Graphic:

Excerpt:

As corporate bonds are mainly fixed rate, their relative value will decrease as floating rate investments

become more attractive with higher benchmark rates. That is, bond prices will fall as yields rise to make

them more attractive, given that their fixed-rate coupons will be lower. About half of insurer bond

investments are corporate bonds, and the vast majority of U.S. insurer corporate bond investments are

investment grade credit quality. From January 2022 to January 2023, the ICE Bank of America (BofA)

Investment Grade Corporate Bond Index, which measures the performance of investment grade

corporate debt, was down by about 14%.

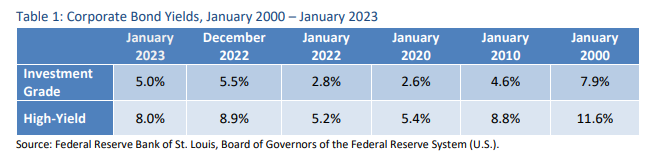

Corporate bond yields have increased significantly since the beginning of 2022 with rising interest rates

and widening credit spreads. As of year-end 2022, investment grade and high-yield corporate bond

yields averaged 5.5% and 8.9%, respectively (refer to Table 1). Investment grade yields increased by

approximately 270 bps during 2022, while speculative-grade yields increased by about 370 bps.

Author(s): Jennifer Johnson and Michele Wong

Publication Date: 23 Feb 2023

Publication Site: NAIC Capital Markets Special Report