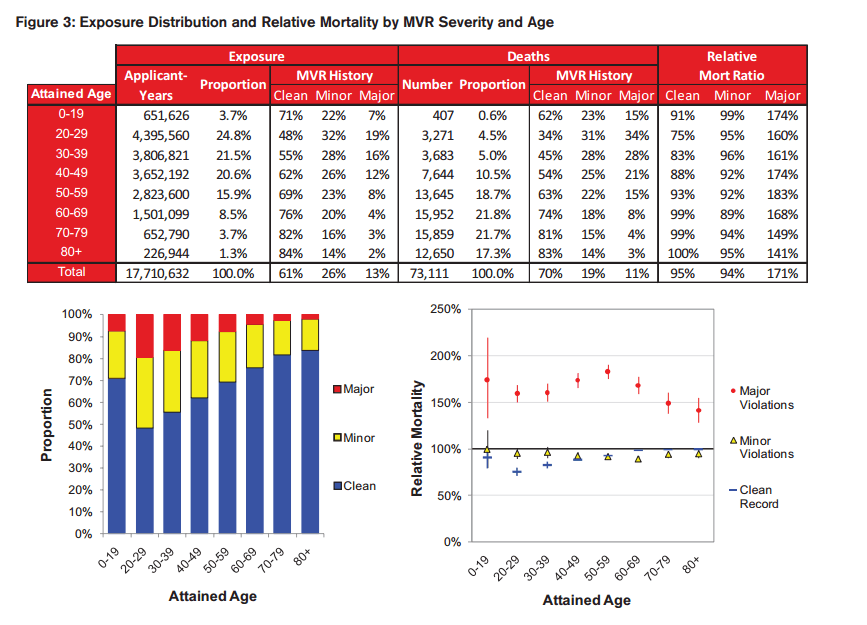

This paper analyzes the all-cause mortality experience of a large cohort of applicants linked to the number and severity of their recent driving infractions. The study verifies that significant excess mortality risk exists for applicants with a recent history of either major or frequent driving violations. The extra mortality risk for drivers with adverse MVRs is persistent across ages for both genders. The results from this study also suggest that MVRs likely have positive protective value across a wide spectrum of ages and face amounts.

The five biggest auto insurers in Illinois have raised automobile insurance rates a whopping $527 million since January, an analysis by two consumer groups shows.

That follows about $1.1 billion in rate increases last year by the top 10 Illinois car insurers.

The analysis by the nonprofit Illinois Public Interest Research Group and Consumer Federation of America looked at auto insurance rate increases by the five largest companies in Illinois: State Farm, Allstate, Progressive, Geico and Country Financial, which together make up 62% of the Illinois market.

…..

Now, state Rep. Will Guzzardi, D-Chicago, has introduced legislation to address those issues and crack down on insurers. Guzzardi’s bill would:

Require automobile insurers to get prior state approval for rate hikes.

Ban “excessive” insurance increases.

Prohibit using gender, marital status, age, occupation, schooling, home ownership, wealth, credit scores or a customer’s past insurance company relationships in setting car insurance rates.

It’s already illegal to use race, ethnicity and religion in setting rates. That would continue under Guzzardi’s proposal.

Author(s): Stephanie Zimmermann | Chicago Sun-Times

Why is the insurance industry now facing increased scrutiny on certain underwriting methods?

Insurers increasingly are turning to nontraditional data sets, sources and scores. The methods used to obtain traditional data—that were at one time costly and time-consuming—can now be done quickly and cheaply.

As insurers continue to innovate their underwriting techniques, increased scrutiny should be expected. It is not unreasonable for consumer advocates to push for increased transparency and explainability when insurers employ these advanced methods.

What is the latest regulatory activity on this topic in the various states and at the NAIC?

Activity in the states has been minimal. In 2021, Colorado became the first (and so far, only) state to enact legislation requiring insurers to test their algorithms for bias. Legislation nearly identical to the Colorado law was introduced in Oklahoma and Rhode Island in 2022, and it is likely other states will consider similar legislation. Connecticut is finalizing guidance that would require insurers to attest that their use of data is nondiscriminatory. Other states have targeted specific factors, but most have adopted a wait-and-see approach.

The NAIC created a new high-level committee to focus on innovation and AI, but it has become clear that a national standard is not likely at this time.

Author(s): INTERVIEW BY STEPHEN ABROKWAH, Interview with Neil Sprackling, president of Swiss Re Life & Health America Inc.

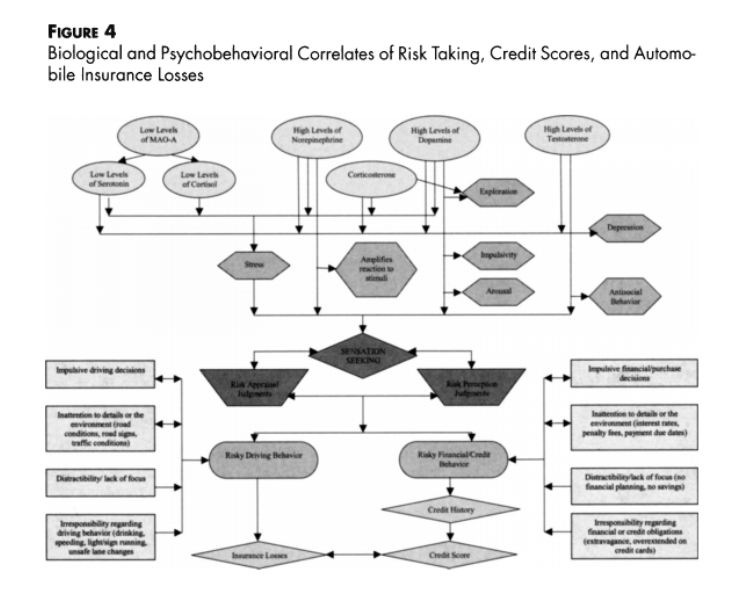

The most important new development in the past two decades in the personal lines of insurance may well be the use of an individual’s credit history as a classification and rating variable to predict losses. However, in spite of its obvious success as an underwriting tool, and the clear actuarial substantiation of a strong association between credit score and insured losses over multiple methods and multiple studies, the use of credit scoring is under attack because there is not an understanding of why there is an association. Through a detailed literature review concerning the biological, psychological, and behavioral attributes of risky automobile drivers and insured losses, and a similar review of the biological, psychological, and behavioral attributes of financial risk takers, we delineate that basic chemical and psychobehavioral characteristics (e.g., a sensation-seeking personality type) are common to individuals exhibiting both higher insured automobile loss costs and poorer credit scores, and thus provide a connection which can be used to understand why credit scoring works. Credit scoring can give information distinct from standard actuarial variables concerning an individual’s biopsychological makeup, which then yields useful underwriting information about how they will react in creating risk of insured automobile losses.

Author(s): Patrick L. Brockett and Linda L. Golden

Publication Date: originally 2007

Publication Site: jstor, The Journal of Risk and Insurance

Cite: Brockett, Patrick L., and Linda L. Golden. “Biological and Psychobehavioral Correlates of Credit Scores and Automobile Insurance Losses: Toward an Explication of Why Credit Scoring Works.” The Journal of Risk and Insurance, vol. 74, no. 1, 2007, pp. 23–63. JSTOR, http://www.jstor.org/stable/4138424. Accessed 22 May 2022.

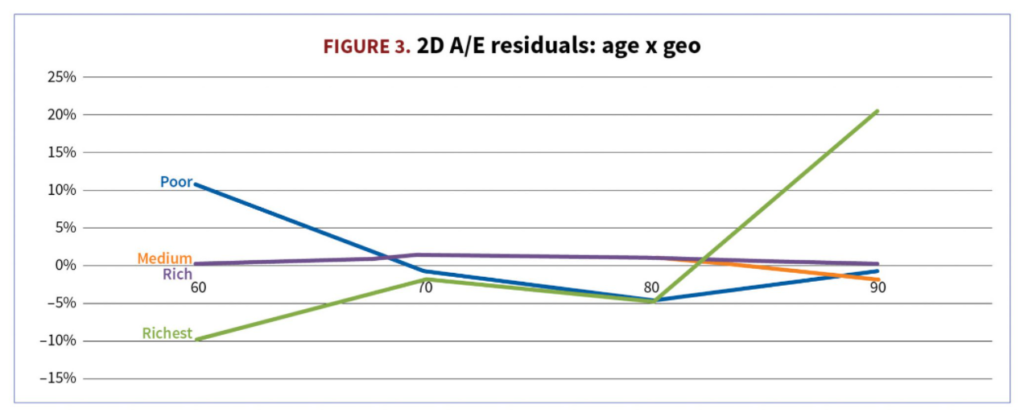

3. Identify pockets of good and poor model performance. Even if you can’t fix it, you can use this info in future UW decisions. I really like one- and two-dimensional views (e.g., age x pension amount) and performance across 50 or 100 largest plans—this is the precision level at which plans are actually quoted. (See Figure 3.)

What size of unexplained A/E residual is satisfactory at pricing segment level? How often will it occur in your future pricing universe? For example, 1-2% residual is probably OK. Ten to 20% in a popular segment likely indicates you have a model specification issue to explore.

Positive residuals mean that actual mortality data is higher than the model predicts (A>E). If the model is used for pricing this case, longevity pricing will be lower than if you had just followed the data, leading to a possible risk of not being competitive. Negative residuals mean A<E, predicted mortality being too high versus historical data, and a possible risk of price being too low.

Leave it to California lawmakers, however, to cast aside thousands of years of complex commercial history in a misguided attempt to fix an admittedly legitimate insurance problem. Thanks to Proposition 103, a 1988 ballot measure, California already has a distorted insurance market that gives the insurance commissioner czar-like powers to approve rate increases and impose rate decreases.

Because of that law, insurers have a tough time adjusting rates to manage their risks. It’s a long, cumbersome, and antagonistic government process to adjust rates. Their other lever for ensuring solvency is to reduce their underwriting risks by, say, not writing fire-insurance policies to homeowners who live in high fire-risk areas or car insurance policies to drivers with multiple DUIs.

….

Instead, California Assemblymember Marc Levine, D-Marin County, has introduced Assembly Bill 1522, which would prohibit insurers from canceling insurance policies solely because a home or business is located in a high-risk wildfire area. It epitomizes California’s economically illiterate edict approach.

Credit analytics firm FICO posits that the reason for the correlation of credit history and claim probability is that “individuals who closely and cautiously monitor and manage their finances tend to also take better care of their cars and homes and are, generally, more diligent in their risk management habits.” Because such individuals are found across demographic classifications, the discrimination argument becomes hard to uphold.

If insurers find that credit scores have bearing on accident propensity, insurers should be allowed to use them. Preventing insurers from deploying basic tools required to generate appropriate risk-adjusted prices leads to mispricing of risk, harming insurance buyers as well as insurers. What is more, such deprivation leads to unintended negative consequences—an unfair socialization of risk, leaving customers either overcharged or undercharged. Executive fiat prohibiting insurers from accessing the tools of their trade is tantamount to Pharaoh ordering the Israelites of old to make bricks without straw. Bad business, bad policy.

Democratic lawmakers have called on U.S. insurers including American International Group Inc., Berkshire Hathaway, Chubb Ltd., Liberty Mutual Insurance Co., MetLife Inc. and Travelers Cos. Inc. to explain how their fossil fuel underwriting policies align with their commitments to sustainability.

In a letter dated March 24, Sen. Sheldon Whitehouse, D-Rhode Island, and Senators Jeffrey A. Merkley, D-Oregon, Elizabeth Warren, D-Massachusetts, and Chris Van Hollen, D-Maryland, request information on each insurer’s fossil fuel underwriting and investment policies.

“An increasing number of your competitors have stopped underwriting coal and other fossil fuel projects and/or restricted their investments in coal and certain dirty and environmentally damaging oil and gas projects such as tar sands,” the letter said.

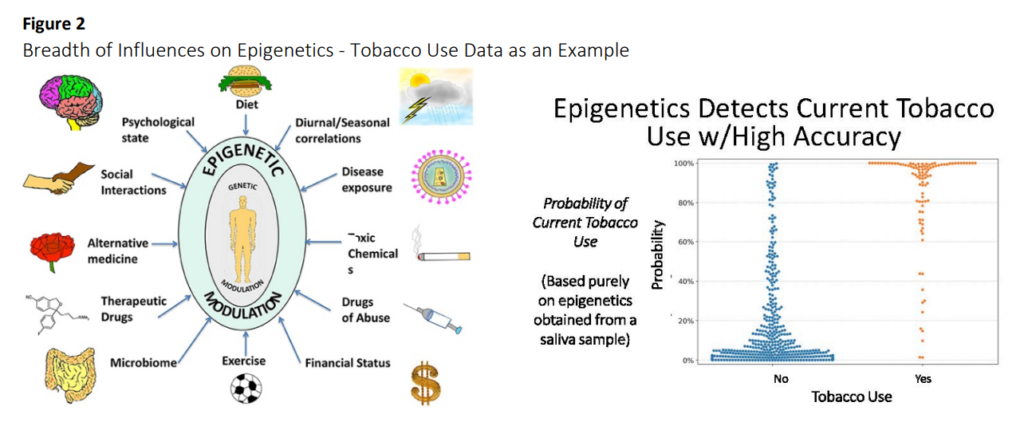

A new subset of Somatic non-blueprint information is the growing field of Epigenetics, defined as changes ‘above the genetics,’ where it has recently been found that lifestyle choices also induce non-heritable physical or chemical changes directly on a person’s DNA after birth, and can be measured by isolating the DNA and revealing these features. The U.S. Center for Disease Control states: “Epigenetics is the study of how your behaviors and environment can cause changes that affect the way your genes work. Unlike genetic changes, epigenetic changes are reversible and do not change your DNA sequence.” (9)

An example of the latter is a finding that the tips of our chromosomes – called telomeres – can shorten or lengthen in correlation with health status and ‘biological aging,’ a finding that was the subject of a 2009 Nobel Prize (10). An additional example of epigenetics is in tobacco use, shown below, and generally discussed at the 2020 SOA Health Conference by Dr. Brian Chen at this link https://webcasts.soa.org/products/actuarial-innovation-and-technologyupdate-on-recent-research#tab-product_tab_speaker_s.

The video features Neil Raden who is the author of ethical use of AI for Actuaries. Alongside him , it features Kevin Pledge who is CEO of Acceptiv , FSA,FIA and chair of Innovation and Research Committee of SOA. We discuss about the issue of ethics and about the use of new data sources in the recent Emerging issues in Underwriting Survey Report by IfOA.