Link: https://www.budget.senate.gov/imo/media/doc/letter_to_citizens.pdf

Graphic:

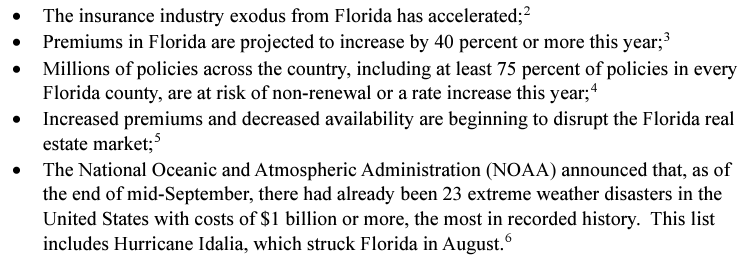

Excerpt:

As of 2022, Citizens’ market share for homeowners multi-peril policies was approaching 20 percent, having more than doubled since 2020. As private insurers in Florida continue to go insolvent or exit the state, Citizens’ market share will likely continue to grow. At 20 percent market share, Citizens’ losses could be as high as $36 billion in the scenario studied by Swiss Re or $162 billion in the scenario studied by Cambridge and Munich Re (assuming that 60 percent of total losses are insured). If Citizens had to raise $162 billion to cover losses, that would result in an approximately $20,000 assessment for every homeowners insurance policyholder in Florida.

….

To that end, please respond to the following requests for information and documents by December 21, 2023:

1. What modeling or other analysis has Citizens done to estimate its total potential exposure to various worst case hurricane scenarios? What is the upper range of Citizens’ potential losses? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ potential losses.

2. What modeling or other analysis has Citizens done to estimate its market share over the next decade? What does Citizens project its market share to be in each of the next 10 years? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ future market share.

3. What modeling or other analysis has Citizens done to determine its ability to fully pay out claims resulting from various loss scenarios? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ financial position and (in)solvency under such scenarios.

4. What are Citizens’ current assets? What is Citizens’ total reinsurance coverage? What are the maximum total claims Citizens would be able to pay out without having to levy an assessment on Florida policyholders? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ current assets, reinsurance, and ability to pay claims.

5. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Michael Yaworsky, their staffs, or any other state officials regarding Citizens’ current or future solvency? Please provide copies of these communications.

6. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials regarding what Citizens and/or the State would do if Citizens were unable to cover its losses? Please provide copies of these communications.

7. Has Citizens contemplated asking for a federal bailout if it were unable to cover its losses? Has Citizens discussed the possibility of a federal bailout with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials? Please provide copies of these communications.

Author(s): Sheldon Whitehouse

Publication Date: 30 Nov 2023

Publication Site: Senate website