Link: https://burypensions.wordpress.com/2022/04/26/nj-opeb-update-2020/

Graphic:

Excerpt:

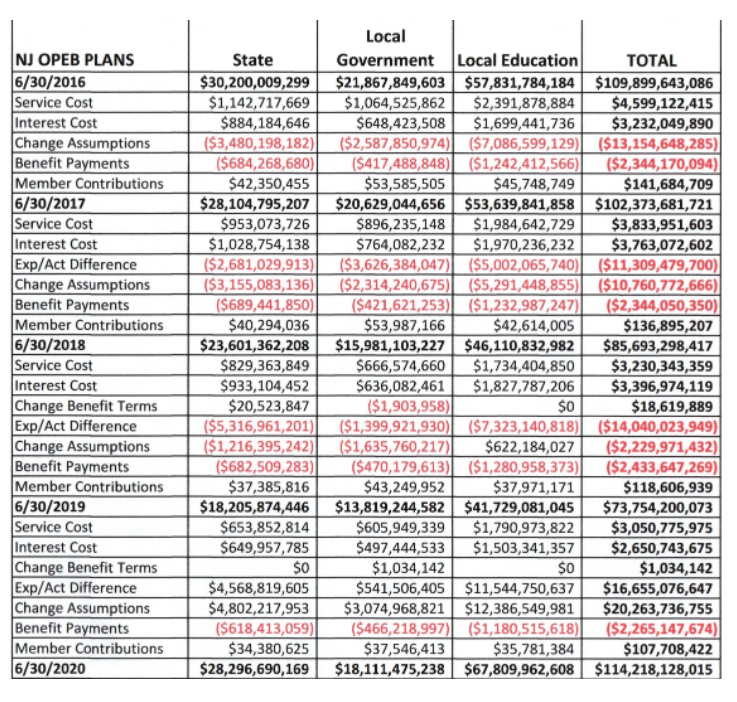

There are three separate reports for state, local government, and local education which throw a lot of distracting numbers at you but, when added up, show that after an amazing 1/3rd reduction in the total OPEB Liability (from $110 billion as of 6/30/16 to under $74 billion as of 6/30/19) the state actuaries sharply reversed course.

Author(s): John Bury

Publication Date: 26 Apr 2022

Publication Site: Burypensions