Graphic:

Excerpt:

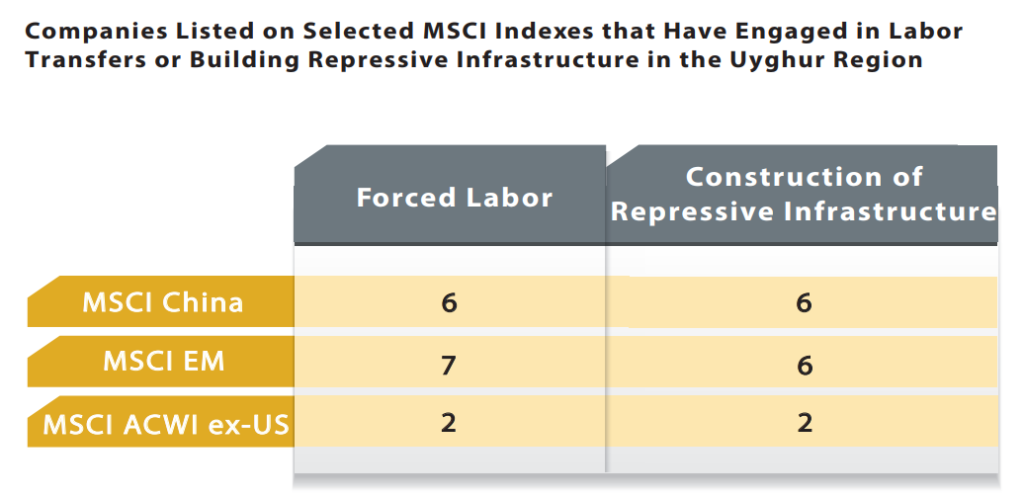

A new report by Hong Kong Watch have found that a number of pension funds may be passively invested in at least 13 China based companies where there is credible evidence of involvement in Uyghur forced labour programs and construction of internment camps in Xinjiang.

As part of the report, Hong Kong Watch found that major asset managers are exposed passively to these companies as a result of their inclusion on Morgan Stanley Capital International’s Emerging Markets Index, China Index and All World Index ex-USA.

….

Commenting on the release of the report, Johnny Patterson, co-founder and a research fellow at Hong Kong Watch, said:

“13 companies on MSCI’s emerging markets index are either known to have directly used forced labour through China’s forcible transfer of Uyghurs, or been involved in the construction of camps. Given this Index is the most widely tracked Emerging Markets index in the world, it raises serious questions about how seriously international financial institutions take their international human rights obligations or the ‘S’ in ESG.

Our view is that firms known to use modern slavery or known to be complicit in crimes against humanity should be classed alongside tobacco as ‘sin stocks’, or stocks which investors do not touch. Governments have a duty to signal which firms are unacceptable, but international financial institutions must also be doing their full due diligence. It is unacceptable that enormous amounts of the money of ordinary pensioners and retail investors is being passively channelled into firms that are known to use forced labour.”

Publication Date: 5 Dec 2022

Publication Site: Hong Kong Watch