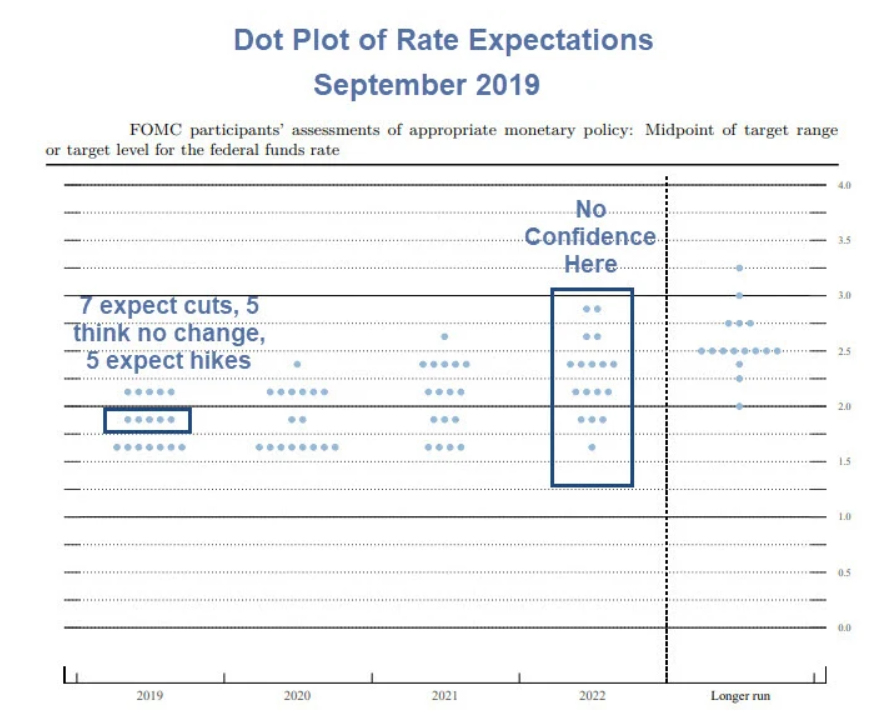

How many rate hikes are coming? The Fed thinks 6 by the end of 2023. I am unconvinced the Fed gets in any hikes in 2022 and certainly not 6 by the end of 2023.

These ridiculous predictions assume there will not be another recession in “the longer run”.

Central banks like to pretend they will hike, but by the time comes, they have delayed so long they find an excuse to no do so.

Possible excuses: A recession, stock market plunge, another pandemic, global warming, global cooling, or an asteroid crash.

Central banks will find some excuse to delay hikes. But the most likely excuse is a recession or stock market crash.

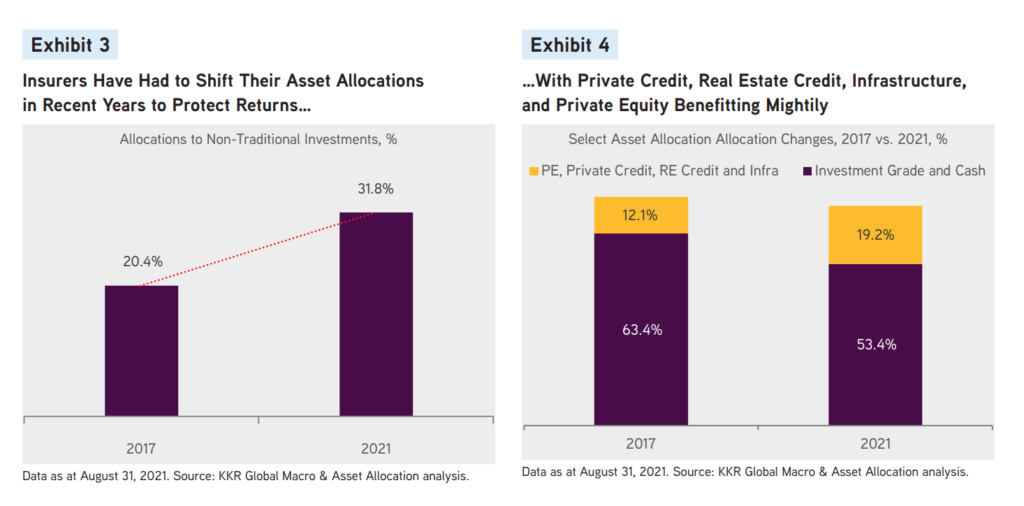

To compensate for the ongoing pressure on interest rates, CIOs participating in our survey have made substantive, structural shifts in their asset allocations. Why did they make this transition? We believe that CIOs are embracing complexity and the thoughtful use of illiquidity, as public market assets roll off and excess cash builds up. Improved asset-liability matching and more robust risk management have also helped, we believe. Reflective of these shifts, non-traditional investments, including Real Estate Credit and Structured Credit, collectively experienced almost a 1,200 basis point increase in market share. As a result, total

non-traditional investments now account for 31.8% of total portfolios surveyed, compared to 20.3% in 2017. As we detail below and in Exhibit 21, our work shows that 100% of the gain came at the expense of traditional public credit, which fell to 48.5% of portfolios surveyed, compared to 60.7% in 2017. Meanwhile, the allocation to Liquid Equities (predominantly by Property & Casualty and Reinsurers that typically favor Public Equities for liquidity) slipped to 5.5% from 9.1% over the same period. Cash as a percentage of assets is now at 4.9%, which is almost double the level it was the last time we did the survey. See below for full details on this increase but we think high cash balances are fueling thoughtful moves into longer duration assets. However, there is obviously more work to be done, as the supply of yielding, long-term assets remains limited.

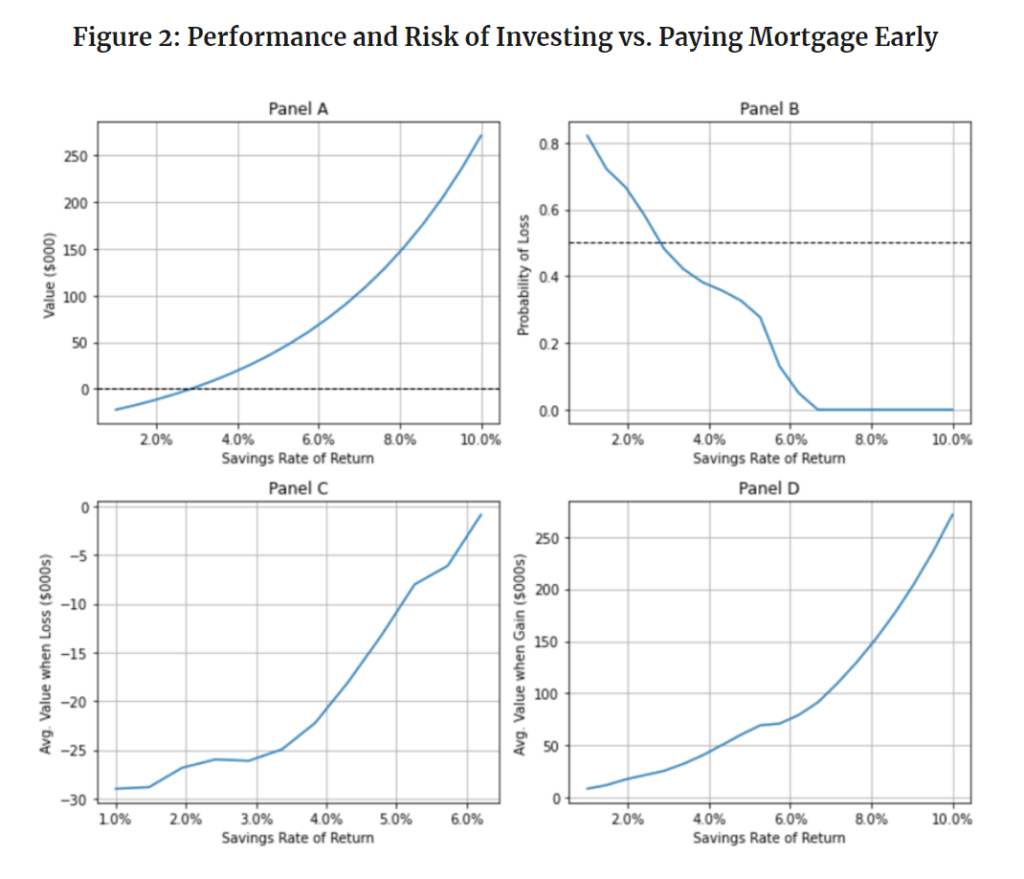

The concern with this exercise is its reliance on past returns. With interest rates near zero, significant economic growth is needed to generate market returns close to those experienced over the last 100 years – approximately 11% per annum. To explore the implications of different future investment performance, let’s repeat the process above by reducing the average return of historical stock returns while maintaining the same risk (i.e., volatility).

Panel A shows that as the return on Lena’s savings increases, i.e., we move from left to right along the horizontal axis, the value of investing the money relative to paying off the mortgage early increases. At a 3% savings return, the cost of her mortgage, Lena would be indifferent between saving extra money and paying down her mortgage early because both options lead to similar average savings balances after 30 years. Savings rates higher (lower) than 3% lead to higher (lower) savings for Lena if she invests her money as opposed to paying down her mortgage early. For example, a 5.5% average return on savings, half that of the historical return, leads to an extra $57,000 in after-tax savings if Lena invests the $210 per month as opposed to using it to pay down her mortgage more quickly.

Panel B illustrates the relative risk of the investment strategy. When the return on savings is 3%, the same as the cost of the mortgage, the choice between investing the money and paying down the mortgage comes down to a coin flip; there is a 50-50 chance that either option will lead to a better outcome. However, if future average market returns are 5.5%, for example, the probability that investing extra money leads to less savings than paying down the mortgage early is only 26%. For average returns above 6.5%, the probability that investing the extra money is a bad choice is zero. In other words, there hasn’t been a 30-year historical period in which the average stock market return was below 3%, even when the average return for the 100-year period was only 6.5%.

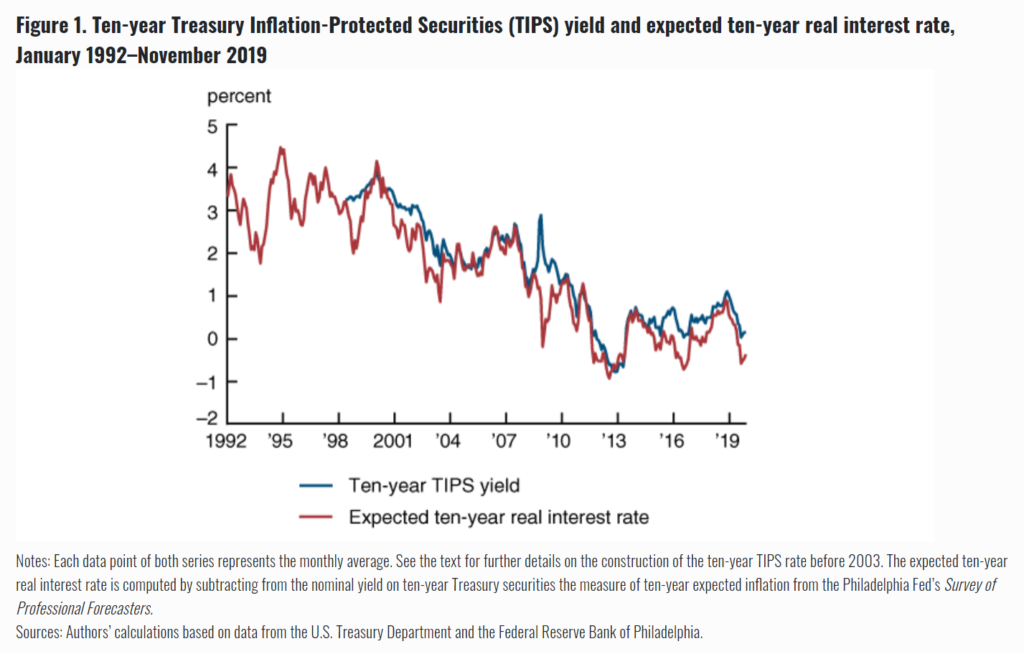

The first observation in the United States motivating the GSG hypothesis is the protracted decline in long-term real interest rates, as shown in figure 1. This figure depicts both a Treasury Inflation-Protected Securities (TIPS) rate and an expected long-term real interest rate, computed by subtracting from the nominal yield on ten-year Treasury securities the measure of ten-year expected inflation from the Survey of Professional Forecasters (SPF).8 From 2003 on, the TIPS rate is for the ten-year TIPS. Before 2003, we use a 30-year TIPS rate, data for which are available starting in 1998, subtracting 40 basis points from it to reflect the average term premium observed in the years when both the ten-year and 30-year TIPS are available. At the time Bernanke first articulated the GSG hypothesis, much of the focus was on Greenspan’s conundrum—that is, the continuing drop in long-term rates in 2004–05 despite repeated hikes in short-term rates during a strong economy. However, with the benefit of hindsight, the much longer-run, apparently secular nature of the drop in long-term real interest rates is evident. Very roughly, it seems fair to say that the ten-year real interest rate in the United States declined about 150 basis points between the latter half of the 1990s (when it averaged around 3.5 percent) and the prelude to the global financial crisis (when it averaged around 2 percent), and then it fell another 200 basis points commencing with the collapse of Lehman Brothers in September 2008 and continuing to the present. While the first drop of 150 basis points is very plausibly a consequence of capital inflows, the post-crisis drop of 200 basis points is unlikely to be attributable primarily to the GSG;9 instead, that second drop suggests a somewhat parallel story of weak domestic investment in the United States.

State and local government pension systems are increasingly dependent on investment returns, and at risk of increasingly volatile results, as funding levels remain depressed and systems increasingly start to pay out more than they take in, according to a new report from Moody’s.

The credit-ratings agency anticipates higher volatility and lower returns across asset classes in 2021 compared to 2020, even as many pension sponsors have spent the past few years lowering their assumed returns from previous loftier targets that they rarely hit.

“With persistently low interest rates for high-grade fixed-income securities, public pension systems continue to rely on highly volatile equities and alternatives to meet return targets, posing a material credit risk for some governments,” the Moody’s analysts wrote.