Link: https://www.rstreet.org/2022/12/12/2022-insurance-regulation-report-card/

PDF link of report: https://www.rstreet.org/wp-content/uploads/2022/12/r-street-policy-study-no-272.pdf

Graphic:

Excerpt:

KEY POINTS

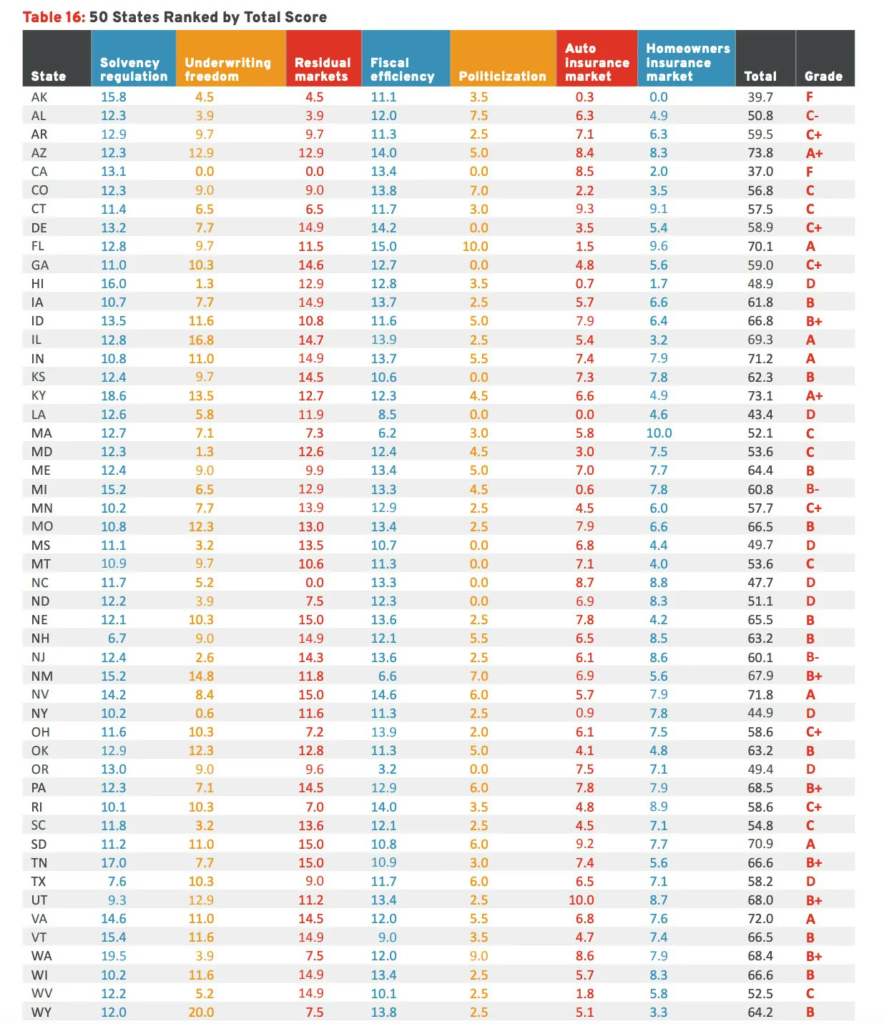

- The RSI Insurance Regulation Report Card analyzes and evaluates the effectiveness of state government regulation of property and casualty insurance and assigns a letter grade to all 50 states. The grade for each state was calculated by adding the weighted results from seven categories.

- The highest grades were for Kentucky and Arizona, both of which received an A+. At the other end of the spectrum, California and Alaska both scored an F.

- 20 states had a higher grade than they did in R Street’s 2020 edition of the Report Card, 23 maintained the same grade and seven had lower grades. This result is positive and means that insurance regulatory regimes have become more effective and efficient in the past two years.

Executive Summary

We are pleased to present the 10th edition of R Street’s Insurance Regulation Report Card, which analyzes and evaluates the effectiveness of U.S. insurance regulation of property and casualty insurance. The first iteration of this report was published in June 2012, and this 2022 edition largely follows the format of prior reports. It begins with a brief introduction on the current landscape of U.S. insurance regulation; reviews recent, relevant federal and state-based regulatory changes; presents a detailed evaluation of the effectiveness of each state’s regulation of insurance in seven key categories; and synthesizes those category evaluations by offering a “report card” grade for each state for analysis and comparison purposes.This report draws on 2021 year-end statutory insurance financial statistics and the most recent datasets available for non-financial information. Sources include data and reports from the National Association of Insurance Commissioners (NAIC), S&P Global Market Intelligence, National Conference of State Legislatures, R Street analyses and others, all of which were accessed through Sept. 30, 2022.

In this report, we seek to shed light on the same three foundational issues we have focused on in past iterations of this report card:

• How free are consumers to choose the insurance products they want?

• How free are insurers to provide the insurance products consumers want?

• How effectively are states discharging their duties to monitor insurer solvency and foster competitive, private insurance markets?

Author(s): Jerry Theodorou

Publication Date: 12 Dec 2022

Publication Site: R Street