A Pennsylvania man who stole $194,000 of retirement benefits paid to his deceased father was sentenced today to five years in prison and ordered to pay full restitution, New York State Comptroller Thomas P. DiNapoli, the United States Attorney for the Eastern District of Pennsylvania Jacqueline C. Romero, the Inspector General for the Social Security Administration Gail S. Ennis, the United States Postal Inspection Service and the Federal Bureau of Investigation announced.

From October 2017 through October 2022, Timothy Gritman, 57, stole $110,897 in pension benefits from the New York State and Local Retirement System and $83,188 in Social Security benefits. He pleaded guilty to wire fraud and Social Security fraud charges in February.

…..

New York state pensioner Ralph Gritman retired from the Nassau County Clerk’s Office in 1992 and moved to Wyoming from Pennsylvania with his son, Timothy Gritman, in August 2017. In September 2017, Medicare records showed he went to a hospital emergency room in Wyoming. This was the last existing record of the father.

The father and son shared a joint bank account where Ralph’s retirement benefits were electronically deposited. Both Ralph Gritman’s pension and Social Security benefits were to cease upon his death, but Timothy Gritman concealed his father’s death in order to continue to receive his retirement benefits. In his attempts to impersonate his deceased father, he used makeup to whiten his hair and eyebrows.

Publication Date: 14 Feb 2024

Publication Site: Office of the NY State Comptroller

The primary responsibility of the $8.4 billion Philadelphia pensionfund is to assure the continuing financial security promised to city workers upon retirement. The welfare of city employees, along with all Philadelphians, depends on the economic and social well-being of the city itself. Therefore, the Philadelphia Public Banking Coalition has proposed that the city pension fund invest $168 million, 2% of its portfolio, in local economically targeted investments to fund projects that benefit Philadelphians.

These investments would address policy goals while achieving returns as high or higher than many of the fund’s current asset classes. Currently, the 2023 pension fund investment policy describes risky investments in options, futures, forwards, and swap agreements. And there’s a precedent for public policy considerations, for example, in limitations on investments in Russian companies, private prisons, and arms manufacturers. The current portfolio exhibits a strong real estate focus but without preference for Philadelphia projects.

Below are just a few of the possible opportunities for targeted investments that would strengthen the health of Philadelphia’s economy.

Author(s): Stan Shapiro and Peter Winslow, For The Inquirer

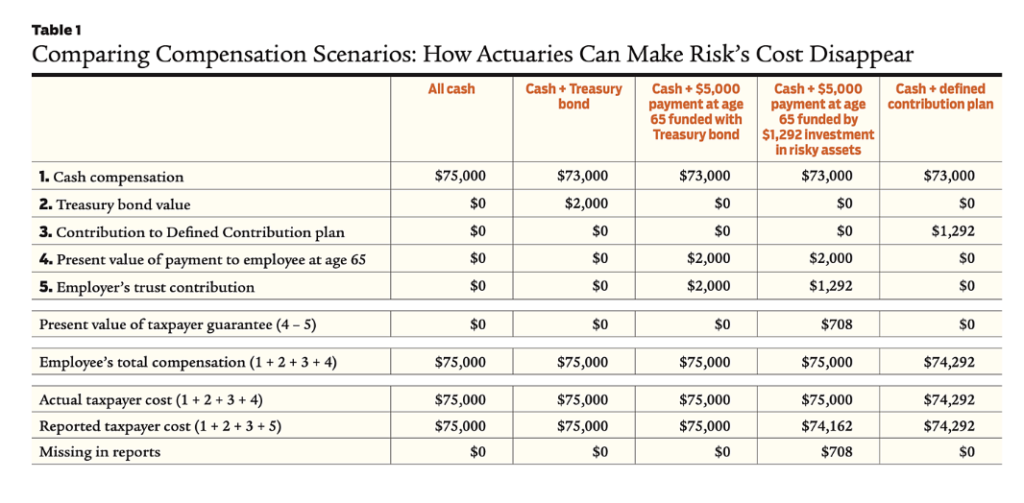

To appreciate the significance of using inappropriate discounting, consider this example: A 45‐year‐old public sector employee earns $75,000 per year with no pension plan or other benefits. To help secure her retirement, her employer considers changing her compensation to $73,000 in salary plus a U.S. Treasury zero‐coupon bond that pays $5,000 in 20 years. The bond is selling in the market at $2,000. The Treasury bond’s implicit annual “discount rate” is thus 4.69 percent, i.e., $2,000 plus 4.69 percent interest compounded for 20 years equals $5,000.

The total compensation cost to the employer would remain $75,000. The employee, in turn, has three options:

She can sell the bond and be in an identical position as before.

She can accept her employer’s nudge and keep the bond until retirement.

She can sell the bond and invest the $2,000 in other assets, e.g., stocks, in the hope of generating additional retirement income, albeit taking the risk that she may end up with less than $5,000.

Now suppose the public employer decides to be more paternalistic. Instead of giving the employee the Treasury bond worth $2,000, it promises her that in 20 years it will pay her $5,000. To fund this liability, the employer could deposit the $2,000 in a trust and have the trust buy the Treasury bond. The promise would then be fully funded by the trust. In 20 years, the Treasury bond would be redeemed for $5,000 and the proceeds forwarded to the employee. In the intervening 20 years, before the bond redemption and payment to the employee, the value of the future payment would increase with the passage of time, and increase (or decrease) as market interest rates decrease (or increase). But the value of the bond held in the trust would change identically to the liability, and the contractual obligation to pay $5,000 at age 65 would remain fully funded at every instant until paid, regardless of what happens in financial markets. Ignoring frictional costs and taxes, the employer’s cost of those actions would be the same as if it had paid the employee $75,000 in cash. And the employee’s total compensation would still be $75,000: $73,000 in cash plus a promise worth $2,000.

But instead of contributing the $2,000 and using it to buy the bond, the public employer could hire a public pension actuary and invest any trust contributions in a “prudent diversified” portfolio including assets, like equities, exposed to various market risks. The actuary would attest that the “expected” annual earnings of the portfolio over the long term is 7 percent (according to a sophisticated financial model). The actuary would then use the 7 percent to discount the $5,000 future payment and certify that the “cost” to the employer is $1,292, which is 35 percent less than the $2,000 cost of the Treasury bond. The actuary would certify that if the employer contributes the $1,292, its benefit obligation is “fully funded” because, if the trust earns the “expected return” of 7 percent (50 percent probable, after all), the $1,292 will accumulate to $5,000 in 20 years. The public employer can then claim it has saved taxpayers $708 ($2,000 – $1,292) by investing in a prudent diversified asset portfolio.

The question is, does it really cost only $1,292 to provide the same value as a $2,000 Treasury bond? Is $1,292 invested in the riskier portfolio worth the same as a Treasury bond that costs $2,000? Of course not. If it is possible to spin $1,292 of straw into $2,000 of gold, why would the government employer stop at pensions? Why not borrow as much as possible now and invest the proceeds in a prudent diversified portfolio expected to earn 7 percent and use the “expected” gains from taking market risk to pay for future general government expenditures?

The public employer is providing a benefit worth $2,000—a guarantee—and hoping to pay for it with $1,292 invested in a risky portfolio. The $708 difference represents the value of the guarantee that taxpayers will make good on any shortfall when the $5,000 comes due. The cost to taxpayers in total is still $2,000, but $708 is being taken from future generations by the current generation in the form of risk. Risk is a cost (precisely $708 in this example). Its price reflects the possibility as viewed by the market that future taxpayers ultimately may have to pay nothing at all if things go well, or a significant sum if they don’t.

Suppose the employer takes this logic one step further and, rather than promising $5,000 in 20 years, it contributes $1,292 to a defined contribution plan that invests in the same prudent diversified portfolio on the theory that the employee will be breaking even because the $1,292 is “expected” to accumulate to $5,000. The employee would be correct to view that as a cut in pay. The $708 cost of risk is shifted to the employee, reducing her compensation, instead of being borne by future taxpayers as in the case of the defined benefit plan.

The employee might complain. Future taxpayers cannot.

The only way for the employer to keep the employee whole with $73,000 of cash compensation plus a defined contribution plan is to contribute $2,000 to the plan. Whether it is invested in the Treasury bond or in riskier assets in the hope of higher returns, the value of her total compensation would still be $75,000.

Table 1 summarizes all these scenarios. The fourth column is the analog of public pension plans. Both the reported annual cost for the future $5,000 payment ($1,292) and the reported total compensation ($74,292) are understated. Investment professionals are paid well for managing risky assets for which high expected returns can be claimed. The actuary collects a fee. The employee has the value of the guarantee and bears none of the market risk being taken. Along with a happy employee, the public employer gets to report an understated compensation cost, freeing up money for other budget items. It’s good for all involved—except for the taxpayers on the hook for $708 in costs hidden by using the 7 percent discount rate.

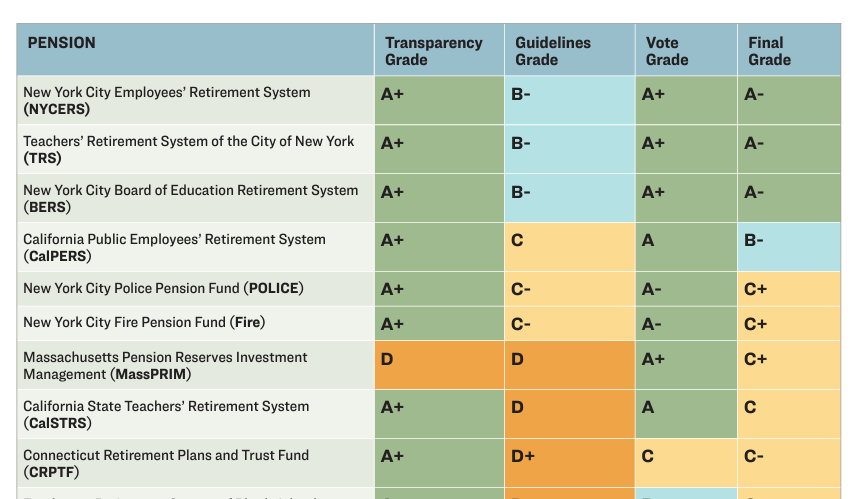

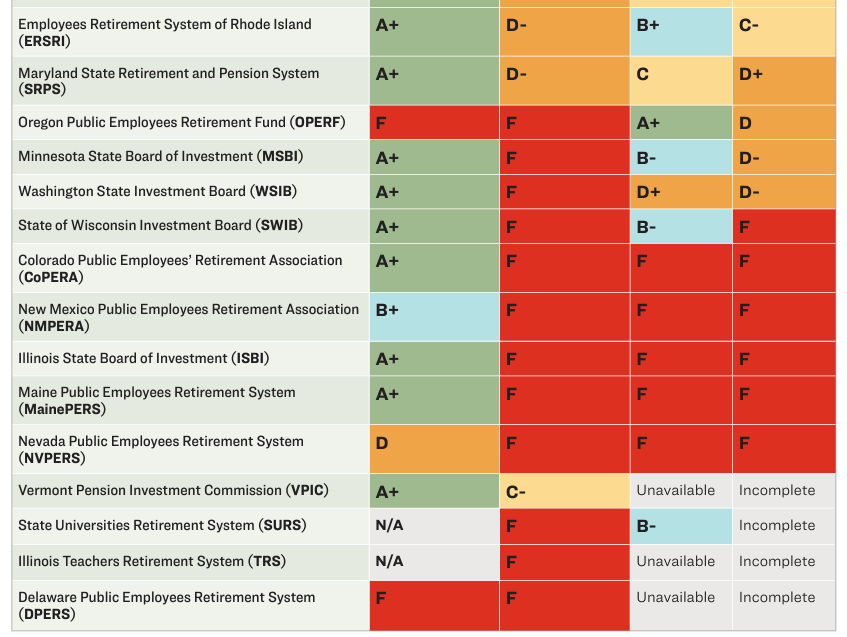

“Too few” public pension funds are addressing climate-related financial risk when it comes to proxy voting, according to a report released Jan. 23 by nonprofit organizations Sierra Club, Stand.earth and Stop the Money Pipeline.

The report, “The Hidden Risk in State Pensions: Analyzing State Pensions’ Responses to the Climate Crisis in Proxy Voting,” looked at 24 public pension funds with a collective $2 trillion in assets, including the $241.7 billion New York City Retirement Systems and state pension funds in California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont, Washington and Wisconsin.

The pension funds were graded on their proxy-voting guidelines, proxy-voting records, and data transparency.

On proxy-voting guidelines, no pension system received an A grade, but three of the five New York City pension funds covering city employees, the Board of Education and teachers, earned a B for addressing systemic risk and climate resolutions. Half of the 24 pension funds studied earned an F.

….

“The findings of this analysis are clear: Far too few state pensions are taking adequate steps to address climate-related financial risks and protect their members’ hard-earned savings, raising serious concerns about their execution of fiduciary duty,” the report’s executive summary said.

….

Amy Gray, associate director of climate finance for Stand.earth, said it is disappointing to see many funds not using proxy-voting strategies to address the financial risks of climate change. “This report is a stark reminder that pension funds can — and must — do so much more to wield their massive investor power,” Gray said in the news release.

A first-of-its-kind report, the Hidden Risk analyzes the proxy voting records and proxy voting guidelines of the 19 public pensions that are in states where a state financial officer has indicated it is a priority issue both to advocate for more sustainable, just, and inclusive firms and markets , and to protect against climate risk.

Ahead of the 2024 shareholder season, a first-of-its-kind report “The Hidden Risk in State Pensions: Analyzing State Pensions’ Responses to the Climate Crisis in Proxy Voting,” from Stand.earth, Sierra Club and Stop the Money Pipeline, analyzes proxy voting records, proxy guidelines, and voting transparency of 24 public pension funds in the USA collectively representing over $2 trillion in assets under management (AUM).

These pensions are based in states where a state financial officer is a member of For the Long Term, a network that advocates for more sustainable, just, and inclusive firms and markets and strives to protect markets against climate risk.

The pensions analyzed include the pension systems of New York City and the states of California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont, Washington, and Wisconsin.

Republican lawmakers in New Hampshire are seeking to make using ESG criteria in state funds a crime in the latest attack on the beleaguered investing strategy.

Representatives led by Mike Belcher introduced a bill that would prohibit the state’s treasury, pension fund and executive branch from using investments that consider environmental, social and governance factors. “Knowingly” violating the law would be a felony punishable by not less than one year and no more than 20 years imprisonment, according to the proposal.

“Executive branch agencies that are permitted to invest funds shall review their investments and pursue any necessary steps to ensure that no funds or state-controlled investments are invested with firms that invest New Hampshire funds in accounts with any regard whatsoever based on environmental, social, and governance criteria,” the bill said.

The New Hampshire Retirement System “shall adhere to their fiduciary obligation and not invest with any firm that will invest state retirement system funds in investment funds that consider environmental, social, and governance criteria, as the investment goal should be to obtain the highest return on investment for New Hampshire’s taxpayers and retirees,” the bill said.

Investors aren’t allowed to consider governance! Imagine if this was the law; imagine if it was a felony for an investment manager to consider governance “with any regard whatsoever.”

….

I’m sorry, this is so stupid. “ESG” is essentially about considering certain risks to a company’s financial results: You might want to avoid investing in a company if its factories are going to be washed away by rising oceans, or if its main product is going to be regulated out of existence, or if its position on controversial social issues will cost it sales, or if its CEO controls the board and spends too much corporate money on wasteful personal projects. Obviously ESG in practice is also other, more controversial things:

If you care about the environment, social issues, etc., you might want to invest in companies that you think are environmentally or socially good, whether or not they are good financial investments.

You might incorrectly convince yourself that the stuff you think is environmentally or socially good is also good for the bottom line: You might have a wishful estimate of how quickly the world will transition away from fossil fuels, to justify your desire not to invest in oil companies. You might tell yourself “this company’s stance on social issues will cost it lots of customers” when really the customers don’t care, but you do.

But if you make it a crime for investors to consider certain financial risks then you get too much of those risks.

In particular, I suspect, you get too much governance risk. If every investor tomorrow said “okay we don’t care about the environment,” most companies probably wouldn’t ramp up their pollution: Their executives probably don’t want to pollute unnecessarily, polluting probably wouldn’t help the bottom line, and many companies just sit at computers developing software and couldn’t pollute much if they wanted to. But if every investor tomorrow said “okay we don’t care about governance,” then, I mean, “governance” is just a way of saying “somebody makes sure that the CEO is doing a good job and doesn’t pay herself too much.” If the investors don’t care about that, then a lot of CEOs will be happy to give themselves raises and spend more time on the corporate jet to their vacation homes.

In May, the United Kingdom’s version of the Securities and Exchange Commission will begin enforcing its pledge to crack down on so-called greenwashing by companies wishing to trade on the label of being green-friendly.

The Financial Conduct Authority’s rules, announced in late November, come as U.S. traders await stronger regulations from the SEC. That body moved in September to curb misleading marketing practices by requiring 80 percent of funds that claim to be “sustainable,” “green,” or “socially responsible” to actually be so.

The sustainability disclosure requirements are now deemed a necessity after regulators found “environmental, social, and corporate governance” analysts at Goldman Sachs and Germany’s DWS Group were promoting investments that were not as ESG-friendly as they claimed.

“The portfolio managers weren’t necessarily doing all of the work that they said they were doing,” the associate director of sustainability research for Morningstar Research Services LLC, Alyssa Stankiewicz, said. “They didn’t have documentation or data maybe related to the ESG-ness of these investments.”

At the same time as ESG-friendly firms are facing accusations of insincerity, they’re also coming under pressure from state pension funds in states with Republican-controlled governments that don’t want their employees’ retirement funds affected by what they view as politicized, left-leaning investing strategies.

A Delaware Chancery Court has appointed pension funds from New York City and from Oregon as the lead plaintiffs in a shareholder lawsuit that alleges Fox Corp. breached its fiduciary duty by exposing itself to defamation lawsuits during its coverage of the 2020 U.S. presidential election.

In September 2023, New York City’s five public pension funds, as well as the Oregon Investment Council and the Oregon Public Employees Retirement Fund, filed shareholder derivative lawsuits against Fox for breach of fiduciary duty. The lawsuits allege Fox’s board of directors knew that Fox News was promoting former President Donald Trump’s false claims that he was the true winner of the 2020 election without regard for whether the assertions were true and thus created significant exposure to defamation charges.

In April, Fox settled a $787 million defamation lawsuit brought by the voting machine company Dominion Voting Systems after Fox broadcasters falsely alleged Dominion was involved in altering results during the 2020 presidential election. Fox also faces a $2.7 billion lawsuit from voting machine company Smartmatic USA Corp.

This past week, I was introduced to another vibrant Facebook group pushing for reform of the Minnesota state pension system. While the name of the group, Pension Reform for Tier II Minnesota Public Educators, may not be catchy, with nearly 19,000 members it also appears to be a formidable advocate. In the group’s words:

….

It’s no secret that most of our nation’s public pension funds are grossly underfunded. Not surprising, the single greatest concern of pension participants today is whether the pensions they rely upon for their retirement security are prudently managed and if pensioners will receive all the benefits they have been supposedly promised.

While for over two decades I have implored unions to get actively involved in scrutinizing the management of pension investments—serving a watchdog function which pension boards are ill-equipped to perform—rarely have I been successful in persuading these unions that the best way to preserve pensions is to expose and address problems, not hide them. Unions tend to believe that any criticism of pensions will only lead sponsors to no longer offer them to workers.

Former New York Mayor Rudy Giuliani said he regrets not taking a city pension now that he’s facing a $148m civil court payout for defaming a pair of Georgia election workers.

The former mayor has since filed for bankruptcy, according to the New York Post.

Empire Centre for Public Policy, a taxpayer watchdog group in New York, found no evidence of Mr Giuliani ever filing to receive a pension.

Had he applied, he would have been eligible for approximately $26,000 per year once he turned 62.

The former mayor would have an extra $442,000 in his coffers if he had applied for a pension.

When The New York Post asked him why he never took a pension, he suggested he was “giving back to the city I love.”

“Although I would like to take it now,” he added.

The former mayor then admitted that he also didn’t “know how to go about it.”

He also is not receiving a federal pension for the time he spent working as Manhattan’s US Attorney and for other government work he performed.

Although neither is considered healthy in terms of pension funding, it does mark a turnaround following years of increasing unfunded liabilities and, therefore, increasing annual payments toward the debt, increased taxes and contract negotiations with state employees that increased their contributions and lowered benefits to make up the difference.

Former Gov. Dannel Malloy had stated that Connecticut’s tax increases in 2011 and 2015 went entirely to pay for the escalating cost of state employee and teacher pensions.

While the year-over-year change seems somewhat small, the change in funding ratio over the past eight years is much more substantial. In 2016, SERS was only 36 percent funded with $20.3 billion in unfunded liabilities. While SERS continues to have roughly $20 billion in unfunded liabilities, its assets have grown by $10 billion during that period, significantly increasing the funding ratio.

Meanwhile, the unfunded liability for TRS has increased by $3.3 billion over that same time frame, but assets increased by nearly $8 billion, increasing the funded ratio from 56 percent to nearly 60 percent. The total unfunded debt for TRS currently stands at $16.4 billion.

When launching GFC in 2011 it was my hope that we would see meaningful pension reform by 2020, but we have failed to achieve that objective and the negative consequences for public services and taxpayers have been enormous. As evidence, just look at the four-fold explosion in annual pension spending by the Los Angeles Unified School District this year compared to ten years ago:

Pension spending will keep exploding. That’s because California’s public pension funds still have inadequate ratios of assets to liabilities despite more than $200 billion of pension contributions and a doubling of the stock market since 2013-14.

Pension reform is not the only thing I got wrong. I thought it would be even easier to terminate California’s unnecessary spending on other post-employment benefits (OPEB), especially after the creation of Obamacare and that program’s generous federal healthcare subsidies, but LAUSD alone is spending $365 million on OPEB this school year. Together, pensions and OPEB consume one of every six LAUSD dollars, leaving that much less for classrooms and salaries.