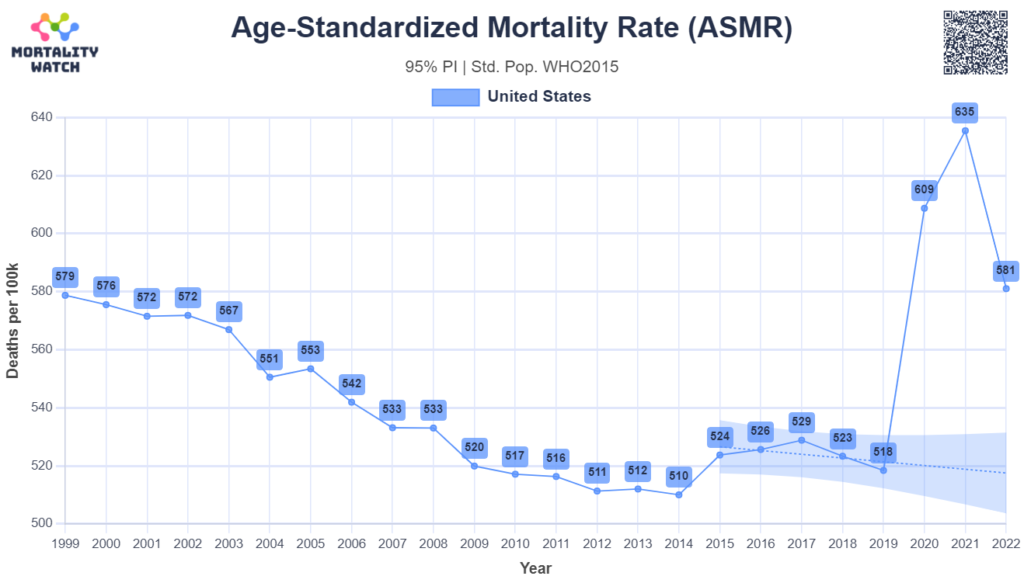

Graphic:

substack: https://usmortality.substack.com/

Publication Date: accessed 23 Apr 2023

Publication Site: Mortality Watch

All about risk

Graphic:

substack: https://usmortality.substack.com/

Publication Date: accessed 23 Apr 2023

Publication Site: Mortality Watch

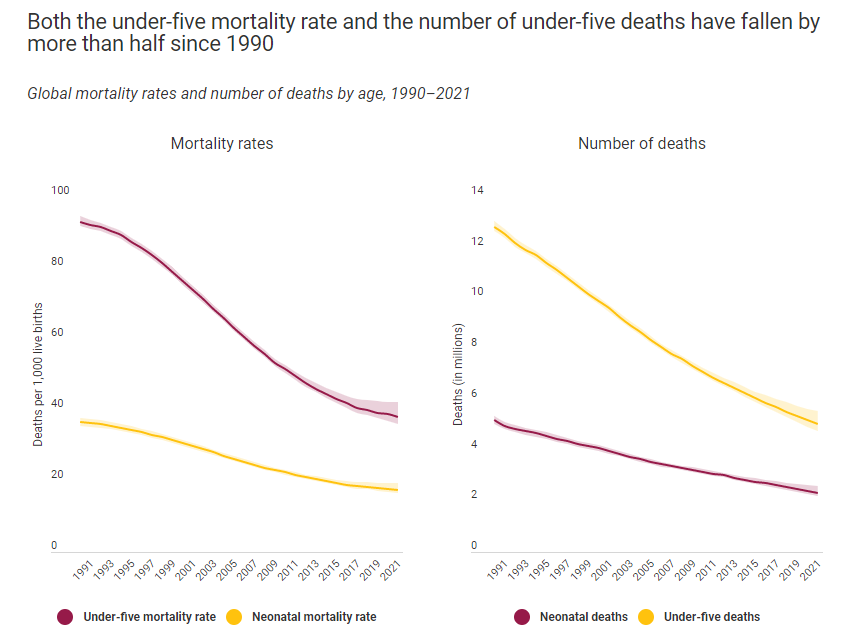

Link: https://data.unicef.org/topic/child-survival/under-five-mortality/

Graphic:

Excerpt:

The world made remarkable progress in child survival in the past three decades, and millions of children have better survival chances than in 1990—1 in 26 children died before reaching age five in 2021, compared to 1 in 11 in 1990. Moreover, progress in reducing child mortality rates has been accelerated in the 2000s period compared with the 1990s, with the annual rate of reduction in the global under-five mortality rate increasing from 1.8 per cent in 1990s to 4.0 per cent for 2000-2009 and 2.7 per cent for 2010-2021.

The under-five mortality rate refers to the probability a newborn would die before reaching exactly 5 years of age, expressed per 1,000 live births. In 2021, 5.0 million children under 5 years of age died. Globally, infectious diseases, including pneumonia, diarrhoea and malaria, remain a leading cause of under-five deaths, along with preterm birth and intrapartum-related complications.

The global under-five mortality rate declined by 59 per cent, from 93 deaths per 1,000 live births in 1990 to 38 in 2021. Despite this considerable progress, improving child survival remains a matter of urgent concern. In 2021 alone, roughly 13,800 under-five deaths occurred every day, an intolerably high number of largely preventable child deaths.

Publication Date: January 2023, accessed 21 March 2023

Publication Site: UNICEF

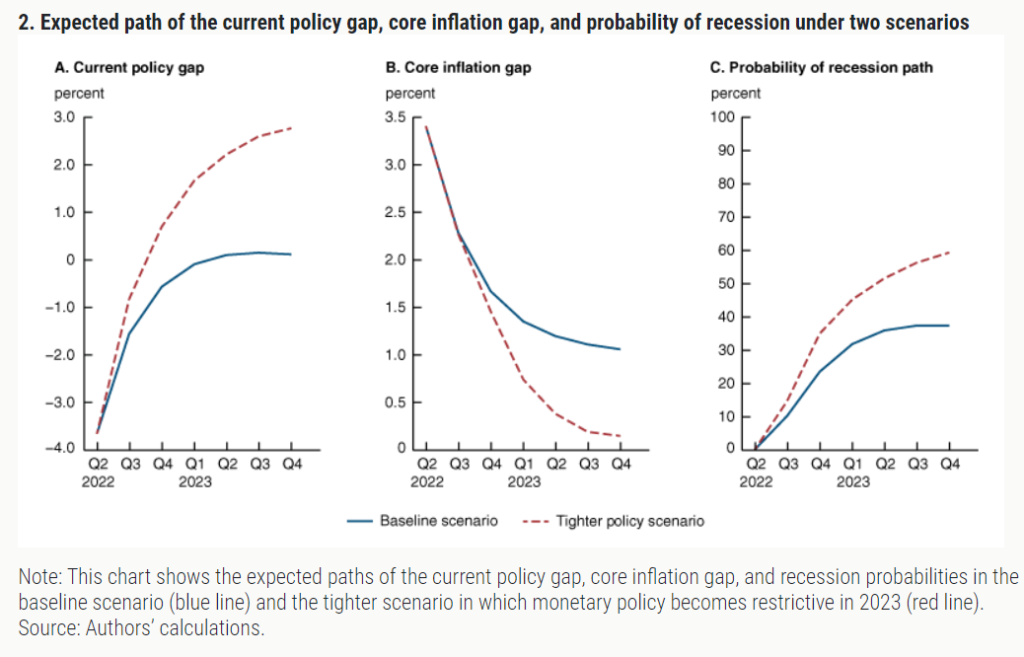

Link: https://www.chicagofed.org/publications/chicago-fed-letter/2022/469

Graphic:

Excerpt:

We simulate future realizations of the policy gap and the slope of inflation forecasts from the 2022:Q2 initial conditions through 2023:Q4 using the ABC model. We then evaluate the recession probability predicted by our preferred probit model for each of these simulated paths. Through this analysis, we show that future inflation outcomes and the odds of a recession depend critically on both the pace of removal of monetary policy accommodation and on how restrictive the monetary policy stance will become over the medium term. In particular, we highlight two scenarios: The first one, which we refer to as the “baseline case,” reflects the ABC model forecasts or, equivalently, the average of all simulated paths. The second one, which we label the “tighter-policy scenario,” is characterized by a faster removal of monetary policy accommodation; it is identified by the average of the simulated paths in which policy becomes restrictive by the end of 2022.11

1. Baseline case: As of early June 2022, the ABC model predicts that nominal and real yields will rise over the next six quarters, the current policy gap will narrow and become mildly restrictive in mid-2023, while core inflation will fall and remain around one percentage point above its model-implied longer-run expectations through 2023 (figure 2, blue lines in panels A and B). The expected tightening of the policy gap and a downward-sloping expected inflation path combine to increase the one-year-ahead recession probability to about 35% by 2023 (figure 2, blue line panel C). Such a level is comparable to the one estimated ahead of the 1994 monetary policy tightening cycle that was followed by a soft-landing scenario.

2. Tighter-policy scenario: In this alternative scenario, monetary policy becomes more restrictive than in the baseline case, in that the policy gap is markedly restrictive over 2023. In this case we find that core inflation declines more rapidly than under the baseline, closing the gap with its model-implied longer-run expectations almost completely by the end of 2023. By that date, in this scenario the likelihood of a recession approaches 60%, a level that, based on our historical estimates, is generally followed by a recession in our sample (figure 2, red lines).

Author(s): Andrea Ajello , Luca Benzoni , Makena Schwinn , Yannick Timmer , Francisco Vazquez-Grande

Publication Date: August 2022

Publication Site: Federal Reserve Bank of Chicago