Graphic:

Excerpt:

The “tax exclusion” for employer‐sponsored health insurance shields workers from paying income or payroll taxes on such benefits. The exclusion is an accident of history that predates modern health insurance and is roughly as old as the income tax itself. It fuels excessive health insurance coverage, medical spending, and health care prices and ties health insurance to employment. It has required Congress to intervene countless times to address problems it creates.

The exclusion requires a worker to let her employer control a sizable share of her earnings, to enroll in a health plan that is likely not her first choice, and to pay the remainder of the premium out of pocket. Overall, the tax code effectively threatens U.S. workers with $352 billion in additional taxes in 2022 if they do not let their employers control $1 trillion of their earnings. The additional tax that workers pay if they do not accept those terms constitutes an implicit penalty.

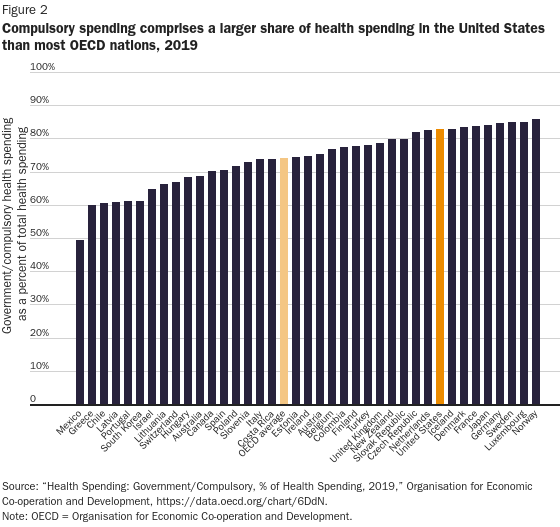

The tax code thus limits a worker’s ability to make her own health decisions. In the United States, compulsory health spending accounts for 83 percent of overall health spending, the ninth highest share among 34 advanced nations. The tax exclusion is the single largest contributor to compulsory health spending.

Reforming the exclusion would free U.S. workers to control $1 trillion of their earnings that employers currently control, give consumers more health care choices, and make health care more accessible. Building on the bipartisan success of tax‐free health savings accounts appears to present the best politically feasible opportunity for reform. The United States will not have a consumer‐centered health sector until workers control the $1 trillion of their earnings that the exclusion forces them to let employers control.

Author(s): Michael Cannon

Publication Date: 24 May 2022

Publication Site: Cato