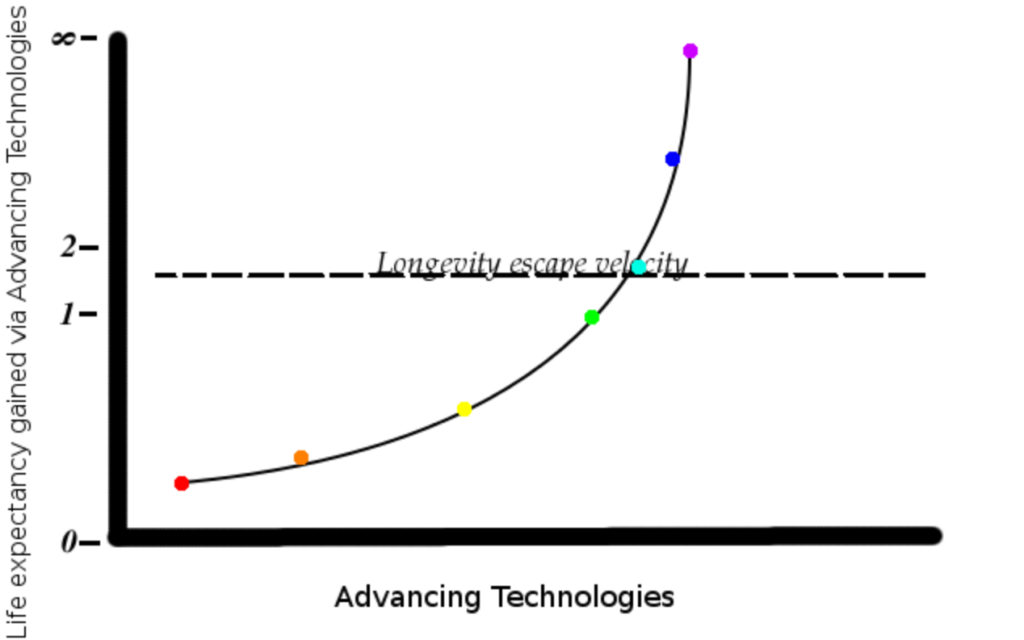

A new series called “Let’s Talk Longevity” kicked of with a conversation (sort of debate) between Drs. Aubrey De Grey and Charles Brenner, centering around the possibility of achieving “Longevity Escape Velocity” (LEV).

De Grey’s position imagines the possibility (50% chance in next few decades) of a “Methusalarity” a moment in which we begin to reverse some aspects of “aging” , primarily via “damage repair” at such a rate that we are able to repair damage in the body as fast as or faster than that damage is occurring. More concretely defined, it can be thought of as 20-30 years more of expected healthy life at age 60 when anti aging therapies begin.

David Sinclair – Harvard professor, celebrity biologist, and author of Lifespan – thinks solving aging will be easy. “Aging is going to be remarkably easy to tackle. Easier than cancer” are his exact words, which is maybe less encouraging than he thinks.

There are lots of ways that solving aging could be hard. What if humans worked like cars? To restore an old car, you need to fiddle with hundreds of little parts, individually fixing everything from engine parts to chipping paint. Fixing humans to such a standard would be way beyond current technology.

Or what if the DNA damage theory of aging was true? This says that as cells divide (or experience normal wear and tear) they don’t copy their DNA exactly correctly. As you grow older, more and more errors creep in, and your cells become worse and worse at their jobs. If this were true, there’s not much to do either: you’d have to correct the DNA in every cell in the body (using what template? even if you’d saved a copy of your DNA from childhood, how do you get it into all 30 trillion cells?) This is another nonstarter.

Sinclair’s own theory offers a simpler option. He starts with a puzzling observation: babies are very young [citation needed]. If a 70 year old man marries a 40 year old woman and has a baby, that baby will start off at zero years old, just like everyone else. Even more interesting, if you clone a 70 year old man, the clone start at zero years old.

….

So Sinclair thinks aging is epigenetic damage. As time goes on, cells lose or garble the epigenetic markers telling them what cells to be. Kidney cells go from definitely-kidney-cells to mostly kidney cells but also a little lung cell and maybe some heart cell in there too. It’s hard to run a kidney off of cells that aren’t entirely sure whether they’re supposed to be kidney cells or something else, and so your kidneys (and all your other organs) break down as you age. He doesn’t come out and say this is literally 100% of aging. But everyone else thinks aging is probably a combination of many complicated processes, and I think Sinclair thinks it’s mostly epigenetic damage and then a few other odds and ends that matter much less.

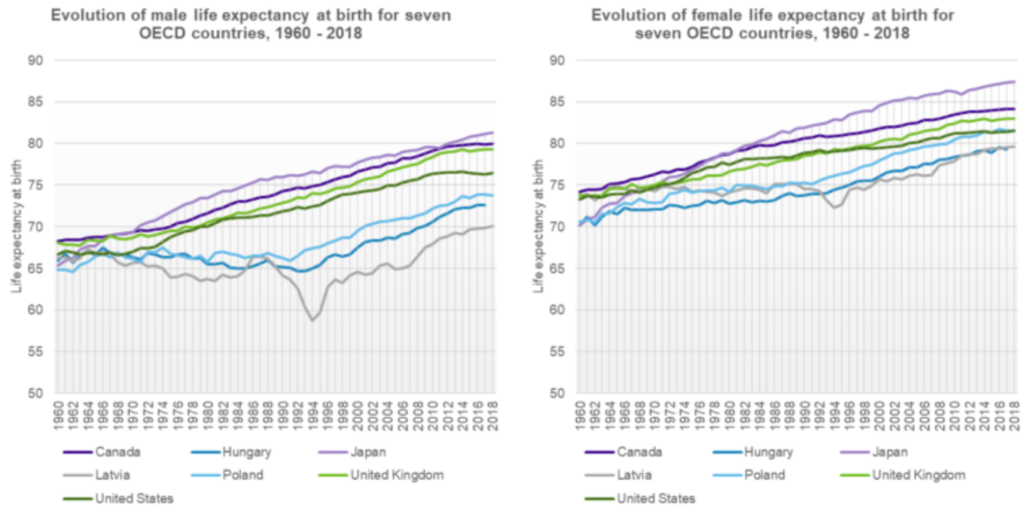

Illustrated below is the evolution of life expectancy at birth for seven Organization for Economic Co-operation and Development (OECD) countries: Canada, Hungary, Japan, Latvia, Poland, the United Kingdom, and the United States. Across the seven countries, male life expectancy at birth ranged from 64.8 years to 68.2 years in 1960, and 69.8 years to 81.1 years in 2017, demonstrating an increase in the inequality of life expectancy of almost eight years between these countries over the period. For females, the increase was approximately four years. The inequality in life expectancy is more apparent and unsettling if we consider, for example, developing countries in Africa, averaging a life expectancy of around 63 years in 2019.

….

Altogether, I believe greater democratization of longevity is achievable with the adoption of health technologies, while ensuring they are accessible and affordable. I am hopeful but I see several challenges ahead. Such a reality will be reliant on governments, health care professionals, and patients’ acceptance and reliance on what the future of health holds. It will also require global partnerships to build out ecosystems that will facilitate inclusive innovation.

Moshe Milevsky claims that someone could be up to 20 years younger biologically than their chronological age, and that biological age is a much be a better way of determining a person’s longevity. If this is true, is there a way that organizations that specialize in longevity and/or mortality and that use mathematical calculations in order to determine risk could use biological age instead of chronological age to predict future health and longevity?

…..

There are two methods used to calculate biological age, coined by Milevsky as the “living” methodology or the “dying” methodology a.k.a. the mortality-adjusted approach.

Both methods begin with the collection of data. A researcher would first gather data from a large group of people at a wide range of ages, collecting biological samples and measurements in order to record various physiological and molecular variables (such as heart rate, blood pressure, mutations of DNA, or the presence of certain proteins in the blood). Researchers may also collect data on variables that they believe will be correlated with enhancement or deterioration of a person’s physiological condition, such as their wealth, occupation or even their appearance or number of Facebook friends!

The estimated number of people aged 65 or older in Japan stood at a record high of 36.4 million as of Wednesday, an increase of 220,000 from a year before, the internal affairs ministry said Sunday.

The share of those aged adults in the nation’s total population rose to a record 29.1%, the highest among 201 countries and regions across the world.

Older men totaled 15.83 million, or 26% of the total male population. There were 20.57 million elderly women, or 32% of the female population.

The ministry released the data ahead of Respect for the Aged Day on Monday, a national holiday.

In Japan, the share of aged people has been rising since 1950. The figure is expected to rise to as high as 35.3% in 2040 when the so-called second baby-boomer generation, or people born in the early 1970s, reaches the age of 65 or older, according to the National Institute of Population and Social Security Research.

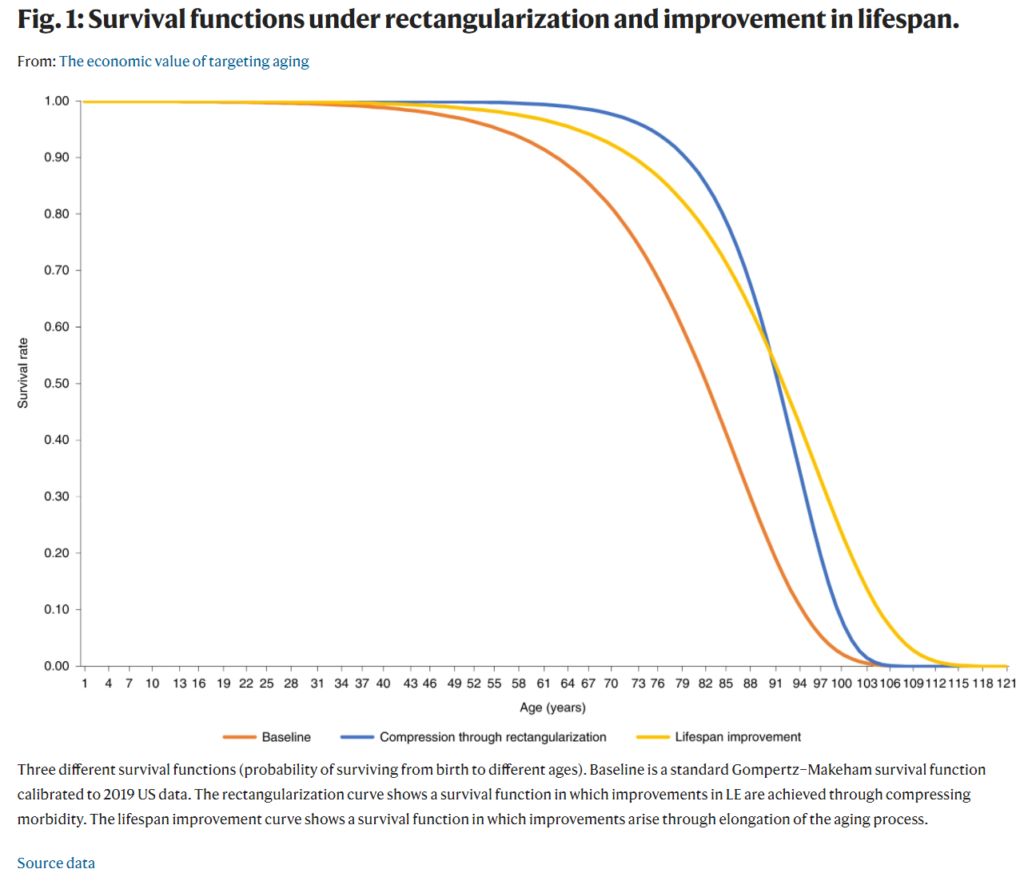

Developments in life expectancy and the growing emphasis on biological and ‘healthy’ aging raise a number of important questions for health scientists and economists alike. Is it preferable to make lives healthier by compressing morbidity, or longer by extending life? What are the gains from targeting aging itself compared to efforts to eradicate specific diseases? Here we analyze existing data to evaluate the economic value of increases in life expectancy, improvements in health and treatments that target aging. We show that a compression of morbidity that improves health is more valuable than further increases in life expectancy, and that targeting aging offers potentially larger economic gains than eradicating individual diseases. We show that a slowdown in aging that increases life expectancy by 1 year is worth US$38 trillion, and by 10 years, US$367 trillion. Ultimately, the more progress that is made in improving how we age, the greater the value of further improvements.

Author(s): Andrew J. Scott, Martin Ellison, David A. Sinclair