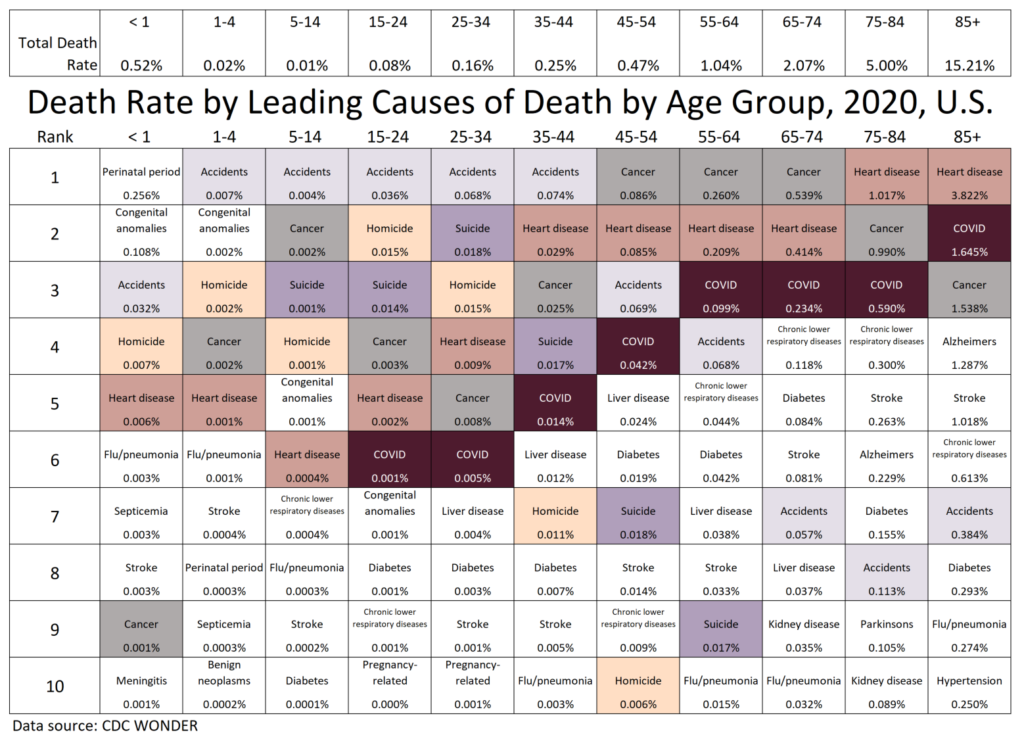

I present the rates in percentages, as opposed to the more traditional number (which is per 100,000 people per year), because I do not want people to get this confused with the raw counts of people who died. Yes, that does mean there are a lot of small numbers. For children, I even had to extend some out to 4 decimal places to get a significant figure.

In adulthood, natural causes of death tend to increase in rate with increasing age. More below.

External causes (accidents, homicides, and suicide) will have the similar rates over broad ages but drop dramatically in ranking with increasing age — as the natural causes become more likely to occur.

COVID has a similar pattern in mortality as heart disease — indeed, the heart disease death rate is approximately twice that of the COVID death rate for the entire age range from 15 to 85+ on the table.

If inflation pushes up interest rates and accelerates wage growth, that could take some of the pressure off of public pension plan performance. Since the Great Recession, pension plans have been steadily lowering their assumed annual rate of return to better match the low-interest rate environment. Pension plan actuaries factor that rate when in calculating a government’s annual pension bill. Lowering that rate results in a higher bill because governments have to make up the difference.

More stable returns. Rising inflation can result in higher returns from a pension plan’s fixed-income assets. Unlike the volatile equities market, the nice steady investment return from fixed-income securities is much nicer to rely on from a planning perspective. In fact, bonds used to be pensions’ bread and butter until interest rates began falling in the 1990s.

The National Association of State Retirement Administrators’ research director Keith Brainard told me this week that if inflation is sustained, governments could decide to stop lowering their investment return assumptions and some could even start raising them again.

That could result in lower pension bills for governments with healthy plans. Or in the case of struggling plans like Chicago or Kentucky, it could at least slow the pace of their rising pension bills.

Higher worker contributions. What’s more, noted Brainard, accelerated wage growth also means those workers paying into pension plans will be contributing slightly more. “What wages will do when inflation is 2% is a lot different than when it’s 6%,” he said.

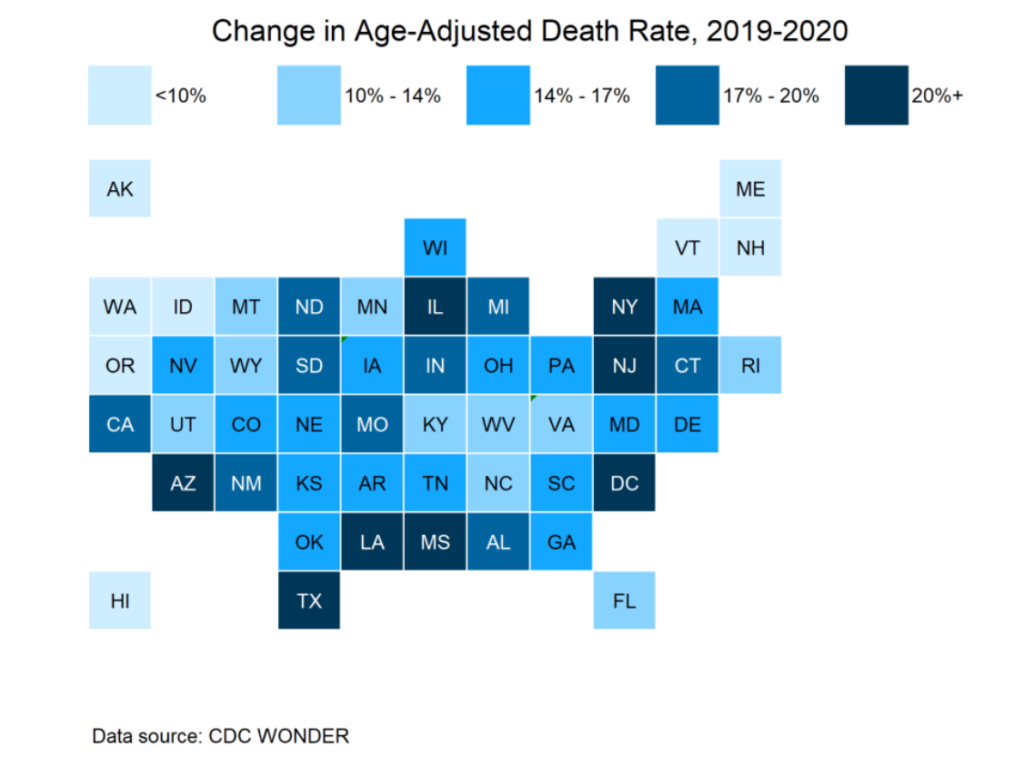

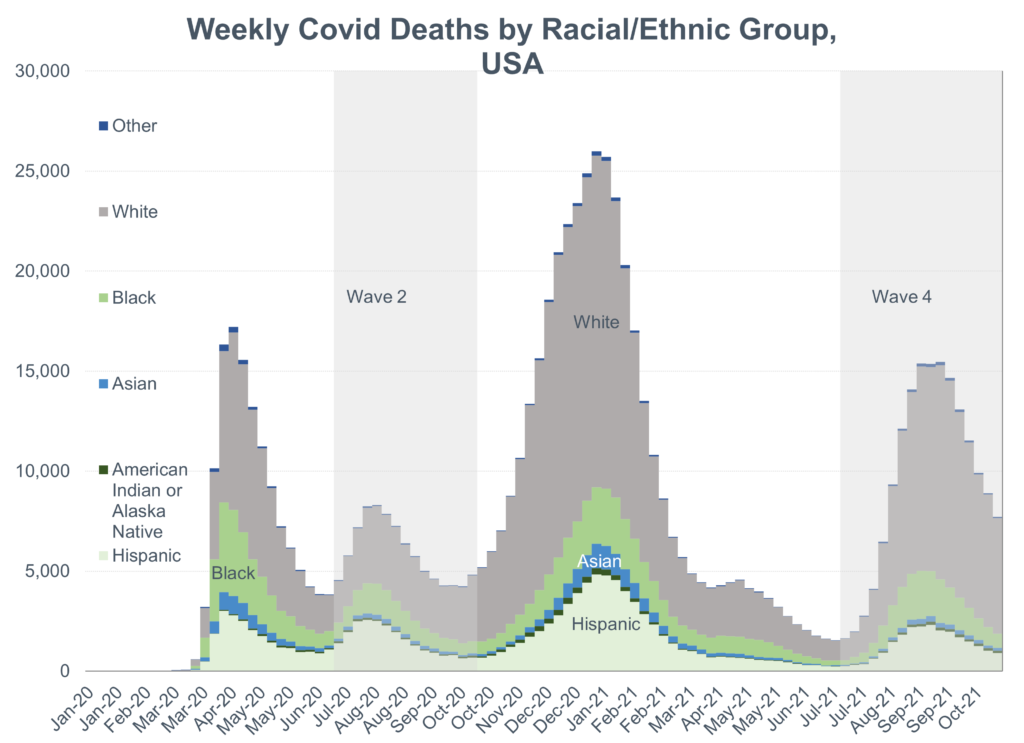

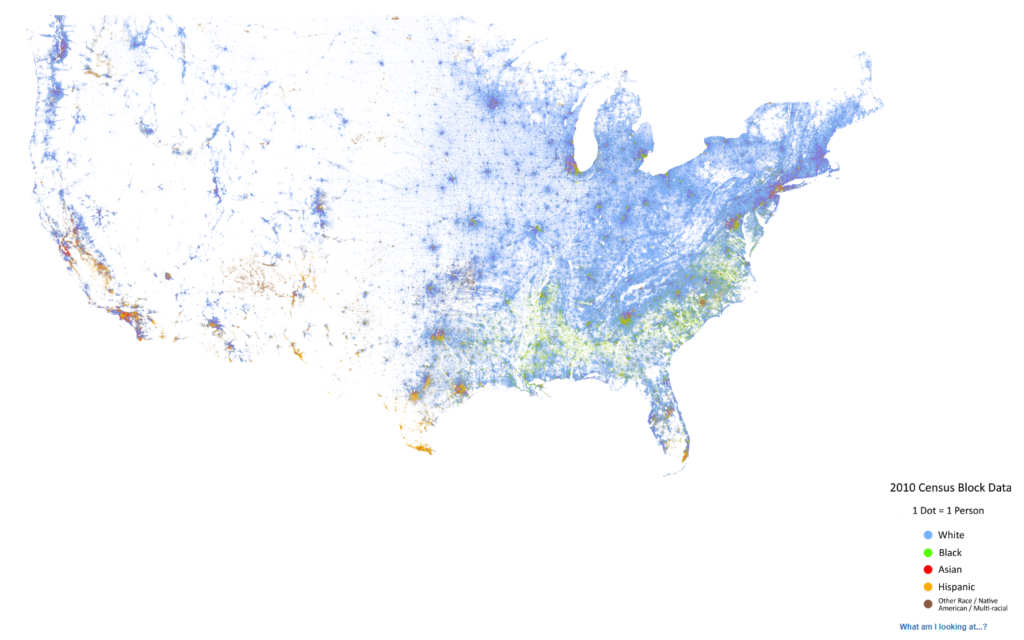

The ranking tables do reflect where COVID hit hard in 2020 — the spring 2020 wave in the northeast, and the summer 2020 wave along the south and southwest (Texas, in particular). No, Florida didn’t show its big COVID impact until January 2021, so it’s pretty far down on this ranking table.

This way, we can see if there are any geographic patterns. We did know the hot spots of NY, NJ, IL (mainly around Chicago), DC, TX, Louisiana (around New Orleans), Arizona. I had not been aware of Mississippi being so bad, but maybe that was spillover from New Orleans.

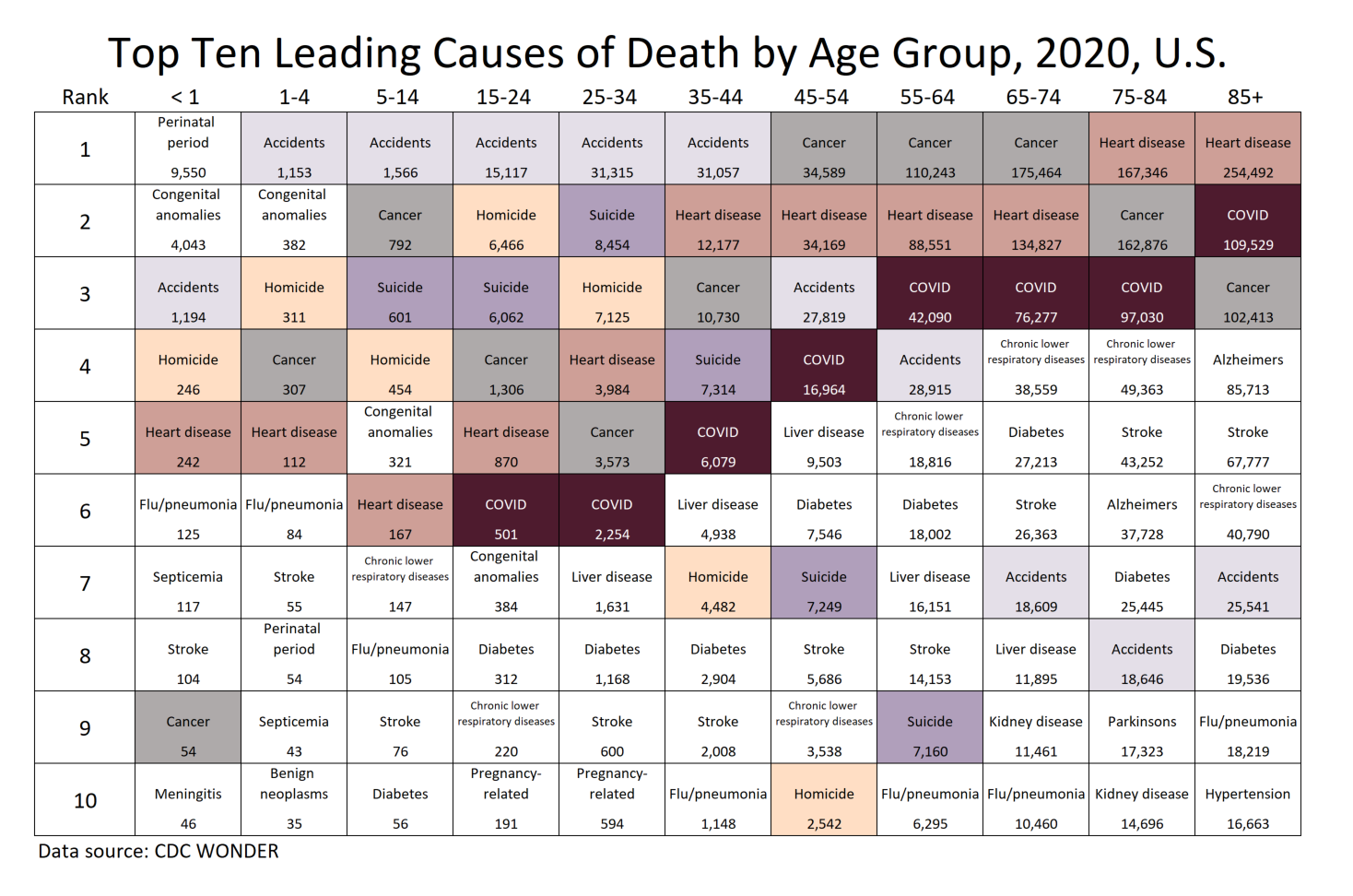

The numbers below each cause are the total number of finalized deaths in CDC Wonder as of 11 January 2022 for the completed calendar year 2020.

COVID deaths for under age 15 weren’t in the top 10 causes for those age groups, which is why they aren’t seen in the table. But you may be interested in those numbers: at #12 for ages 5-14, with 49 deaths at #12 for ages 1-4, with 19 deaths at #13 for infant mortality (<1 year), at 35 deaths

In general, other than the new cause of COVID, most of the causes of death were in the same rank order as in 2019, with a few switches for causes that tend to be close in numbers.

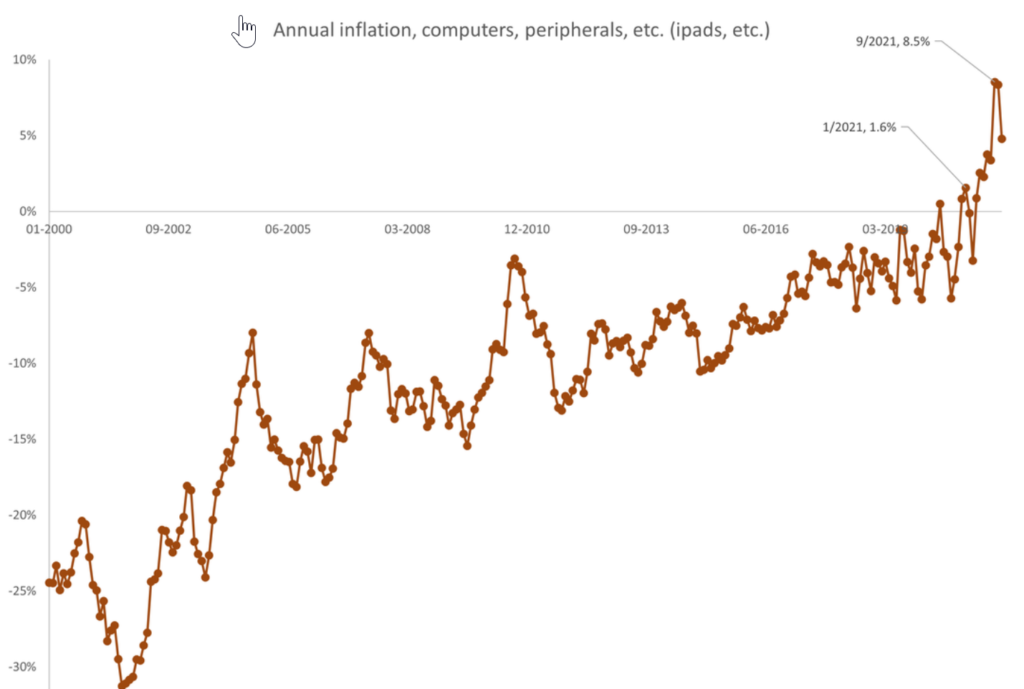

Productivity gains in consumer electronics have not been able to exceed the erosion of the currency’s value.

Bills such as Build Back Better are just a piece of the reason — we have more coming. We have a huge demographic issue, and a huge Social Security and Medicare bill not yet paid. Shoveling out more money and writing more IOUs will not help matters.

The pandemic created a lot of uncertainty around state and local government revenues for much of 2020. That was a big reason for the dramatic boost in the rate of bonds issued with insurance that year: In total, $34.45 billion in new bonds carried insurance — the highest since the Great Recession ended in 2009. Even with the economic stabilization this year, insurance is still going strong. Through October 2021, wrapped municipal bond issuance totaled $31.5 billion, according to RBC Capital Markets.

Looking ahead, the chatter about municipal climate risk has been increasing in recent years. Extreme weather events linked to climate change have called into question the preparedness and resiliency of utilities and other government issuers, while studies point to the potential long-term economic effect. One BlackRock Investment Institute report estimated that some vulnerable cities could see economic losses of up to 10% of GDP without decisive action.

The bottom line: Insurance provided safety for muni market investors during the pandemic and its continued use indicates that investors and issuers are both finding it attractive in situations where there might be a little more long-term uncertainty. Climate risk plays right into this notion. While no one expects bond insurance to dominate the market as it once did, it’s likely that the pandemic spike in usage is here to stay.

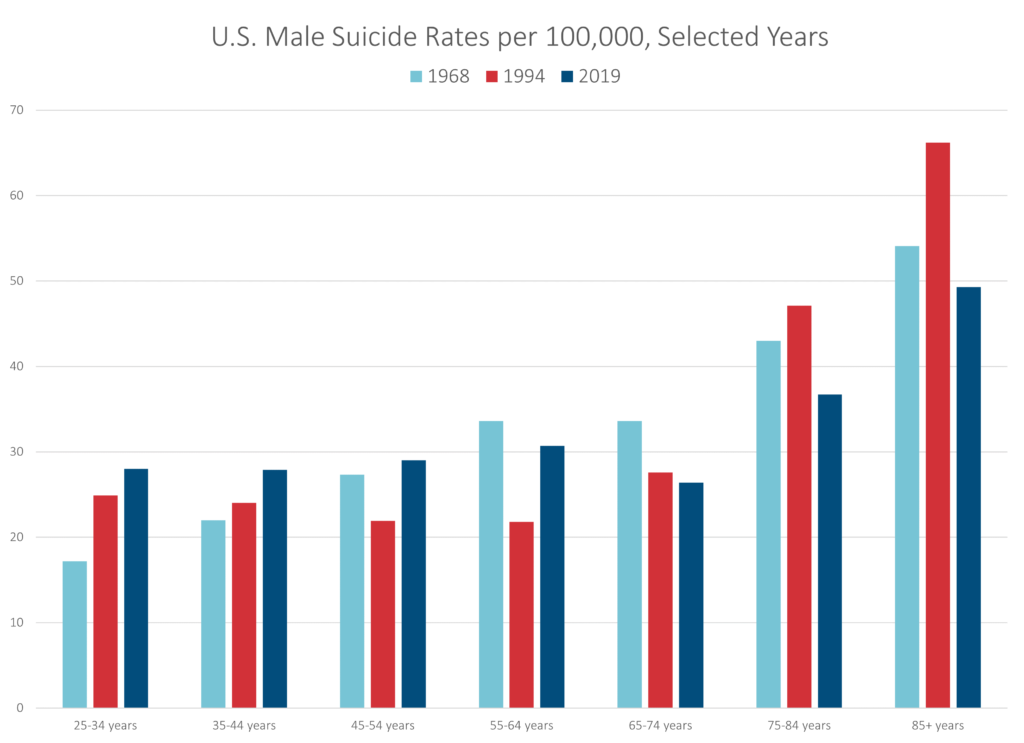

Let’s look at the rate trend for those over age 55 — the suicide death rates in 2019 are lower than they were in 1968. There has been an improvement.

But under age 55, we have a different story.

Indeed, from age 25 to 64, we see a flattening of the suicide death rate, as we have a rate in 1968 which was fairly low rising up to a level similar to that of much older men.

As I’ve said about other mortality trends — in many cases, I can’t tell you why this is happening. I don’t know. I can just see that it is happening. And I would like to do something about it.

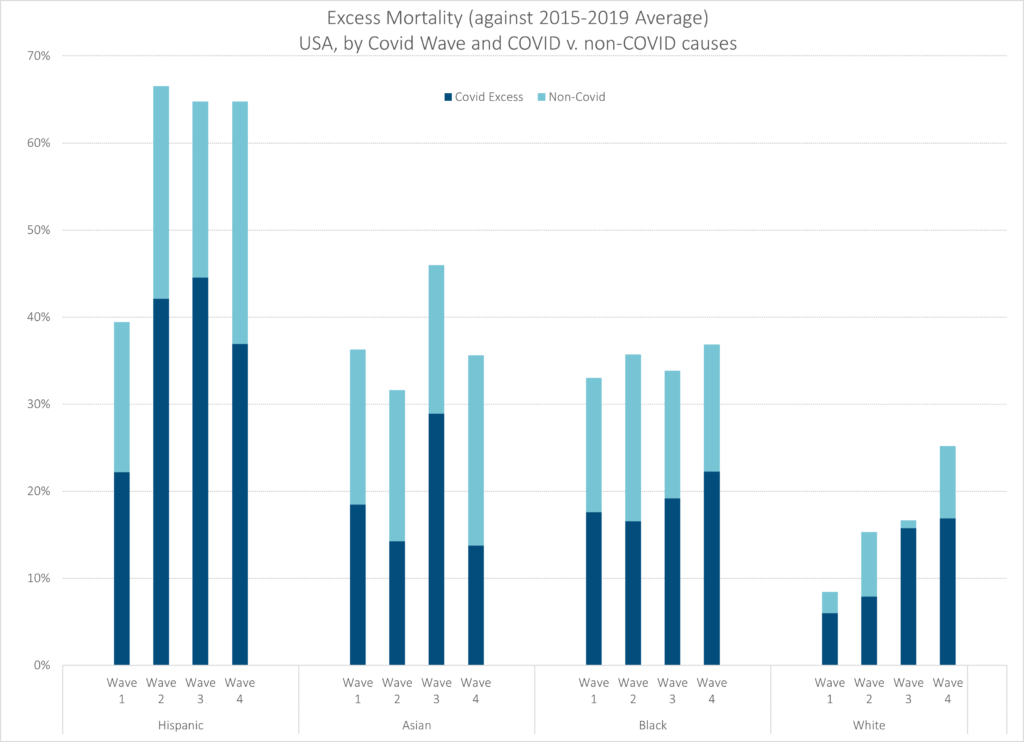

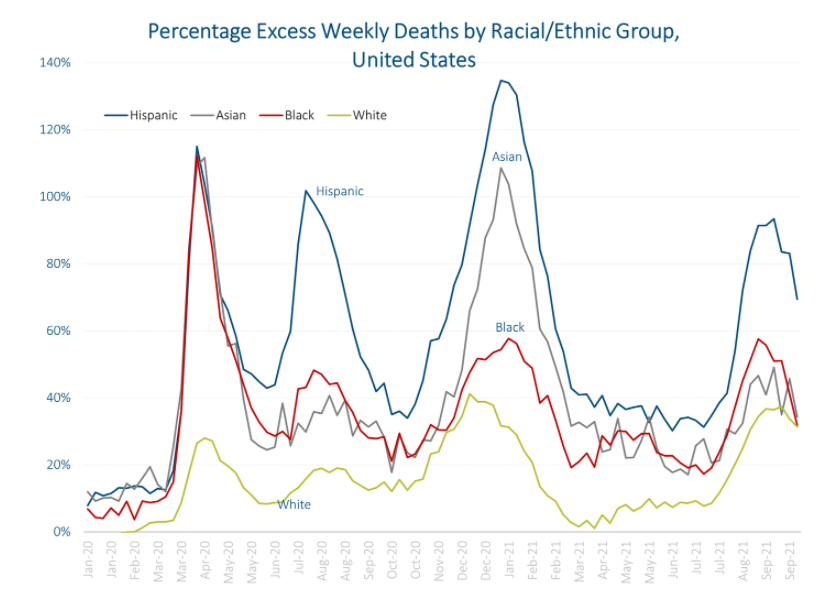

As noted earlier, the Hispanic excess mortality was about a level as the other non-White groups, but then spiked with Wave 2 and stayed very high.

The Asian group saw its excess mortality peak with Wave 3 — remember, that’s the large wave with the most COVID deaths. But they have been at about 30 – 35% excess mortality for the other waves.

The Black group looks like it’s slightly rising in excess mortality, but staying within a fairly narrow range of about 33% to 37% excess mortality.

The White group is definitely showing an increasing trend of excess mortality. Interesting.

Due to the White group’s increasing excess mortality, the overall population is showing an increasing trend — look, Whites have been the majority of deaths for a long time, as they’re the majority of old folks. That’s how that works.

About ten years ago, when the replication crisis started, we learned a certain set of tools for examining studies.

Check for selection bias. Distrust “adjusting for confounders”. Check for p-hacking and forking paths. Make teams preregister their analyses. Do forest plots to find publication bias. Stop accepting p-values of 0.049. Wait for replications. Trust reviews and meta-analyses, instead of individual small studies.

These were good tools. Having them was infinitely better than not having them. But even in 2014, I was writing about how many bad studies seemed to slip through the cracks even when we pushed this toolbox to its limits. We needed new tools.

I think the methods that Meyerowitz-Katz, Sheldrake, Heathers, Brown, Lawrence and others brought to the limelight this year are some of the new tools we were waiting for.

Part of this new toolset is to check for fraud. About 10 – 15% of the seemingly-good studies on ivermectin ended up extremely suspicious for fraud. Elgazzar, Carvallo, Niaee, Cadegiani, Samaha. There are ways to check for this even when you don’t have the raw data. Like:

The Carlisle-Stouffer-Fisher method: Check some large group of comparisons, usually the Table 1 of an RCT where they compare the demographic characteristics of the control and experimental groups, for reasonable p-values. Real data will have p-values all over the map; one in every ten comparisons will have a p-value of 0.1 or less. Fakers seem bad at this and usually give everything a nice safe p-value like 0.8 or 0.9.

GRIM – make sure means are possible given the number of numbers involved. For example, if a paper reports analyzing 10 patients and finding that 27% of them recovered, something has gone wrong. One possible thing that could have gone wrong is that the data are made up. Another possible thing is that they’re not giving the full story about how many patients dropped out when. But something is wrong.

But having the raw data is much better, and lets you notice if, for example, there are just ten patients who have been copy-pasted over and over again to make a hundred patients. Or if the distribution of values in a certain variable is unrealistic, like the Ariely study where cars drove a number of miles that was perfectly evenly distributed from 0 to 50,000 and then never above 50,000.

Green bonds. Issuance is expected to hit a record high this year and so are municipal green bond offerings. My friend and colleague Mark Funkhouser explains why local leaders should take advantage of this alignment of financial interests and moral ones.

More spending flexibility in the American Rescue Plan. Legislation now making its way through Congress would allow governments to use some of their ARP funds for highway and transit projects and to address natural disasters.

Rising income tax revenue. The K-shaped recovery and federal stimulus has resulted in the largest median state personal income jump in 14 years. According to Fitch Ratings, state income tax revenues increased by 6.3% last year and this year is expected to produce similar growth. This has implications for public pensions, tax cuts and — of course — the 2022 midterms.

Companies ranging from Ford Motor Company to Union Pacific Railroad report substantially improved business activity for the month of October. The current recession may have ended in the summer. Aggregate bond purchases were the largest since one year ago as Americans finally start investing again. Opinion articles, however, advise against common stock and its gambling attributes.

Historical Fact: American and international investors will soon assume high GDP growth is a feature of the American economy, as God-given and laid down in the natural order as the seasons. At the end of 1921, however, it’s not yet clear elements are present for business revival.

And now you can see it — the blue curve for Hispanics has a summer 2020 peak much higher than that for whites, Blacks, and Asians.

I want to note the high peak for Asian deaths in winter 2020-2021.

See that there is a high spike for Asian, Hispanic, and Black in that first NYC-centered wave that we’ve known so well… but a little blip for White. And I want you to think about that a little. Because that really explains a lot of the disproportionate effects on minorities in the U.S. and it goes back to Charles Blow’s question at the top of this post.

The answer to all of this being geographic distribution.