Link: https://www.kansascityfed.org/documents/8337/JH_paper_Sufi_3.pdf

Graphic:

Excerpt:

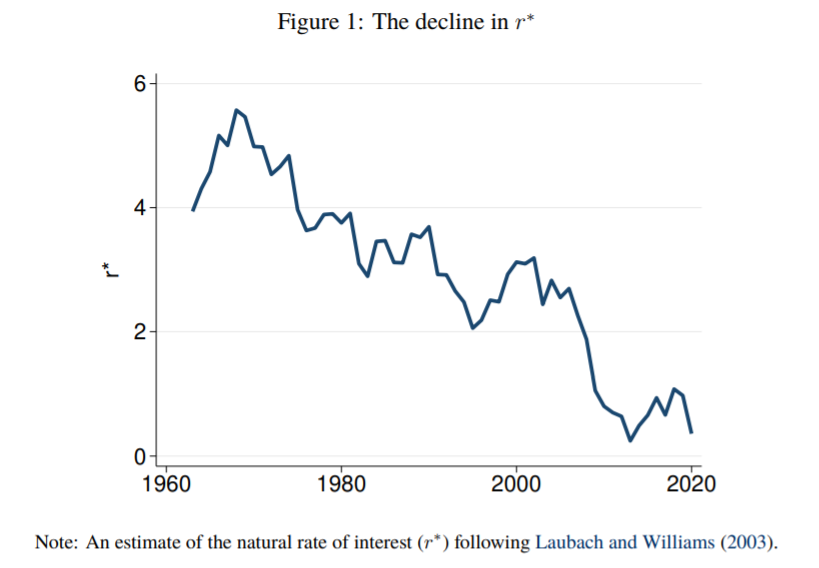

Downward pressure on the natural rate of interest (r∗) is often attributed to an increase in saving. This study uses microeconomic data from the SCF+ to explore the relative importance of demographic shifts versus rising income inequality on the evolution of saving behavior in the United States from 1950 to 2019. The evidence suggests that rising income inequality is the more important factor explaining the decline in r∗. Saving rates are significantly higher for high income households within a given birth cohort relative to middle and low income households in the same birth cohort, and there has been a large rise in income shares for high income households since the 1980s. The result has been a large rise in saving by high income earners since the 1980s, which is the exact same time period during which r∗ has fallen. Differences in saving rates across the working age distribution are smaller, and there has not been a consistent monotonic shift in income toward any given age group. Both findings challenge the view that demographic shifts due to the aging of the baby boom generation explain the decline in r∗.

.

Author(s): Atif Mian, Ludwig Straub, Amir Sufi

Publication Date: August 2021

Publication Site: Kansas City Federal Reserve