Graphic:

Excerpt:

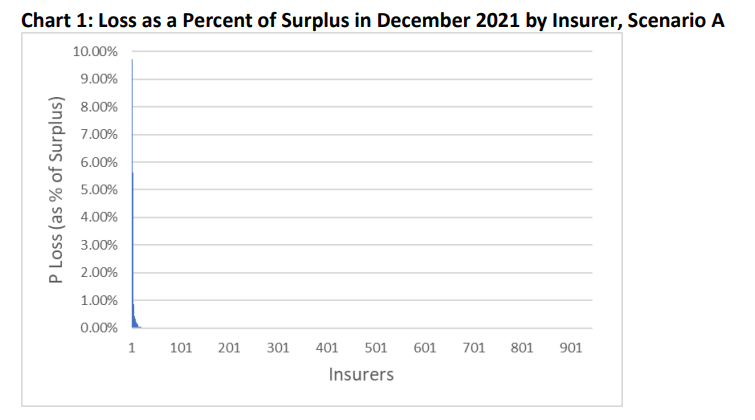

The stress test analysis found that 1,114 U.S. insurers, with a surplus of about $1.2 trillion, held some

amount of CLO tranches modeled. Similar to last year’s stress testing results, we found that the losses on

insurers’ CLO investments that were modeled, even in the stressed scenarios, were highly concentrated.

To understand the impact of potential losses on insurers, principal loss (compare with Table 7) for

scenarios A, B, and C was divided by each insurer’s year-end 2021 total surplus. For each scenario, the

principal loss as a percentage of total surplus for each of the 1,114 insurers was sorted from highest to

lowest. Then the insurer with the largest percentage loss was referenced as “Insurer 1,” the insurer with

the second largest percentage loss was referenced as “Insurer 2,” and so on until the smallest percentage loss, which was referenced as “‘Insurer 1,114” (x-axis). Please note the difference in the scale of the y-axis

in Charts 1, 2, and 3.

Chart 1 shows the distribution of losses as a percentage of surplus for December 2021’s Scenario A.

Although the bulk of insurers show no losses, 49 of the 1,114 insurers experienced losses in this

scenario. Intuitively, the losses were derived primarily from CCC-rated CLO tranches. The largest loss as

a percentage of surplus under Scenario A was 9.72%. Similar to the analysis for year-end 2020, no

insurers experienced double digit losses.

Author(s): Jean-Baptiste Carelus, Eric Kolchinsky, Hankook Lee, Jennifer Johnson, Michele Wong, Azar Abramov

Publication Date: Jan 2023

Publication Site: NAIC Capital Markets Special Reports