Graphic:

Excerpt:

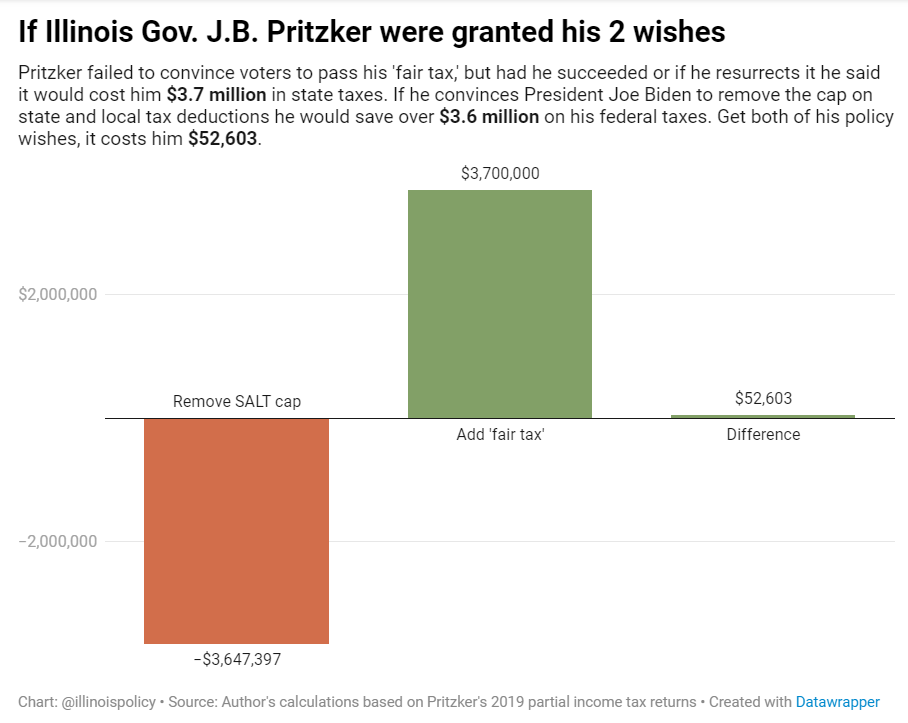

Of course, no one can know the true extent to which Pritzker has been able to reduce his tax bills through loopholes and carve-outs over the years, because he refuses to release his full tax returns. In recent years it has been revealed Pritzker went to great lengths to avoid paying taxes, removing toilets from his Gold Coast mansion to skimp on his property tax bill by $331,000 and establishing shell corporations in the Bahamas in a likely attempt to avoid U.S. income taxes. The toilet ploy earned him a federal investigation.

The letter, which pushes for tax reforms that would almost exclusively benefit the wealthy, comes less than six months after Pritzker’s progressive income tax amendment was rejected by voters and is a significant departure from his previous stance on taxation. In the letter, Pritzker claims the cap hurts middle-class taxpayers and is “untenable” during these dire economic times. Because the data is clear on who directly benefits from the SALT deduction, one can only assume the governor is implying higher taxes on the wealthy also hurt Americans with lower incomes.

That is precisely the argument opponents of the “fair tax” made after the governor first unveiled his tax-the-rich scheme in 2019.

Author(s): Orphe Divounguy, Bryce Hill

Publication Date: 23 April 2021

Publication Site: Illinois Policy Institute