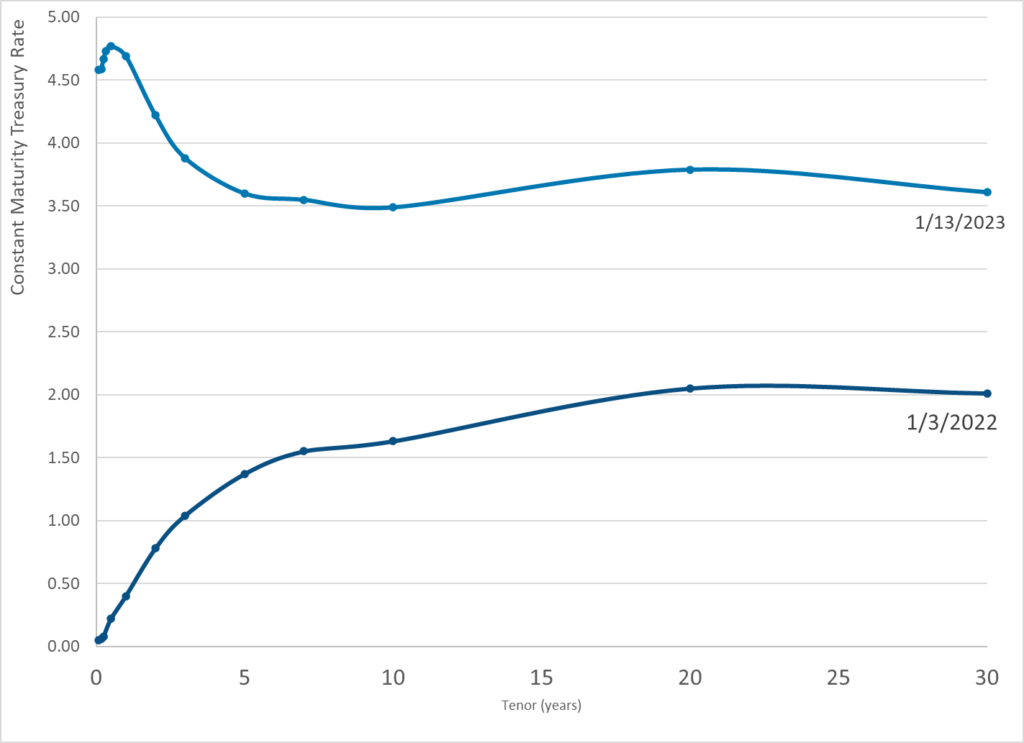

Graphic:

Publication Date: 13 Jan 2023

Publication Site: Treasury Department

All about risk

Graphic:

Publication Date: 13 Jan 2023

Publication Site: Treasury Department

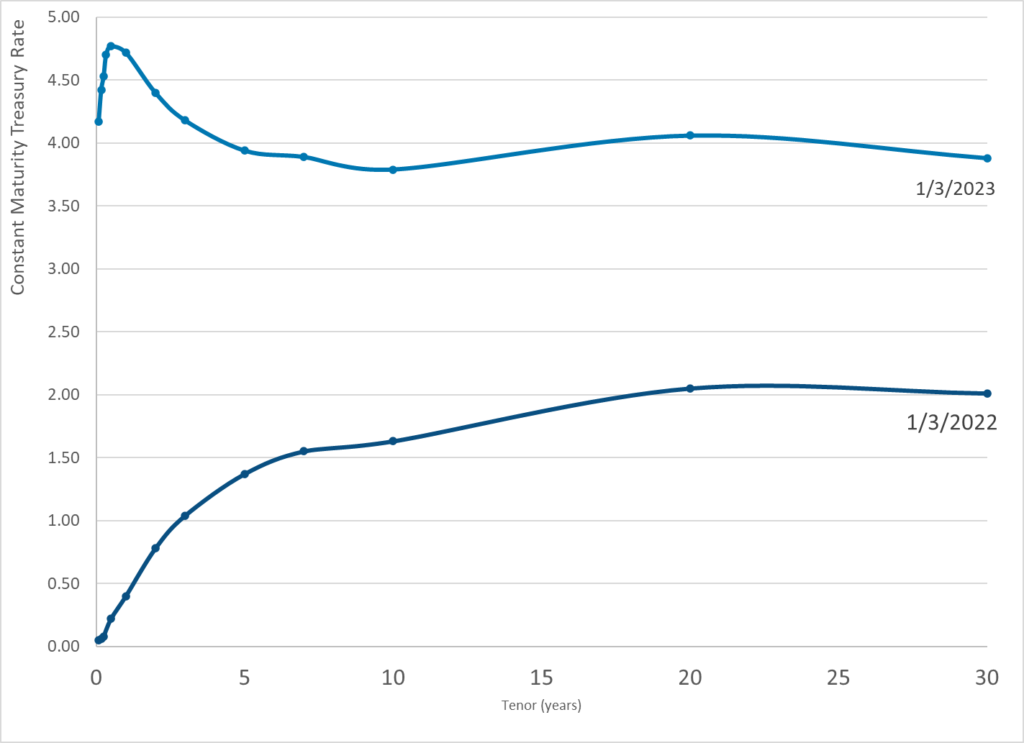

Graphic:

Publication Date: 3 Jan 2023

Publication Site: Treasury Department

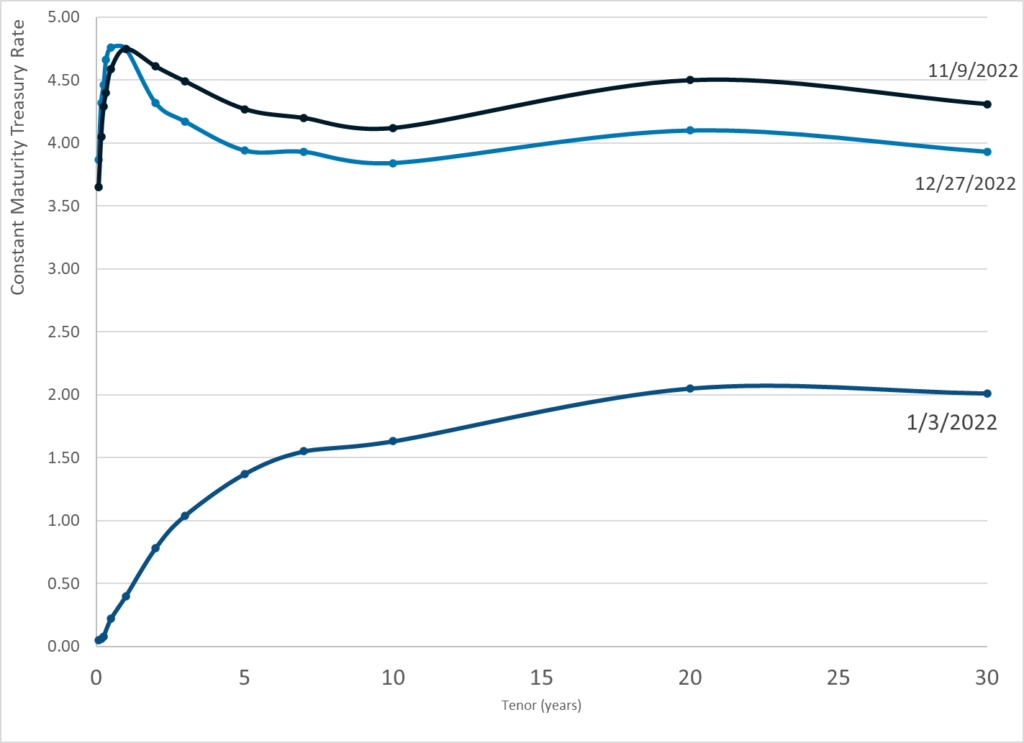

Graphic:

Publication Date: 27 Dec 2022

Publication Site: Treasury Department

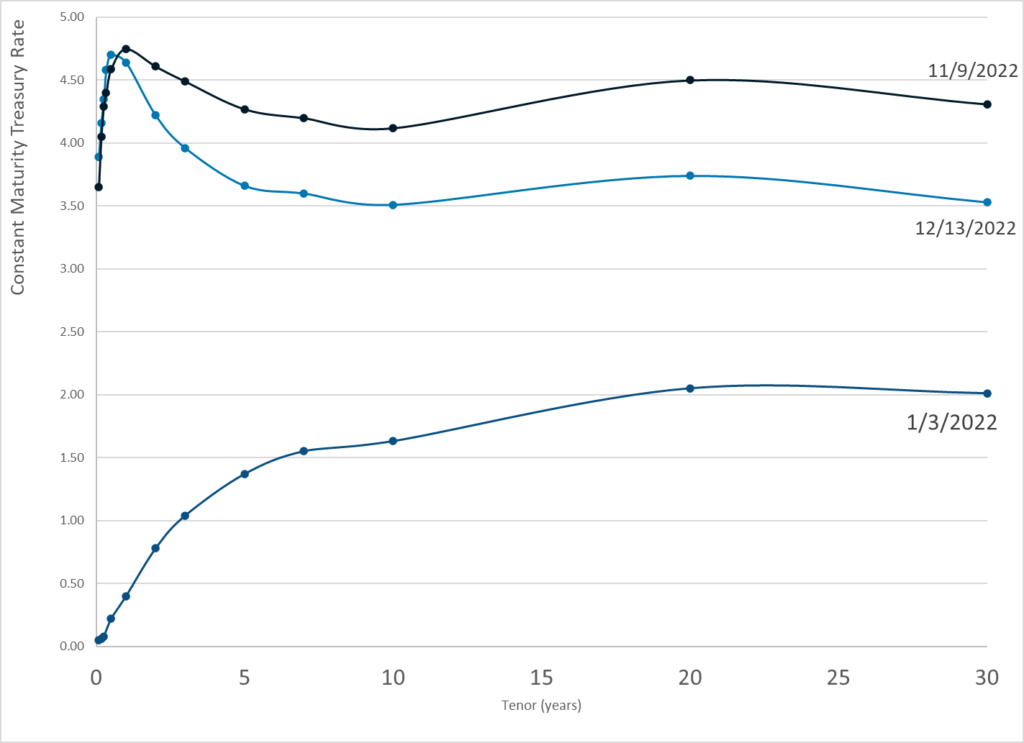

Graphic:

Publication Date: 13 Dec 2022

Publication Site: Dept of Treasury

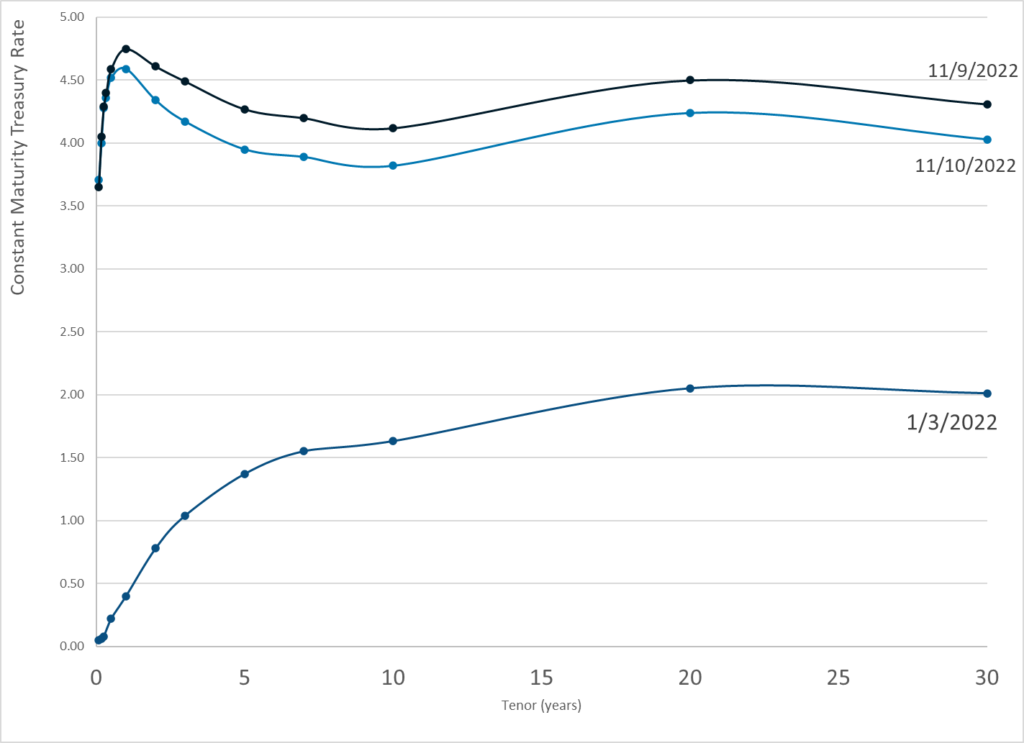

Graphic:

Publication Date: 10 Nov 2022

Publication Site: Treasury Dept

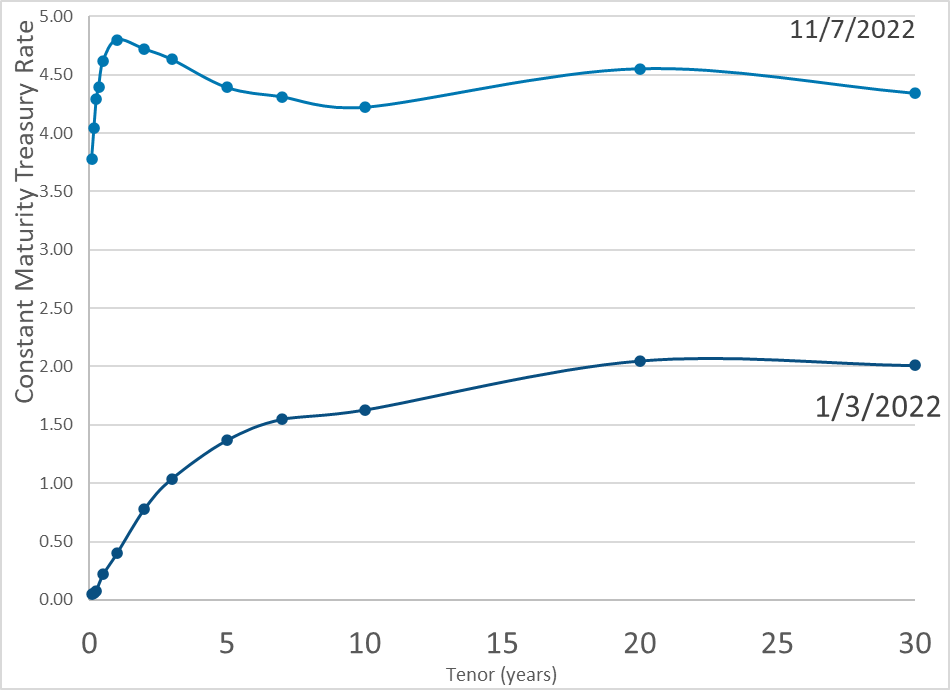

Graphic:

Publication Date: 7 Nov 2022

Publication Site: Treasury Dept

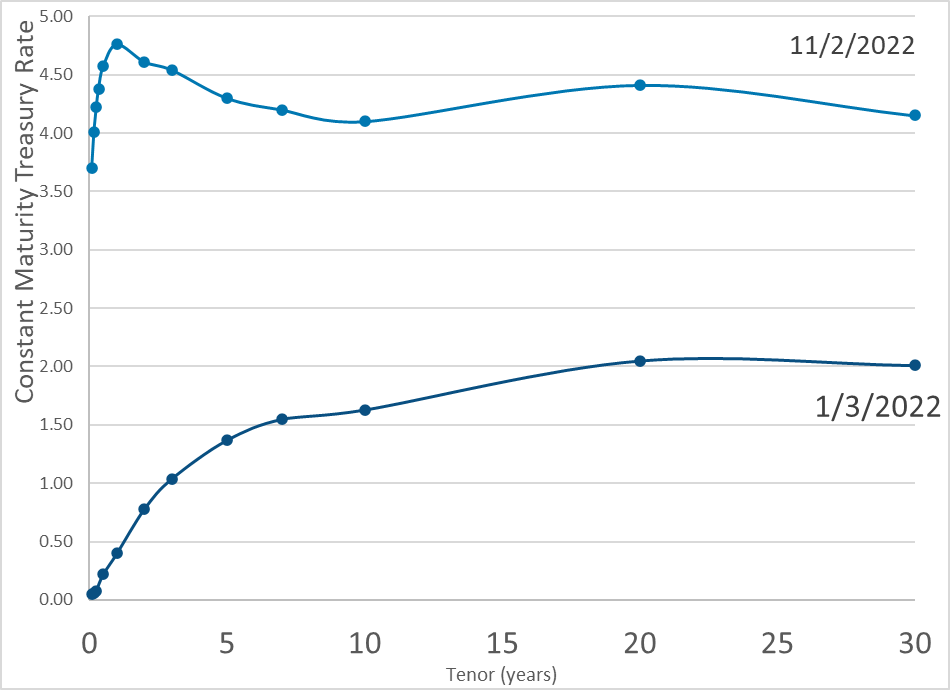

Graphic:

Publication Date: 2 Nov 2022

Publication Site: Dept of Treasury

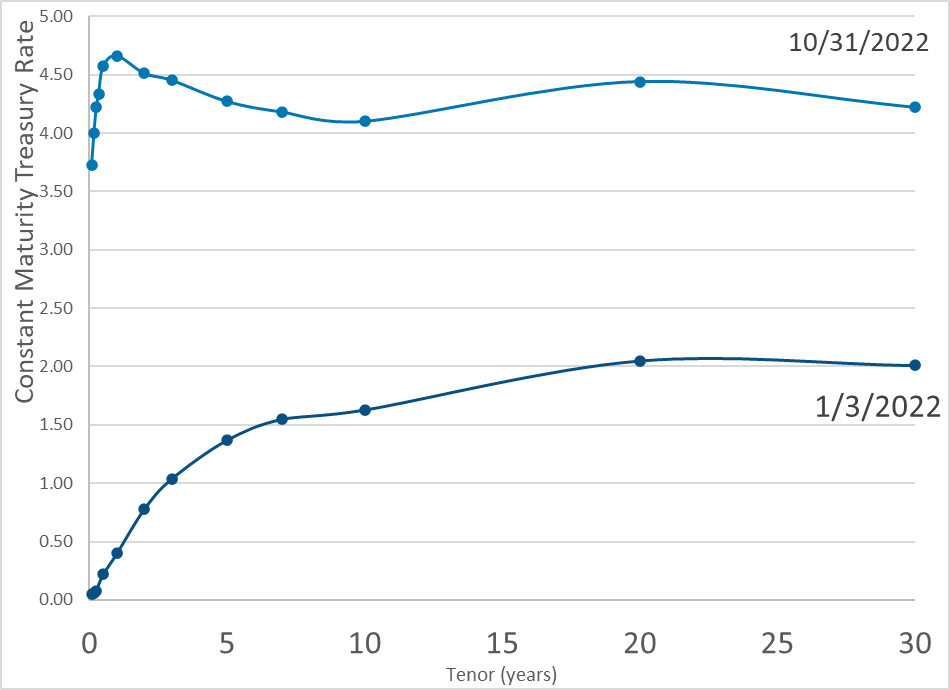

Graphic:

Publication Date: 31 Oct 2022

Publication Site: Treasury Dept

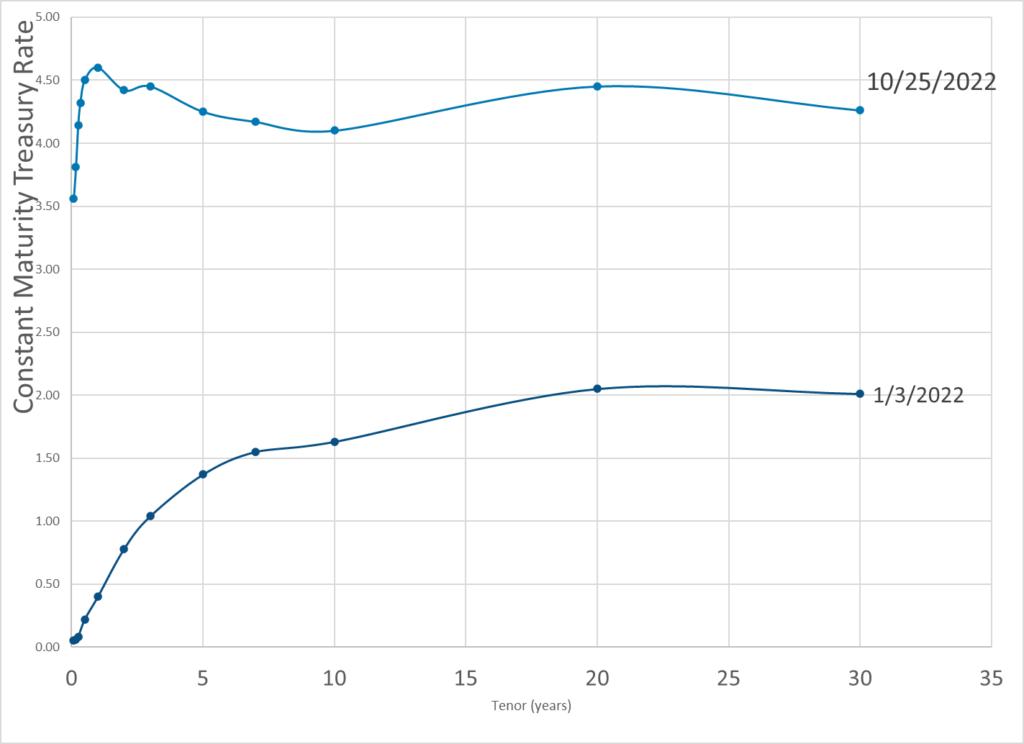

Graphic:

Publication Date: 25 Oct 2022

Publication Site: Dept of Treasury

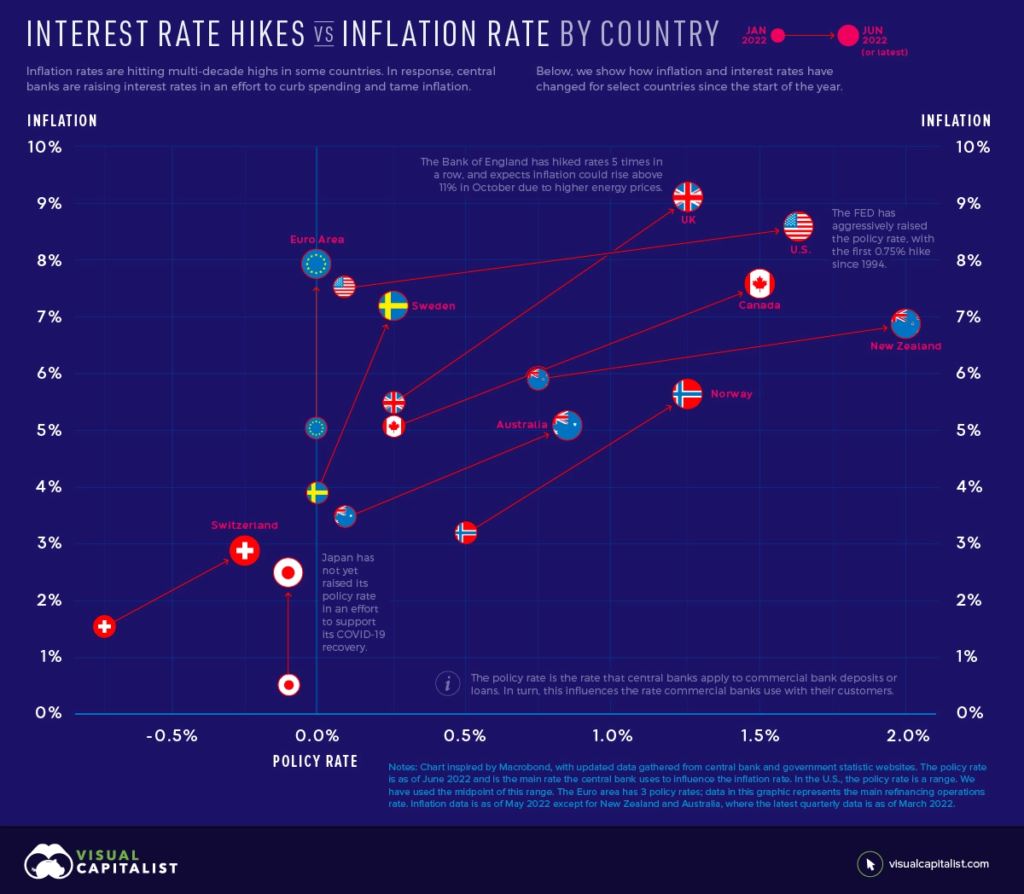

Link: https://www.visualcapitalist.com/interest-rate-hikes-vs-inflation-rate-by-country/

Graphic:

Excerpt:

To understand how interest rates influence inflation, we need to understand how inflation works. Inflation is the result of too much money chasing too few goods. Over the last several months, this has occurred amid a surge in demand and supply chain disruptions worsened by Russia’s invasion of Ukraine.

In an effort to combat inflation, central banks will raise their policy rate. This is the rate they charge commercial banks for loans or pay commercial banks for deposits. Commercial banks pass on a portion of these higher rates to their customers, which reduces the purchasing power of businesses and consumers. For example, it becomes more expensive to borrow money for a house or car.

Ultimately, interest rate hikes act to slow spending and encourage saving. This motivates companies to increase prices at a slower rate, or lower prices, to stimulate demand.

Author(s): Jenna Ross, Nick Routley

Publication Date: 24 June 2022

Publication Site: Visual Capitalist

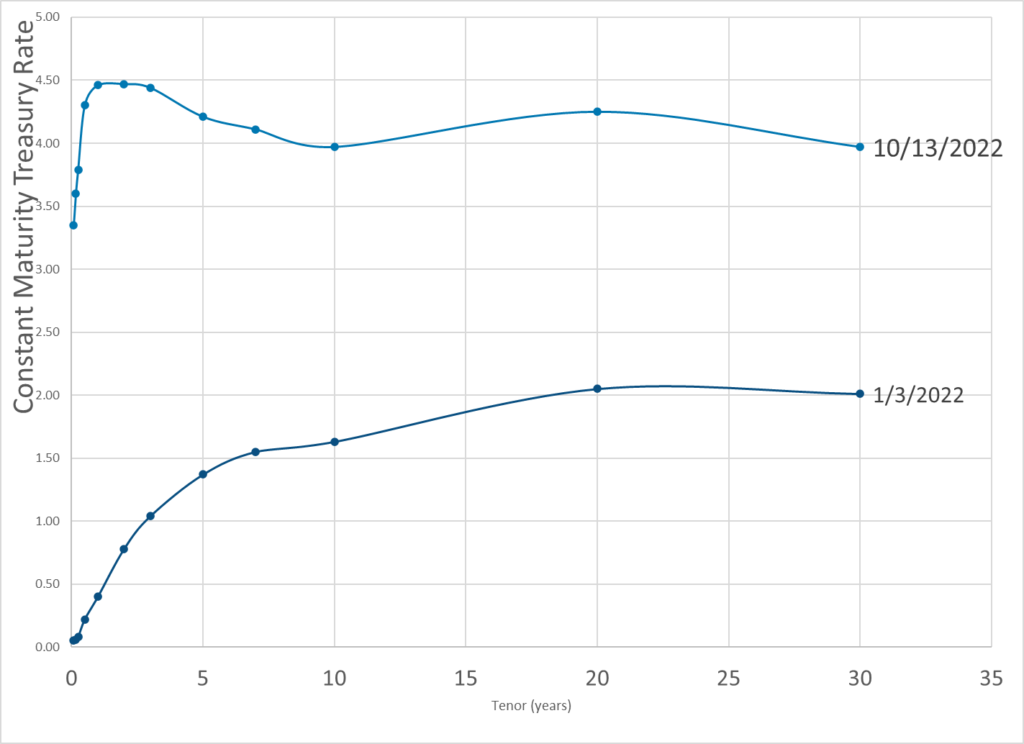

Graphic:

Publication Date: 13 Oct 2022

Publication Site: Dept of Treasury

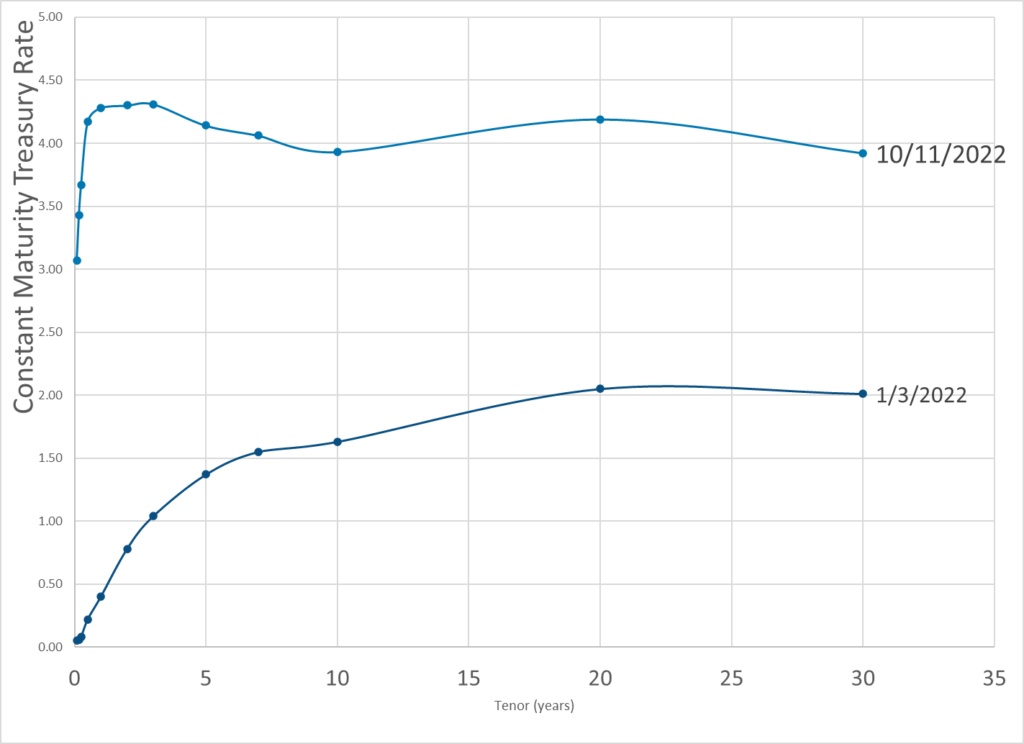

Graphic:

Publication Date: 11 Oct 2022

Publication Site: Dept of Treasury