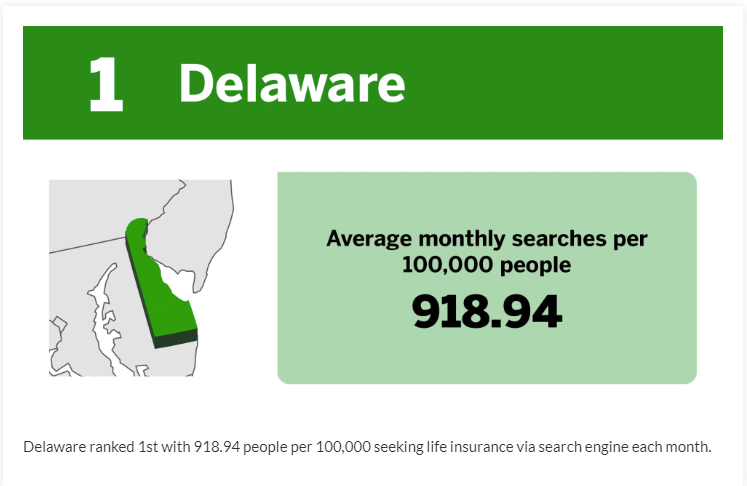

To determine where residents are most concerned about life insurance, Beca Life ranked them by monthly online searches for terms related to the product, based on data from Google Keyword Planner. The total number of monthly average searches in each state was compared against its population, to determine the average monthly searches per 100,000 people.

The top five states have an average of 852.84 people per 100,000 seeking life insurance via search engine each month.

The Society of Actuaries (SOA) Research Institute’s Mortality and Longevity Strategic Research Program Steering Committee issued a call for essays to explore the application of artificial intelligence (AI) to mortality and longevity. The objective was to gather a variety of perspectives and experiences on the use of AI in mortality modeling, forecasting and prediction to promote discussion and future research around this topic.

The collection includes six essays that were accepted for publication from all submissions. Two essays were chosen for prizes based on their creativity, originality, and likelihood of further thought on the subject matter.

Author(s): multiple

Publication Date: September 2024

Publication Site: Society of Actuaries, SOA Research Institute

The Committee on Life Insurance Mortality and Underwriting Surveys of the Society of Actuaries sent companies a survey in May of 2019 on mortality improvement practices as of year-end 2018. The survey results were released in January 2022. The survey was completed by respondents prior to the onset of COVID-19. The present report provides an opportunity to update the results for pandemic-based changes and compare the before and after surveys. The 2022 survey was opened in March 2022 and closed by the end of April. Thirty-five respondent companies participated in this survey, with 29 from the U.S. and six from Canada. This group was further divided between direct writers (26) and reinsurers (nine). This survey focused on the use of mortality improvement and how it has changed for financial projection and pricing modeling following the initial stages of COVID-19. Details regarding assumptions and opinions on mortality improvement in general were asked of the respondents. National Association of Insurance Commissioners discussions on mortality improvement factors due to COVID-19 for reserving purposes have taken place, but this survey was conducted before any adjustments reacting to them. Seventy-four percent (26 of 35) of respondents indicated using durational mortality improvement assumptions in their life and annuity pricing and/or financial projections. Moreover, of those that used durational mortality improvement assumptions, attained age and gender were the top two characteristics in which assumptions varied. Respondents were asked to indicate the different limitations when applying durational mortality improvement assumptions. The Survey found that the most common lowest and highest attained age to which durational mortality improvement was applied were 0 and about 100, respectively. The lowest and highest durational mortality improvement rate ranged from -1.50% (deterioration) to 2.80% (improvement). The time period in which the mortality improvement rates were applied ranged from 10 to 120 years, but this varied between life (10/120) and annuities (30/120). The most common time period was 20 to 30 years for life; less consensus was seen for annuities. Analysis is provided in Appendix C for instances when highlights are shared in the body of the report.

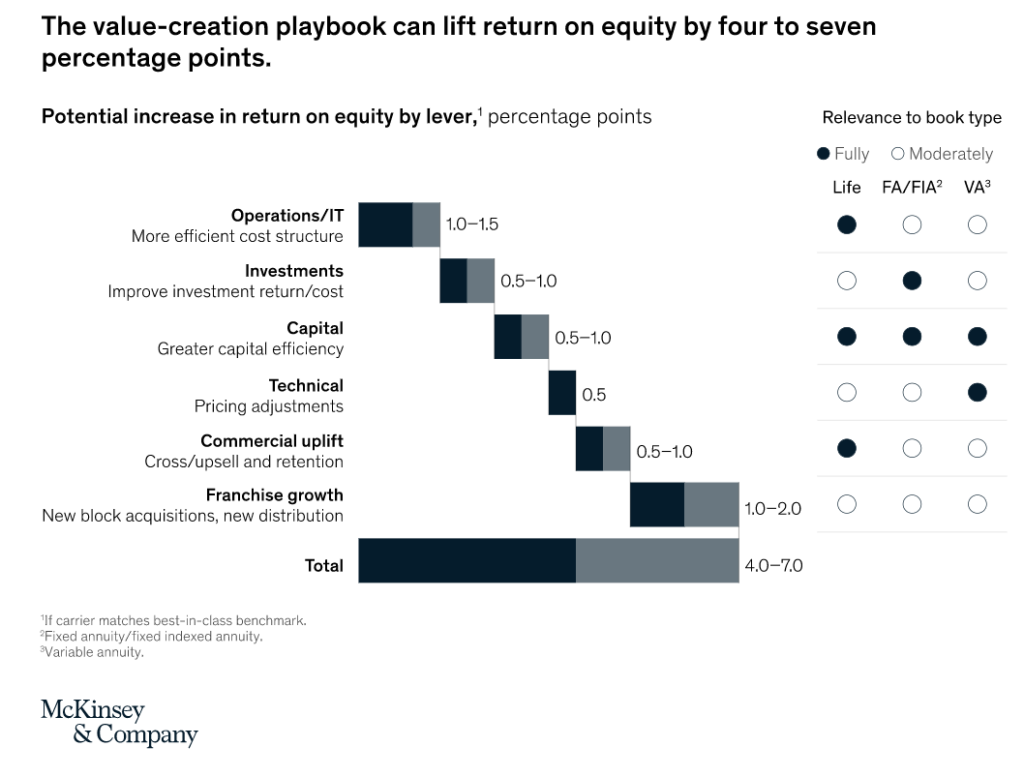

Once they’ve acquired a book, firms can turn their attention to driving value. Building on our guidelines for closed-book value creation, owners have six levers that can collectively improve ROE by up to four to seven percentage points (exhibit):

Investment performance: optimization of the SAA and delivery of alpha within the SAA

Capital efficiency: optimization of balance-sheet exposures—for example, active management of duration gaps

Operations/IT improvement: reduction of operational costs through simplification and modernization

Technical excellence: improvement of profitability through price adjustments, such as reduced surplus sharing

Commercial uplift: cross-selling and upselling higher-margin products

Franchise growth: acquiring new blocks or new distribution channels

Most PE firms view the first lever, investment performance, as the main way to create value for the insurer, as well as for themselves. This lever will grow in importance if yields and spreads continue to decline. Leading firms typically have deep skills in core investment-management areas, such as strategic asset allocation, asset/liability management, risk management, and reporting, as well as access to leading investment teams that have delivered alpha.

Capital efficiency is also well-trod ground, and for private insurers it presents a greater opportunity given their different treatment under generally accepted accounting principles, (GAAP), enabling them to apply a longer-term lens and reduce the cost of hedging. However, most firms have yet to explore the other levers—operations and IT improvement, technical excellence, commercial uplift, and franchise growth—at scale. Across all these levers, advanced analytics can enable innovative, value-creating approaches.

Author(s): Ramnath Balasubramanian, Alex D’Amico, Rajiv Dattani, and Diego Mattone

The authors examine 19 factors to determine which were most closely linked to permanent and term life insurance premiums sold in the United States in 2020. With spatial regression analysis using multi-scale geographically weighted regression (MGWR) approach, the authors find the following 5 covariates to be the most statistically significant for and positively correlated with permanent insurance sold: household income, percentage of the population that is African American, education, health insurance, and Gini index (a statistical measure of wealth inequality). For term insurance sold, the 5 most significant covariates are household income, education, Gini index, percentage of households with no vehicles, and health insurance. Their relationships with term insurance sold are positive except for the percentage of households with no vehicles.

Author(s):

Wilmer Martinez Kyran Cupido Petar Jevtic Jianxi Su

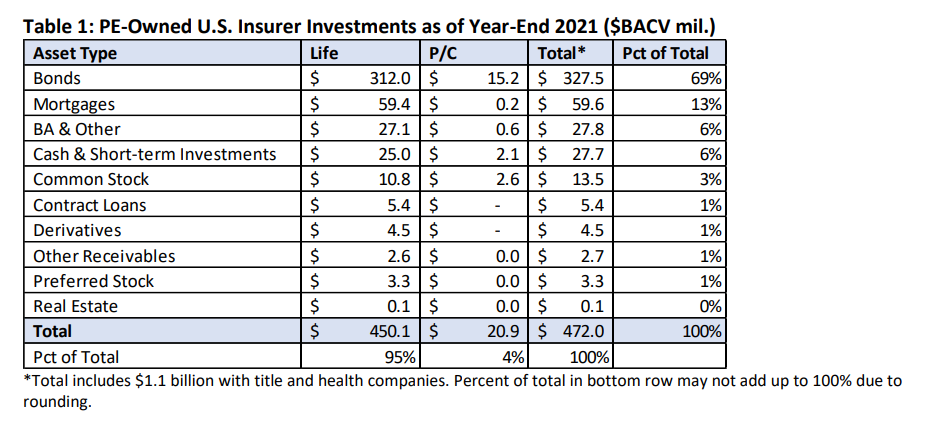

The BACV of total cash and invested assets for PE-owned insurers was about 6% of the U.S. insurance industry’s $8.0 trillion at year-end 2021, down slightly from 6.5% of total cash and invested assets at year-end 2020. The number of PE-owned insurers, however, increased to 132 in 2021 from 117 in 2020, but they were about 3% of the total number of legal entity insurers at both year-end 2021 and year-end 2020.

Consistent with prior years, U.S. insurers have been identified as PE-owned via a manual process. That is, the NAIC Capital Markets Bureau identifies PE-owned insurers to be those who reported any percentage of ownership by a PE firm in Schedule Y, and other means of identification such as using third-party sources, including directly from state regulators. As such, the number of U.S. insurers that are PE-owned continues to evolve.1 Life companies continue to account for a significant proportion of PE-owned insurer investments at year-end 2021, at 95% of total cash and invested assets (see Table 1). This represents a small decrease from 97% at year-end 2020 (see Table 2). Notwithstanding, there was a slight increase in PE-owned insurer investments for property/casualty (P/C) companies, to 4% at year-end 2021, compared to 3% the prior year. In addition, there was also a small increase in total BACV for PE-owned title and health companies’ investments, at about $1.1 billion at year-end 2021, compared to under $1 billion at yearend 2020.

Author(s): Jennifer Johnson and Jean-Baptiste Carelus

Publication Date: 19 Sept 2022

Publication Site: NAIC Special Capital Markets Reports

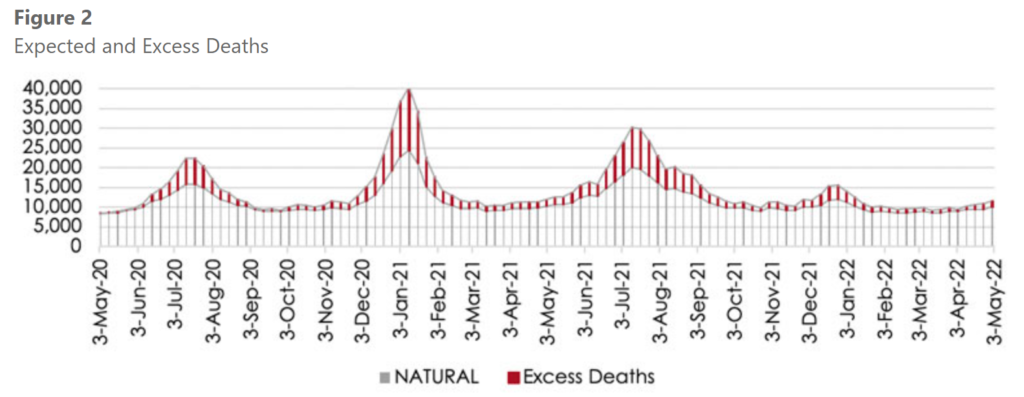

The impact of Covid-19 in South Africa in terms of excess deaths was substantial, when considering the reported excess deaths as published by the South African Medical Research Council (SAMRC).[4] Please note that in this article we will not further consider whether all excess deaths can be directly attributed to Covid-19, however, as per the article “Correlation of Excess Natural Deaths with Other Measures of the Covid-19 Pandemic in South Africa,”[5] it is estimated that 85 percent to 95 percent of excess natural deaths are attributable to Covid-19.

Based on the SAMRC excess deaths, taking the expected plus excess deaths as Actual and expected natural deaths as per their methodology as Expected, we observe an Actual versus Expected (AvE) ratio of 116 percent in 2020, a ratio of 131 percent in 2021, and a ratio of 113 percent in 2022 up to May 1. When we look at the AvE for each wave, we can see that the 2nd wave (predominantly Beta variant) and the 3rd wave (predominantly Delta variant), had the most severe impact on the general population (see figure 2 and figure 3)

It’s been 21 years since novelist Michael Peterson was on trial for the murder of his wife, Kathleen, but the case is still capturing the public’s attention—most recently in an HBO Max series, “The Staircase.”

….

The case also involved the potential for a large life insurance payout. Kathleen had a $1.4 million life insurance policy, which was due to be paid to Michael in the event of her death. Prosecutors said Peterson was hoping to use the payout to address his debt [1] , including $143,000 in credit card debt.

…..

Peterson signed away any claim to the life insurance proceeds during the trial. However, because of the slayer rule, Peterson wouldn’t have been able to collect any money. Under the slayer rule, anyone suspected of murder or plotting a murder is prevented from benefiting from the dead person’s life insurance policy. Instead, Kathleen’s biological daughter, Caitlin Atwater, and her daughter’s father, Fred Atwater, received the money. [2]

In the scope of insurance fraud, life insurance murders aren’t a huge occurrence but they do happen, says Matthew J. Smith, executive director of the Coalition Against Insurance Fraud. For instance, in 2017, Joaquin Shadow Rams Sr., was convicted of killing his 15-month-old son for insurance money. Rams had taken out a $500,000 life insurance policy on the boy soon after he was born, which Smith says, should have been a red flag.

1. Clients could swarm on life and annuity products with benefits guarantees like ants on a candy bar that fell under the picnic table.

Sales of products such as non-variable indexed annuities and non-variable indexed universal life insurance policies soar, as clients flocks to arrangements that can protect them against further drops in stock prices but help them share in gains if and when prices go back up.

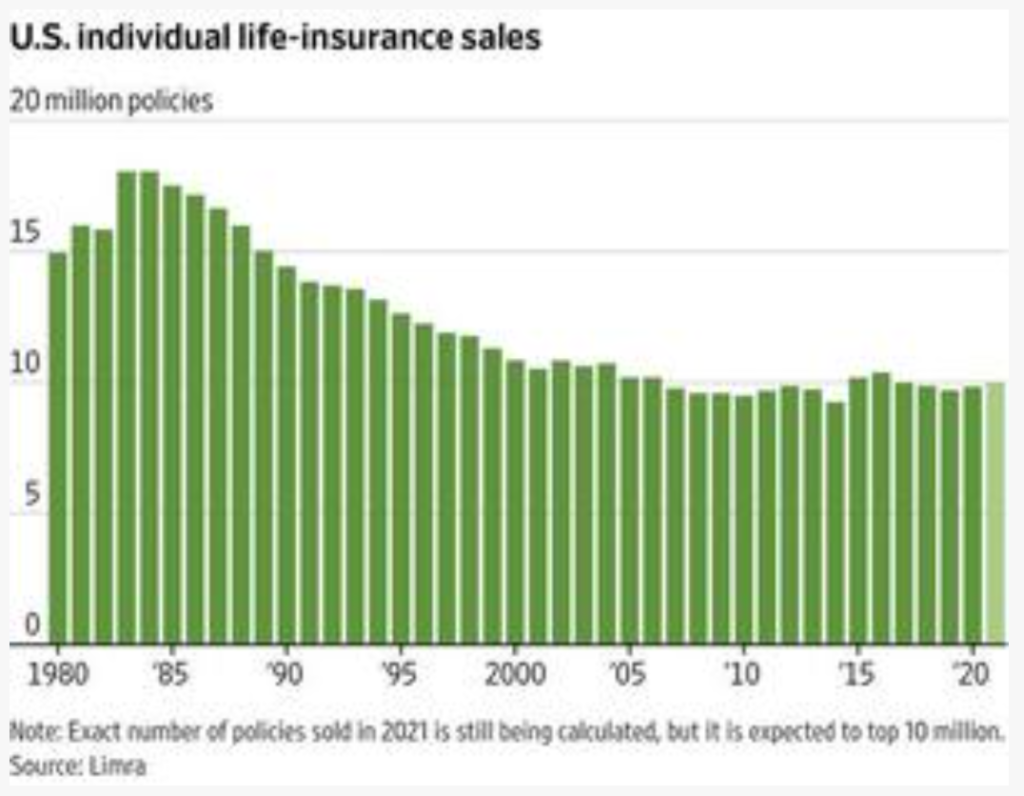

Americans went on a buying spree for life insurance in 2021, driven by concerns of death from the coronavirus pandemic.

Premium volume for new individual life-insurance policies surged 20% from 2020, while the number of policies issued rose 5%, the biggest year-over-year percentage gains since the 1980s, according to industry-funded research firm Limra.

“As we zero in on one million Americans who tragically lost their lives, it’s not a surprise that people are thinking about their own mortality and the impact on loved ones if anything were to happen to them,” said David Levenson, Limra’s chief executive.

The exact number of policies sold is still being calculated, but it is expected to top 10 million, Limra said. That milestone was last crossed in 2016. In 2020, an estimated 9.83 million policies were sold, up 1.7% from 2019.

COVID-19 returned to killing older Americans at a much higher rate than younger Americans in the first quarter, and that helped to hold down life insurers’ death claims.

The pandemic killed about 155,000 U.S. residents in the latest quarter. That was up from 127,000 in the fourth quarter of 2021, but down from 191,000 in the first quarter of 2021, according to statistics from the U.S. Centers for Disease Control and Prevention and other public and private sources.

Some life insurers and reinsurers that posted earnings last week skipped COVID-19 mortality details.

…..

MetLife: $230 million in world group life claims this quarter, down from $280 million a year earlier.

Hartford Financial: $96 million before taxes this quarter, down from $185 million a year earlier.

Unum: 1,400 deaths at an average of $55,000, or $77 million, down from 1,725 deaths at an average of $65,000, or $112 million, a year earlier.

Lincoln Financial: $53 million in group life claim claims and $18 million in group disability claims this quarter, down from $83 million in group life claims and $7 million in group disability claims a year earlier.

Voya: $35 million in group life claims this quarter, up from $29 million a year earlier.

High levels of Covid-19 deaths hurt fourth-quarter results in MetLife Inc.’s business of providing employer-sponsored life insurance as the Delta variant persisted in the U.S., but the outsize payouts were more than offset by unusually strong investment gains.

The New York company’s net income soared to $1.18 billion, compared with a year-earlier period that had been hurt by mark-to-market losses on financial hedges that aim to protect against falling interest rates. MetLife’s adjusted earnings, which analysts track as a measure of recurring profitability, were flat at $1.84 billion.

Another household-name insurer, Allstate Corp., reported a 70% drop in net income to $790 million, and a 50% decline in adjusted net income to $796 million, primarily driven by worsened car-insurance underwriting income. Accident volume increased on more-crowded roads, and inflation pushed repair costs higher.

Catastrophe costs were also higher. U.S. property insurers ended the year with two high-profile catastrophes: deadly tornadoes in and around Kentucky, and devastating wildfire between Denver and Boulder, Colo.