Link: https://www.bostonglobe.com/2023/06/19/opinion/mbta-retirement-fund-finances/

Excerpt:

The MBTA Retirement Fund is going over a cliff, and the reasons why are well known. But neither the T nor its unions are in a hurry to do anything about it.

The new MBTA Retirement Fund Actuarial Valuation Report shows the fund’s balance as of Dec. 31, 2022, was $1.62 billion — about $300 million less than what it was just 12 months earlier. Its liability — the amount it will owe current and future T retirees — is over $3.1 billion, meaning the fund is about 51 percent funded. In 2006, it was 94 percent funded. A “death spiral” generally accelerates when retirement system funding dips below 50 percent.

In April, the Pioneer Public Interest Law Center got the MBTA to hand over an August 2022 arbitration decision regarding a pension dispute between the T and its biggest union. It contained a critical win for the authority: Arbitrator Elizabeth Neumeier decided that most employees would have to work until age 65 to earn a full pension, saving the MBTA at least $12 million annually.

But the Carmen’s Union sued to invalidate that portion of the decision, and the parties returned to the bargaining table. The new pension agreement they hammered out doesn’t include the historic retirement age victory; T management negotiated it away.

….

As of Dec. 31, 2022, 5,555 active employees paid into the fund, but 6,783 retirees collected from it. The biggest reason for the mismatch is the age at which T employees retire. Those hired before December 2012 can retire with a full pension after 23 years of service, regardless of age. Those hired after December 2012 can retire with a full pension at age 55 after 25 years.

The arbitrator finally gave the MBTA the win it so desperately needed, and T management promptly gave it back. Many MBTA managers have long opposed changing the age at which employees can earn a full pension, fearing the reaction of T unions.

….

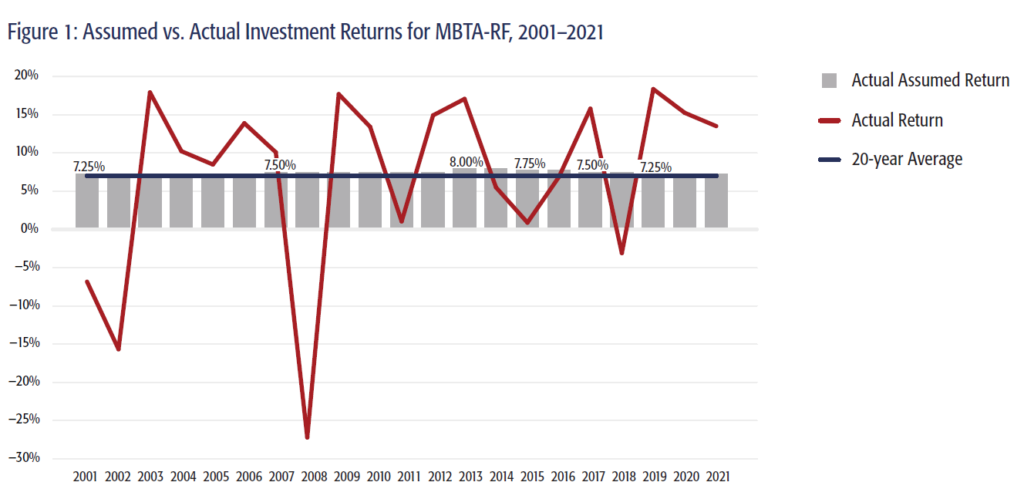

Hard as it may be to believe, the T retirement fund’s financial outlook is even worse than it appears. Financial projections assume the fund’s assets will earn 7.25 percent annually. Over time, actual returns have been more like 4 percent to 7 percent.

These misleading projections are based on other faulty assumptions. In her 2022 decision, Neumeier refused the MBTA’s request to use newer actuarial tables, ruling that changing would be costly and that there was no compelling reason to update the tables. The ones in place are from 1989 — so old that they assume all T employees are men. Since women tend to live longer, the tables materially understate the retirement fund liability.

Author(s): Mark T. Williams, Charles Chieppo

Publication Date: 19 Jun 2023

Publication Site: Boston Globe